TODAY’S S&P 500 SET-UP – August 3, 2012

As we look at today’s set up for the S&P 500, the range is 20 points or -0.66% downside to 1356 and 0.81% upside to 1376.

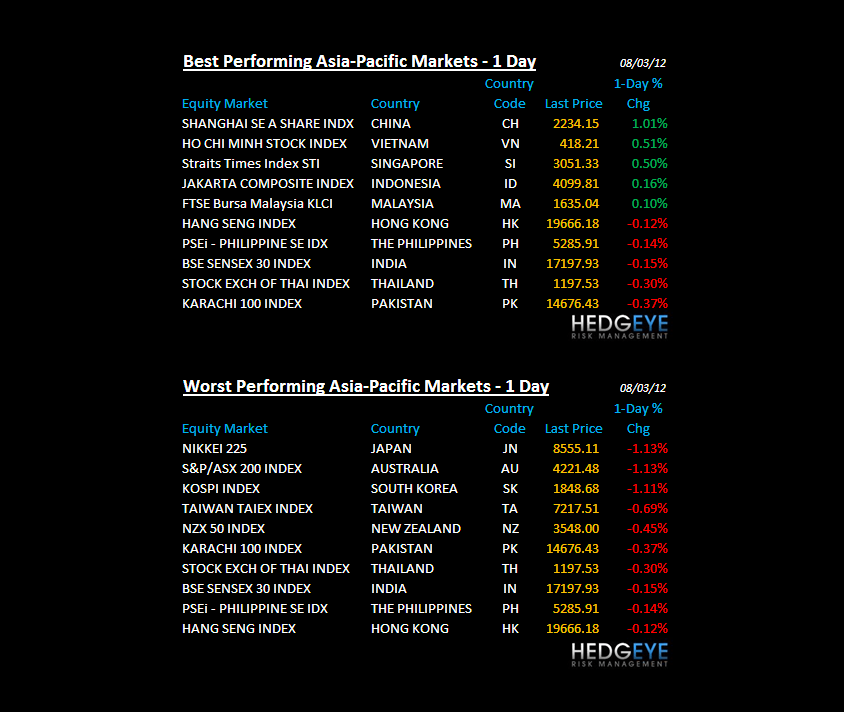

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/02 NYSE -722

- Up versus the prior day’s trading of -779

- VOLUME: on 08/02 NYSE 825.56

- Decrease versus prior day’s trading of -19.47%

- VIX: as of 08/02 was at 17.57

- Decrease versus most recent day’s trading of -7.33%

- Year-to-date decrease of -24.91%

- SPX PUT/CALL RATIO: as of 08/02 closed at 0.97

- Down from the day prior at 1.26

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 35

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.51%

- Increase from prior day’s trading of 1.48%

- YIELD CURVE: as of this morning 1.28

- Up from prior day’s trading at 1.26

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, July, est. 100k (prior 80k)

- 8:30am: Unemployment Rate, July, est. 8.2% (prior 8.2%)

- 8:30am: Avg Hourly Earnings M/m, July, est. 0.2% (prior 0.3%)

- 8:30am: Avg Weekly Hours All Employees, July, est. 34.5 (prior 34.5)

- 10am: ISM Non-Manufacturing, July, est. 52.0 (prior 52.1)

- 1pm: Baker Hughes rig count

GOVERNMENT/POLITICS:

- House is out for Aug. recess. Senate may be in session

- NASA announces winners for the next round of funding to develop spacecraft capable of carrying astronauts, 9am

- FCC holds an open meeting on cable television technical and operational requirements and the use of microwave for wireless broadcasts, 10:30am

WHAT TO WATCH:

- July gain in payrolls probably failed to reduce U.S. unemployment

- Knight said to open books to suitors as loss pressure grows

- Knight losses ignite call for stronger SEC trading oversight

- Citigroup is said to join firms refraining from Knight trading

- Some ETF spreads widen as Knight is fighting to survive

- Joyce faces Knight extinction after computers wipe out profit

- NYSE 2Q earnings drop 20%, beating est.

- Fidelity said to plan jump into ETF business with active funds

- CF Industries to buy Viterra’s interests in CFL for C$915m

- BofA says Libor probe prompts subpoenas over rate submissions

- ECB-politicians’ crisis bargain emerges after 2 1/2 yrs

- Toyota 1Q profit beats est., increases sales forecast

- SAP will pay at least $306m to Oracle in a copyright- infringement lawsuit

- American Express may be forced to pay refunds amid CFPB review

- Morgan Stanley should cut fixed-income unit by half, ISI Says

- BHP to take $3.3b in charges on shale, nickel assets

- Nomura ordered to improve business by FSA on insider leaks

EARNINGS:

- Alliant Energy (LNT) 6am, $0.47

- Northwest Natural Gas Co (NWN) 6am, $0.16

- Pason Systems (PSI CN) 6am, C$0.18

- Immunogen (IMGN) 6:30am, $(0.30)

- Sirona Dental Systems (SIRO) 6:30am, $0.77

- WellCare Health Plans (WCG) 6:30am, $1.21

- Buckeye Partners (BPL) 7am, $0.64

- Brookfield Office Properties (BPO CN) 7am, $0.26

- Gartner (IT) 7am, $0.41

- ITT (ITT) 7am, $0.37

- Procter & Gamble (PG) 7am, $0.77

- Viacom (VIAB) 7am, $1.00

- Exelis (XLS) 7am, $0.48

- Health Net (HNT) 8am, $0.67

- RBC Bearings (ROLL) 8am, $0.61

- TELUS (T CN) 8am, C$1.00

- Telephone & Data Systems (TDS) 8:02am, $0.45

- United States Cellular (USM) 8:03am, $0.72

- PNM Resources (PNM) 8:30am, $0.30

- SNC-Lavalin Group (SNC CN) 9:10am, C$0.61

- Morguard Real Estate Investment Trust (MRT-U CN) 4pm, C$0.34

- UIL Holdings (UIL) 4:10pm, $0.33

- WGL Holdings (WGL) 5pm, $0.01

- Berkshire Hathaway (BRK/A) 5:15pm, $1,777 (possible)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Bull Market in Crops Extends With Spreading Drought: Commodities

- Israel Finds $240 Billion Gas Hoard Stranded by Politics: Energy

- Natural Gas Matches Coal as Top U.S. Power Fuel: BGOV Barometer

- Oil Rises From Three-Week Low on Forecasts U.S. Hiring Increased

- Corn Swings Between Gains, Declines on Drought, Ethanol Usage

- Sugar Seen Falling as Brazil Harvest May Accelerate; Cocoa Gains

- Gold Cuts Weekly Drop in London as Price Slump Spurs Purchases

- Copper Seen Rising as Employment Report May Show Stronger Hiring

- Gold Imports by China From Hong Kong Decline for Second Month

- India’s Power Crisis May Signal Copper Demand: Chart of the Day

- Coal Rally Seen as China’s Cuts Dwarf Australia: Energy Markets

- China to Pay Higher Prices for Soybeans on Drought, USDA Says

- Natural Gas Extends Biggest Decline in Three Years on Stockpiles

- Japan Shifts to Brazilian Corn From U.S. as Prices Reach Record

- Brazil Coffee Growers Harvest 70% of Crop as Dry Weather Helps

- Drought Assistance for Livestock Producers Passed by U.S. House

CURRENCIES

USD – we got longer yesterday (9 LONGS vs 6 at start of the day) but will not overstay my welcome on any cheerleading market open; will watch USD Index as my leading indicator; its down as we type, but as long as it holds $82.35, the Dollar up, deflation of stocks/commodities to lower highs on bounces will continue to be on.

EUROPEAN MARKETS

SPAIN – IBEX was +2% into Draghi, dropped 7% intraday (not a typo) on Draghi, then rallies “off the lows” +1.8% this morning – add all that up and you get the point – this is a complete gong show. Q308 didn’t see country indices whip like that; it’s not the same; it’s much more globally interconnected this time - and expectations for bailouts are a lot higher.

ASIAN MARKETS

JAPAN – Asian stocks continue to move independent of these Western media stories; Nikkei and KOSPI dropped another -1.1% last night (both remain in Bearish Formations) and the Nikkei is down -16.6% now since March. That’s a lot – so you’ll see the central planning begging move to the BOJ now.

MIDDLE EAST

The Hedgeye Macro Team