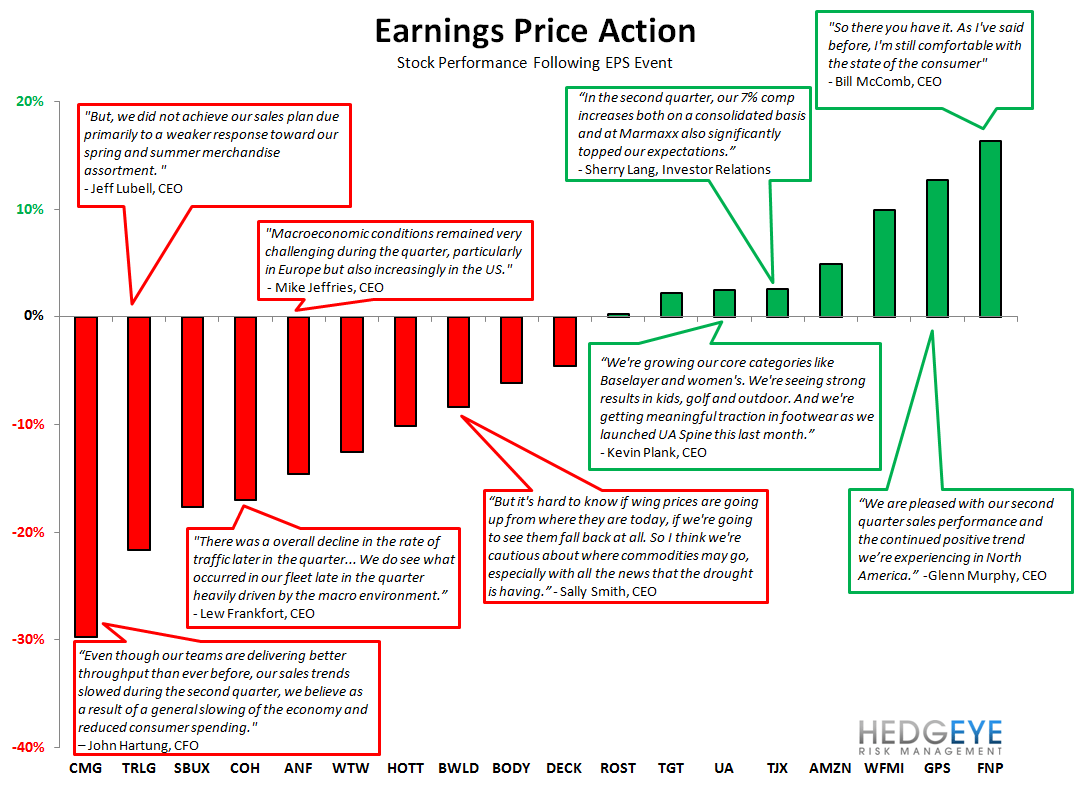

What a week! If there's anything we can say about earnings season thus far, is that the only stocks that were rewarded are those that beat on revenue. With such a poor Macro backdrop and so many companies missing, simple margin upside (especially if SG&A) was not enough. What we find comical is that there are so many companies that took all the credit for their success when Macro was favorable. Now they are blaming the environment on the way down. We won't name names.