This note was originally published at 8am on July 19, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Midway upon the journey of our life,

I found myself within a forest dark,

For the straight foreward pathway had been lost."

-Dante Aligihieri, “The Inferno”

Keith is out in California this week meeting with some of our subscribers, so instead of getting up at 2am Eastern time he handed me the baton on the Early Look this morning. As I was riding the train into New York last night, an article in The New Yorker prompted the theme for this note: heat. (By the way, yes I know hockey players from Alberta aren’t supposed to read The New Yorker, but just indulge me this once.)

Whether you are a believer in global warming, or not, this has been one heck of a hot summer. The temperature hasn’t necessarily created an inferno, like in Dante’s namesake poem, but, yes, it has been quite hot. In fact, for the month of June the average temperature in the United States was 71.2 degrees Fahrenheit. This is two degrees higher than the average for the 20th century. In aggregate, the average June temperature made the last 12 months the hottest year since record keeping began in 1895.

Not surprising, especially for those amateur psychologists amongst us, the upshot of the heat wave is that according to a University of Texas poll more than 70% of Americans now believe in climate change. This is up from 52% in the winter of 2011 when we had record snows. If you didn’t know whether the average person reacts to their most proximate stimuli, now you know.

The downside to Mother Nature bringing the proverbial heat is that much of the more agriculturally oriented parts of this country are experiencing droughts. According to the National Atmospheric and Oceanic Administration, the country is under the most severe drought since 1955. Currently, 55% of the contiguous United States is in a moderate-to-severe drought.

So, inferno? Indeed.

The upshot of a drought is that it provides a bullish backdrop for commodity prices. Former Hedgeye intern Brennan Turner recently retired from professional hockey and now operates a brokerage business for farmers in Western Canada. As part of his business he writes a morning note to farmers. In his note from a couple of days ago, he commented that for Canadian farms, because of the drought in the United States, this year could be like three years in one for both yields and revenues. As they say, there is always a bull market somewhere.

The more pressing question for most of us, though, is whether the bull market that has been occurring in U.S. equities over the last week plus is sustainable. Our view, not to mince words, is no. In fact, yesterday between meetings Keith ducked into a Starbucks and shorted the SP500 in the Virtual Portfolio. So, we are official time stamped on our bearish view.

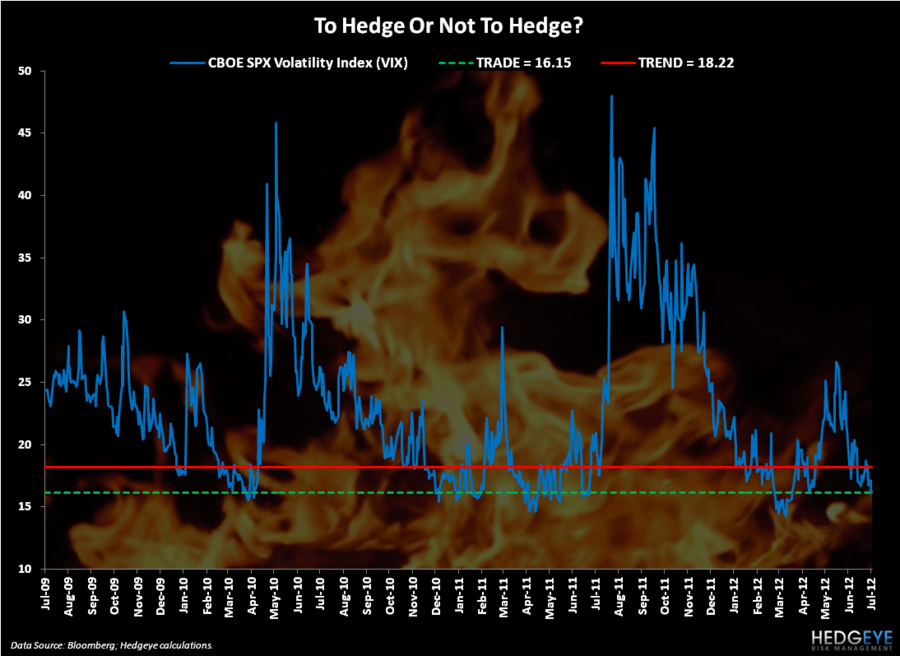

The first thing that concerns us is volatility. As is highlighted in the Chart of the Day, every time that volatility has approached the 15-ish level on the VIX over the past three years, the market has put in an intermediate term top. Volatility is a great proxy for investor sentiment and currently the VIX is at 16.2. Complacency, just like heat, is officially here my friends.

The second factor that we are concerned about is earnings. Wall Street analysts are quite good at engineering earnings “beats”. This quarter is clearly no exception since as of yesterday 73% of companies in the SP500 had “beat” earnings for the quarter. Even if the market is excited by this, those of us who are quantitative in nature should not be surprised.

Coming in the Q2 2012 top down earnings estimates for the SP500 were projecting a -2.1% year-over-year decline in earnings. How’s that for the soft bigotry of low expectations? So sure, companies are beating very low expectations, but more concerning for the equity market is future earnings estimates. Currently, earnings growth for Q1 and Q2 of 2013 is expected to be 14%. Yah, I don’t think so. Both a lack of real earnings growth and declining future earnings are not a positive catalyst for equities.

Finally, one of our last major worries is Europe. Just as the Eurocrats finally go on their lengthy summer vacations, the European sovereign debt markets have again taken a turn for the worse. Overnight, the Spaniards held an auction for 2-5-7 year bonds and bond buyers didn’t exactly bringing the buying heat. To be precise, bid-to-cover was an abysmal 1.9x versus 4.3x just over a month earlier on June 7th. Meanwhile the yield on the Spanish 10-year bond is once again back above the 7% handle.

Not to put wood on my bearish inferno this morning, but for those of you who are interested in stock specific ideas our Restaurant research team, led by Howard Penney, is hosting a conference call on Darden Restaurants this morning. I won’t give away their punch line, but the title of the call is: “Is Darden Too Big Too Perform?” I think you get the drift. If you are institutional investor and interested in listening in, ping sales@hedgeye.com.

Our immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Germany’s DAX, and the SP500 are now $1566-1594, $101.29-106.98, $82.88-83.93, $1.21-1.23, 6499-6752, and 1354-1375, respectively.

Good luck out there today,

Daryl G. Jones

Director of Research