TODAY’S S&P 500 SET-UP – August 1, 2012

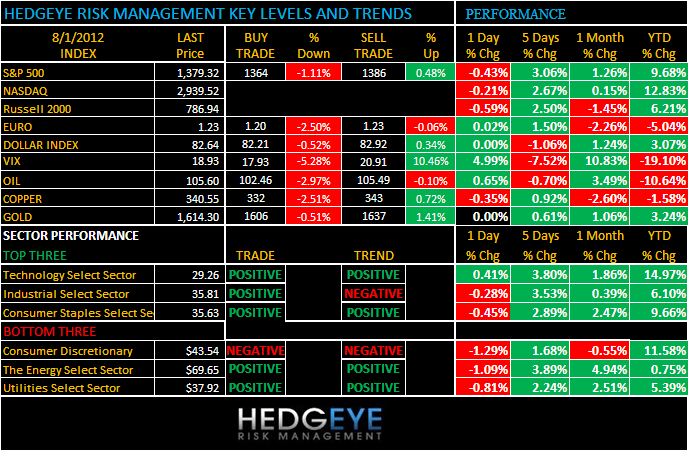

As we look at today’s set up for the S&P 500, the range is 22 points or -1.11% downside to 1364 and 0.48% upside to 1386.

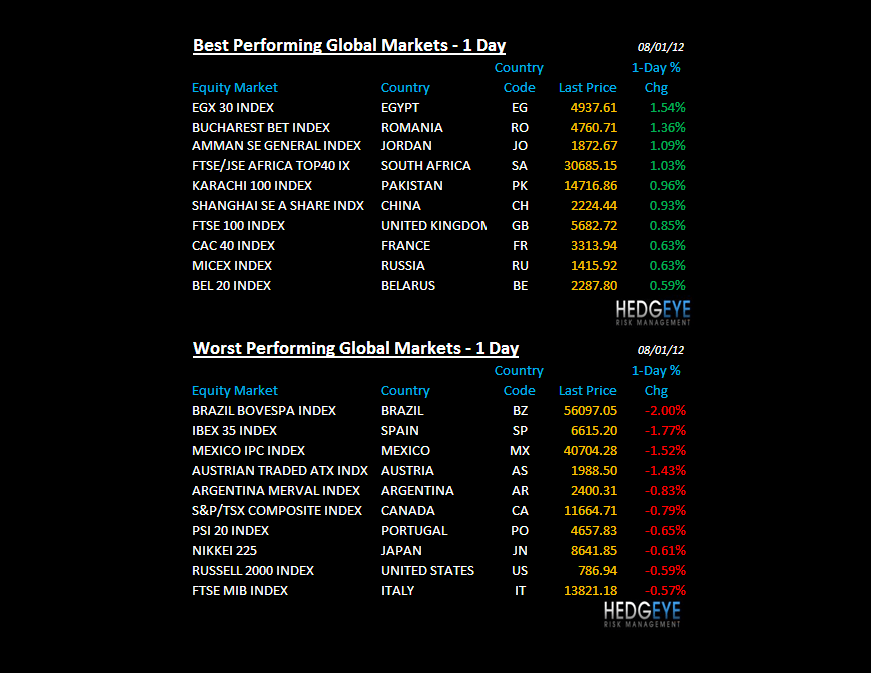

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/31 NYSE -528

- Down versus the prior day’s trading of -88

- VOLUME: on 07/31 NYSE 887.94

- Increase versus prior day’s trading of 34.83%

- VIX: as of 07/31 was at 18.93

- Increase versus most recent day’s trading of 4.99%

- Year-to-date decrease of -19.10%

- SPX PUT/CALL RATIO: as of 07/31 closed at 0.97

- Down from the day prior at 1.00

CREDIT/ECONOMIC MARKET LOOK:

GROWTH – take a step back on look at the global growth data in July from the Big 3 Macro – USA’s was as bad as it’s been, China just printed their slowest PMI in 8 months and Germany just tanked a 43 PMI for July (new low vs 45 in June) too. When the entire world’s growth slows at an accelerating rate, bonds are getting this right and for central planners this is getting #TooBigToBail

INFLATION – that little critter was a positive for markets in May/June as commodity prices got hammered. Not anymore – our models are calling for a sequential rise (m/m) in July as food/energy/housing rents just ripped. Indonesia Just printed that rising inflation fact at +4.6% y/y for July and Brazil pops back up to +6.7%.

- TED SPREAD: as of this morning 35

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.47%

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.27

- Up from prior day’s trading at 1.26

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, July 27 (prior 0.9%)

- 8:15am: ADP Employment Change, July, est. 120k (prior 176k)

- 9am: Markit US PMI Final, July, est. 51.8

- 10am: ISM Manufacturing, July, est. 50.2 (prior 49.7)

- 10am: ISM Prices Paid, July, est. 40 (prior 37)

- 10am: Construction Spending M/m, June, est. 0.4% (prior 0.9%)

- 10:30am: DoE inventories

- 2:15pm: FOMC Rate Decision Announced

- U.S. Treasury announces 3-, 10-, 30-yr auction sizes

GOVERNMENT/POLITICS:

- Senate Banking Committee holds hearing on HUD rental housing programs for the poor

- Senate Environment and Public Works Committee hearing on climate-change and local adaptation measures, 10am

- House Energy and Commerce Committee votes on the No More Solyndras Act, 10am

- FTC Chairman Gary Gensler testifies before the Senate Agriculture Committee on futures market oversight and the collapse of Peregrine Financial, 9am

- U.S.-China Economic and Security Review Commission holds 2- day meeting to prepare 2012 annual report to Congress, 10am

- House Financial Services Capital Markets and Government- Sponsored Enterprises subcommittee marks up H.R. 757, the “Equitable Treatment of Investors Act;” H.R. 2827, which seeks to amend 1934 law to clarify provisions related to regulation of municipal advisers; and H.R. 6161, the “Fostering Innovation Act,” 10:15am

- House Science, Space and Technology’s subcommittee on Space and Aeronautics hearing on commercial suborbital reusable launch vehicle market, 2pm

- House Science and Technology Committee hears from representatives of Lockheed Martin and Deere on the relationship between business and research universities, 10 am

- Regulators from 11 Asia-Pacific nations to discuss carbon trading, smart-grid technologies and market regs, 8:30am

- CFPB Director Richard Cordray testifies before the House Small Business Cmte on CFPB regulations/small businesses, 1pm

- Health insurers including UnitedHealth, WellPoint face deadline to send $1.3b in rebates to ~12.8m customers who paid more than the law allows for their 2011 policies

- U.S. Postal Service will miss a $5.5b payment due to the U.S. Treasury for future retirees’ health care

- House Armed Services Cmte hearing on defense sequestration, including OMB Dir. Jeff Zients, 10am

WHAT TO WATCH:

- Fed may extend low-rate pledge beyond 2014: economists

- Olympus sees violation of laws possible with U.S. disclosure

- Italy PM Mario Monti is making the rounds of European capitals as his country’s borrowing costs creep higher, pressing leaders for collective action

- Geithner vows to press for writedowns for underwater home loans

- Carl Icahn said to sell MGM Holdings stake back to film studio

- July manufacturing in U.S. probably stagnated as spending cooled

- Automakers may show annual sales at 14.1m rate, analysts say

- Apple lawyer tells jury Samsung concluded “it’s easier to copy”

- MF Global customers eventually will recoup their money, according to trustee overseeing the parent co.’s liquidation

- Monsanto’s $1b patent claim against DuPont to go to jury

- China manufacturing teetered close to contraction in July

- Edison sees possible generation unit bankruptcy, nuclear probes

- U.K. July manufacturing shrank most in 3+ yrs

- Australian house prices unexpectedly rise as RBA lowers rates

- Eloqua offers 50% discount to software-as-service Peers in IPO

EARNINGS:

- Burger King Worldwide (BKW) Bef-mkt, $0.14

- Huntsman (HUN) 6am, $0.54

- Enterprise Products (EPD) 6am, $0.58

- Amerigroup (AGP) 6am, $0.70

- Catamaran (CCT CN) 6am, $0.55

- Macerich (MAC) 6am, $0.73

- Dollar Thrifty Automotive Group (DTG) 6am, $1.24

- El Paso Electric (EE) 6:08am, $0.74

- SPX (SPW) 6:30am, $0.74

- RR Donnelley (RRD) 6:30am, $0.43

- Calumet Specialty Products (CLMT) 6:30am, $0.53

- Littelfuse (LFUS) 6:30am, $1.00

- Garmin (GRMN) 6:30am, $0.67

- Intact Financial (IFC CN) 6:55am, C$1.40

- DST Systems (DST) 7am, $0.97

- American Tower (AMT) 7am, $0.77

- Booz Allen Hamilton (BAH) 7am, $0.42

- Wisconsin Energy (WEC) 7am, $0.44

- Avon Products (AVP) 7am, $0.22; Preview

- Comcast (CMCSA) 7am, $0.48

- Time Warner (TWX) 7am, $0.58

- Tronox (TROX) 7am, $0.57

- Harley-Davidson (HOG) 7am, $1.05

- Senior Housing Properties Trust (SNH) 7:01am, $0.46

- AGL Resources (GAS) 7:30am, $0.28

- Hospira (HSP) 7:30am, $0.49

- Devon Energy (DVN) 7:30am, $0.82

- Wright Express (WXS) 7:30am, $0.98

- Hyatt Hotels (H) 7:30am, $0.22

- Owens Corning (OC) 7:30, $0.64

- IntercontinentalExchange 7:30am, $1.32

- Mastercard (MA) 8am, $5.58

- Phillips 66 (PSX) 8am, $1.78

- HSN (HSNI) 8am, $0.61

- Magellan Midstream (MMP) 8am, $0.90

- Marathon Oil (MRO) 8:30am, $0.59

- Allergan (AGN) 9am, $1.06; Preview

- Cavium (CAVM) 4pm, $0.02

- Unum Group (UNM) 4pm, $0.76

- Itron (ITRI) 4pm, $0.97

- Alexander & Baldwin (ALEX) 4pm, $0.15

- Matson (MATX) 4pm, $0.36

- Clear Channel Outdoor Holdings (CCO) 4pm, $(0.01)

- BioMarin Pharmaceutical (BMRN) 4pm, $(0.21)

- Portfolio Recovery Associates (PRAA) 4pm, $1.63

- Walter Energy (WLT) 4pm, $0.39

- Green Mountain Coffee Roasters (GMCR) 4:01pm, $0.49

- Amdocs (DOX) 4:01pm, $0.67

- Williams Partners (WPZ) 4:01pm, $0.49

- Williams Cos (WMB) 4:01pm, $0.25

- New Gold (NGD CN) 4:01pm, $0.09

- DaVita (DVA) 4:01pm, $1.47

- MetLife (MET) 4:03pm, $1.24

- Onyx Pharmaceuticals (ONXX) 4:04pm, $(0.91)

- First Solar (FSLR) 4:05pm, $0.93

- Hanover Insurance Group (THG) 4:05pm, $0.19

- Weight Watchers International (WTW) 4:05pm, $1.35

- Trimble Navigation (TRMB) 4:05pm, $0.70

- Mako Surgical (MAKO), 4:05pm, ($0.22)

- Equity One (EQY) 4:07pm, $0.27

- Prudential Financial (PRU) 4:07pm, $1.54

- Lincoln National (LNC) 4:08pm, $1.00

- Boston Beer (SAM), 4:10pm, $1.28

- Hartford Financial Services Group (HIG) 4:15pm, $0.46

- Avis Budget Group (CAR) 4:15pm, $0.70

- Intrepid Potash (IPI) 4:15pm, $0.25

- Transocean (RIG) 4:15pm, $0.44; Preview

- Federal Realty Investment Trust (FRT) 4:30pm, $1.04

- Dominion Resources (D) 4:30pm, $0.60

- CVR Energy (CVI) 4:35pm, $2.13

- Chemtura (CHMT) 4:51pm, $0.52

- First Quantum Minerals (FM CN) 4:59pm, $0.22

- Home Capital Group (HCG CN) 5pm, C$1.53

- Tesoro (TSO) 5pm, $2.29

- Murphy Oil (MUR) 5pm, $1.33

- Orient-Express Hotels (OEH) 5pm, $0.13

- General Growth Properties (GGP) 5:19pm, $0.21

- Rexnord (RXN) Aft-mkt, $0.24

- Centerra Gold (CG CN), Post-Mkt, ($0.15)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor is checking out of the Bernanke Bailout drug deal early here this morning; not sure what it means or if Gold/Oil will follow – this man has proven he will do anything to keep commodity/stock markets up. Game time decision; regardless he can’t arrest Growth Slowing and Inflation Rising here in July/August.

- All Markets Gain First Time in Two Years Led by Drought, Draghi

- South America Readies Record Crop Amid U.S. Drought: Commodities

- Wheat Drops as European Harvest May Help Offset U.S. Drought Cut

- Oil Trades Near Two-Week Low on Concern Central Banks Won’t Act

- Copper Drops as Chinese Manufacturing Unexpectedly Slows Down

- Cocoa Nears Nine-Month High on West African Sales; Sugar Rises

- Gold Seen Gaining in London on Speculation About Monetary Easing

- Sugar Output in India’s Biggest Grower May Climb 10% Next Year

- Ivory Coast’s Coastal Cocoa Farmers Say Drought Threatens Crop

- Worst India Outage Highlights 60 Years of Missed Targets: Energy

- Rain-Scarce India Depends on Record Inventory to Feed People

- Sweltering Mideast Boosts Diesel as India Wilts: Energy Markets

- UN CO2 Offsets, EU Permits Lead Commodity Declines in July

- Palm Oil Gains as Demand Seen Climbing on U.S., India Crop Woes

- Rubber Drops as China Manufacturing Grows at Slowest in 8 Months

- Wheat Exports From Pakistan to Plunge as Flood Cuts Harvest

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team