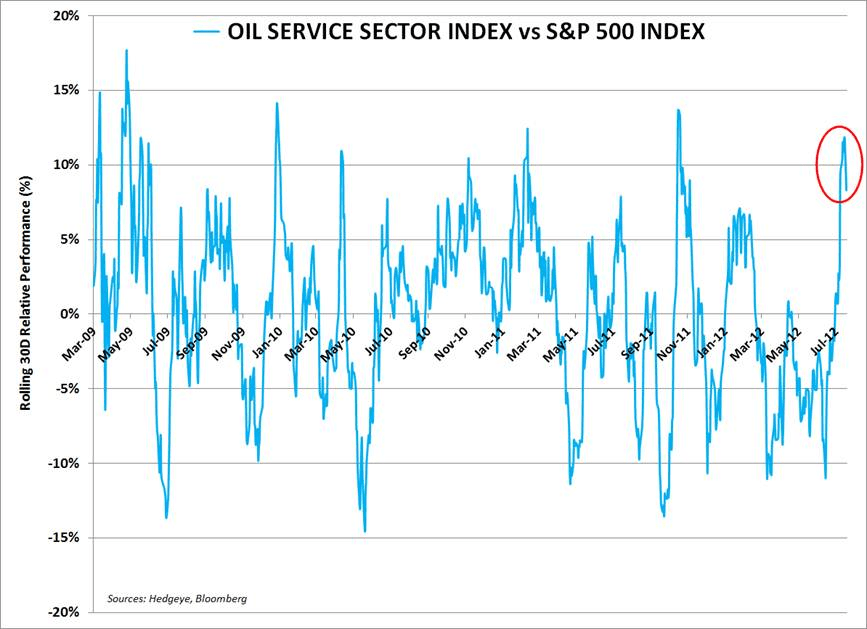

As the inflation trade prepares to make a big move this week courtesy of the Federal Open Market Committee (FOMC) meeting, the energy sector is at the center of everyone’s attention. The Oil Services Sector Index (OSX) has outperformed the broader market (the S&P 500) more than 8% over the last 30 days. The high beta nature of the sector can be attributed to the performance, but there are three underlying themes that highlight why this is happening:

1. Better-than-expected earnings reports from BHI, HAL, SLB, NOV, CAM and others. It is worth noting that the “beats” came off very low expectations and numbers that had been significantly revised lower over the prior six months. This is a very important point to keep in mind.

2. Inflation trade – Brent crude is up 8.3% MTD. This is subject to change if the US dollar roars back into action and heads higher; oil in turn will fall significantly should this occur considering we have an abundance of crude currently available.

3. Mean reversion move. The OSX still trails the S&P500 by 27% over the last 12 months even with the recent gains.

As the chart above shows, the OSX tends to fluctuate between +15% and -15% versus the S&P 500 with a tendency to auto-correlate. Hedgeye Energy Analyst Kevin Kaiser expects some profit taking to occur over the next three weeks (our TRADE duration), but the FOMC decision this week and performance of the dollar will weigh heavily on the OSX performance going forward. After all, if oil continues to climb higher, OFS names like the ones listed above will be able to put up better numbers in the third quarter.