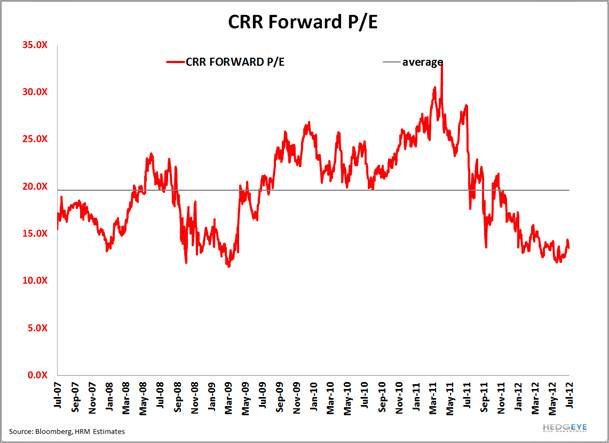

We’ve been bearish on CARBO Ceramics (CRR) for a few weeks now and last week’s earnings confirmed our concerns over demand for ceramic fracking proppant in the energy space. The stock sunk from $83 a share to $68 a share and has continued to sell off since then.

Hedgeye Energy Analyst Kevin Kaiser sees further contraction in CRR as ceramic proppant becomes more commoditized. We doubt that CARBO Ceramics can continue to trade at a 12x multiple on forward P/E as the downfall continues. Like other players in the energy space, CRR needs to lower guidance for the back half of 2012 and into 2013 as margins decrease and proppant costs come down. Looking at the chart below, you can see what the future holds for CRR.