“Nature has made no man a slave.”

-Alcidamas

What would the #OldWall’s manic media mouthpieces do without this week’s central planning events? What would we all do without the drugs that promise to suspend economic gravity? What would we wake up to this morning if markets were actually free?

Alcidamas was a popular Greek philosopher in 4th century BC who Victor Davis Hanson cites at the end of Chapter 8 in “The Soul of Battle.” That quote precedes an excellent chapter in human history titled “And All of Greece Became Independent and Free.”

It’s too bad that when we use the word free in today’s marketplace, the first thing that comes to mind is getting a sticker.

Back to the Global Macro Grind…

US Stocks closed down for the 7th day in the last 9 yesterday, but no worries, we have a central plan on tap at 745AM EST that is going to whip this sucker right back up to a level where perma-bull marketers can say “but the market is up year-to-date.”

Everything in the land of nodding (other than where the entire street gets paid - fund flows, volumes, and performance), is just dandy right now. Buy, hold, and pray.

I have absolutely no idea what this conflicted and compromised central planner is going to tell us today. All I can assure you is that there’s at least -3.5% downside in the EuroStoxx50 and a stiff move to $1.20 in the EUR/USD if he doesn’t deliver the drugs.

Bernanke didn’t crack open the cocaine lines yesterday, and for that, I give him a golf clap. What his pseudo sober decision did to the rest of Global Macro markets was proactively predictable:

- US Dollar went straight back up (+0.7% on the day, closing above an important TRADE line of $82.95 support)

- Gold went straight back down (down a full 1% where we covered our short position at $1603 support)

- US Stocks went down, then up, then back down as underperforming hedgies got whipped around, again

What happens next?

I have no idea. Once I get Draghi’s Italian Job, I’ll let you know. Until then I can only wait and watch for “whatever” as I score ranges, probabilities, and risk managed scenarios – like I do every morning.

On that front, here’s a morning dump for you in US markets:

- US Dollar Index remains in a Bullish Formation (bullish on all 3 of our risk management durations, TRADE/TREND/TAIL)

- US Treasury Yields (10yr) remain in a Bearish Formation (bearish on all 3 of our risk management durations)

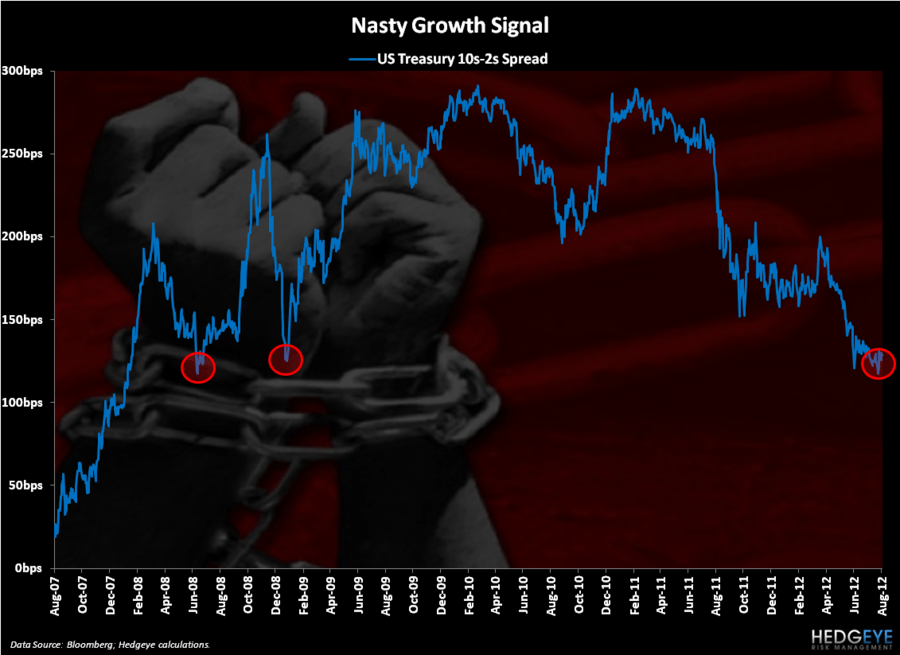

- US Treasury Yield Spread (10s minus 2s) = +129bps wide and continues to compress; very bearish economic signal

- SP500 immediate-term risk range of 1, with its intermediate-term TREND line right in the middle of that (1376)

- US Equity Volatility (VIX) remains in a Bullish Formation with intermediate-term TREND support = $17.62

- US Equity Volume studies are as nasty as I have ever measured them in my career (+16% on yesterday’s down move)

- Russell2000 negatively diverging from SP500, already bearish TRADE and TREND, closing down -1.7% yesterday

- S&P Sector Studies continue to flag on 3 Sectors (out of the 9 majors) as buys (Healthcare, Consumer Staples, Utilities)

- S&P Sectors recently snapping both TRADE and TREND lines = Consumer Discretionary, Transports, and Basic Materials

- Energy (which is asset price inflation, not growth) continues to be the best performer on a 1-month duration

On that last point, Keynesian central planners get their tighty whities in a bunch. I think that’s primarily because it implies that they themselves are perpetuating #GrowthSlowing by infusing a market wedgie of expectations that jams commodity prices higher.

#tighty #whitie #wedgie – none of those words spell checked on my PC, weird.

What might also seem a bit odd to the beggars for more of what isn’t working is what’s going on in the rest of the world this morning:

- Chinese Stocks, after having 1 up day, went straight back down last night (Bearish Formation, down -14% since May)

- Japanese Equities remain no volume/no bid (Bearish Formation, Nikkei225 down -16% since March)

- South Korean Equities (KOSPI, great leading indicator) backed off TRADE resistance of 1881 again last night

Oh, right – the rest of the world, per the Fed and ECB, is really the West. Damn them people in the East who eat inflated food and consume derivatives of $106/barrel Brent Oil.

As we beg the Italian for more of what the British are chastising Chinese swimmers for using, let’s get a medal count:

- China = 30 medals

- USA = 29 medals

- Japan = 17 medals

Not sure what that means for Global Macro other than China is not Japan.

In the spirit of winning, let’s just play the game that’s in front of us out there today. At the end of the day, Market Slavery to the next central plan or not, we can fight this for a lot longer than our overlords can remain in office.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, and the SP500 are now $1, $105.29-107.84, $82.35-84.03, $1.20-1.23, 6, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer