Conclusion: This company smells so much like it did at the time it was spun out of Sara Lee. We think that the market is giving the company too much credit in blowing through historical profitability, and out-earning the best brands in the business. The consumer is unlikely to be that forgiving.

We think that a whole lot of historical context is needed in looking at this HBI quarter. The reason is that in reconciling the company’s guidance for earnings and cash flow for 2H and 2013, you need to go back in time to 2006 and imagine that you’re the analyst at a buldge bracket brokerage firm that just got the call from your banker regarding the mandate to lead the spin-off from Sarah Lee (hint hint).

Think of the following.

1) HBI is guiding for 2H EBIT margins to come in between 12.5-13.0%, and that was unprescedented. Its’ historical 2H peak is 11.6%. For the record, Nike and Ralph Lauren will be lucky to land those margin levels in the back half.

2) Getting long term debt to $1bn by the end of 2013 means that HBI needs to generate well over $600mm in free cash flow next year. That’s about 35% higher than anything HBI ever reported.

Now here’s the interesting part. When did HBI print those margin levels? In 2004-05. And the peak free cash flow numbers? In 2004-05. When did Sara Lee spin-out Hanesbrands? 2006. If there’s anything that the company made no secret about way back then were the contentious ‘discussions’ between SLE and HBI because it was being spun out with such a disproportionately high debt burden. In addition to being saddled with debt, SLE had underinvested in HBI in the 2-years prior (SG&A), knowing full well that it would be monetized over the intermediate-term. The punchline is that we’re talking about achieving margin and free cash flow rates well above those realized when the company was being dressed up to maximize the amount of capital that ultimately ended up in SLE’s wallet – and leaving HBI in a multi-year hole in the process.

So the question is…can they get to these levels?

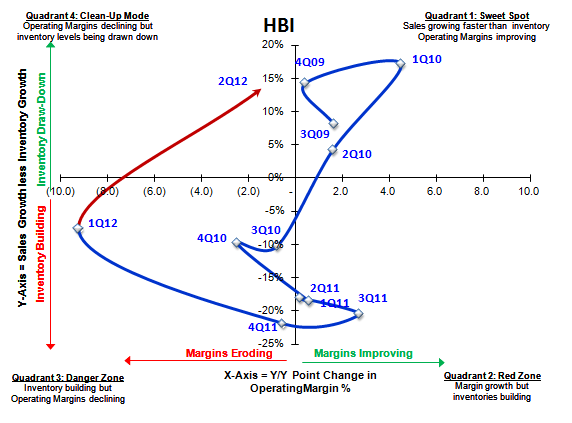

Yeh…perhaps. But a lot needs to go right. Was I the only one who was disturbed that Outerwear margins were down 1,200bps, International was down 1.8%, and most notably Direct to Consumer was DOWN 3%? DTC (which is largely dot.com) should never be down for any company. Period.

The View on Inflation is All Wrong!

The most troubling thing from my perspective is this prevailing view that ‘inflation is good’ and that the recent raw material cycle has ‘broken in’ the retailers like oil to a new baseball glove, conditioning them to pay higher prices in the future. That’s an assumption that we don’t think belongs in any good risk management process.

Ultimately, the consumer will decide if the inflation will sustain itself. Not the retailers. Just because costs change, it does not mean that the consumer’s perceived value proposition will change. In the context of the value proposition, will the consumer be cool with Nike getting a lower margin than HBI? I know that sounds like a ridiculous question, as the consumer is not looking at comparative margin charts. But they are pretty smart with where their dollars go, and beyond the course of several quarters, this is a question that is not only 100% valid, but one that needs to be asked. When the answer is ‘No’ it always leads to violent swings in a given company’s results relative to plan.

It’d be unfair not to mention that there is a pretty positive angle here. Even if EBIT growth is flat this year, we get 300-500bp of EPS growth from delevering. You’ve got to hand it to the company in that they have systematically chipped away at the $2.6bn debt burden they were originally handed, and are now sitting at only $1.65bn. Next year, lower interest expense alone gets HBI 12% earnings growth.

In addition, the working capital change this quarter was nothing short of astounding – with days inventory on hand off by about 36 days. Much of that is due to the yy change in raw materials costs, but the numbers are what they are. And they’re positive. The question, as noted above, is whether the retailer and consumer will allow them to keep it.

Our take on the Stock

In the end, the consensus is right in line with this margin and cash flow guidance for this year, and is at $3.14 next year – in line with management’s continued comment of a ‘potential’ EPS in the ‘low 3s’ in 2013. We're 5-8% lower in each period.

On these numbers, the stock definitely looks cheap at about 10x. But the reality is that it still has debt, and a cash flow outlook that we think is far less stable than the market thinks as the mid-tier landscape is rattled by JCP. At nearly 9x EBITDA, we can think of a dozen other places to invest our capital.

Brian P. McGough