TODAY’S S&P 500 SET-UP – July 31, 2012

As we look at today’s set up for the S&P 500, the range is 35 points or -1.61% downside to 1363 and 0.92% upside to 1398.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/30 NYSE -88

- Down versus the prior day’s trading of 2012

- VOLUME: on 07/30 NYSE 658.58

- Decrease versus prior day’s trading of -27.85%

- VIX: as of 07/30 was at 18.03

- Increase versus most recent day’s trading of 7.96%

- Year-to-date decrease of -22.95%

- SPX PUT/CALL RATIO: as of 07/30 closed at 1.00

- Down from the day prior at 1.26

CREDIT/ECONOMIC MARKET LOOK:

10yr – both the US and German 10yr fall right back after testing immediate-term TRADE resistance (yields); immediate-term TRADE resistance for the UST 10yr = 1.59%, so we bought back our long-bond TLT position on that yesterday, taking our Fixed Income asset allocation back up to 21%; the bond market has been nailing #GrowthSlowing since March.

- TED SPREAD: as of this morning 34

- 3-MONTH T-BILL YIELD: as of this morning 0.11%

- 10-Year: as of this morning 1.49%

- Decrease from prior day’s trading at 1.50%

- YIELD CURVE: as of this morning 1.27

- Down from prior day’s trading at 1.28

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook retail sales

- 8:30am: Annual Revisions: Personal Income and Spending

- 8:30am: Employment Cost Index, 2Q, est. 0.5% (prior 0.4%)

- 8:30am: Personal Income, June, est. 0.4% (prior 0.2%)

- 8:30am: Personal Spending, June, est. 0.1% (prior 0.0%)

- 8:30am: PCE Deflator M/m, June, est. 0.0% (prior -0.2%)

- 8:30am: PCE Core M/m, June, est. 0.2% (prior 0.1%)

- 9am: S&P/CS 20 City M/m, May, est. 0.4% (prior 0.7%)

- 9am: S&P/CaseShiller Home Price Index, May, est. 137.55 (prior 135.8)

- 9:45am: Chicago Purchasing Manager, July, est. 52.4 (prior 52.9)

- 10am: Consumer Confidence, July, est. 61.5 (prior 62)

- 11am: Fed to purchase $4.25b-$5b notes due July 31, 2018-May 15, 2020

- 11:30am: U.S. to sell 4-wk bills

- 2pm: Fed will release tentative outright Treasury operation schedule

- 4:30pm: API Inventories

GOVERNMENT/POLITICS:

- House Energy and Commerce subcommittee holds forum to discuss state and federal cooperation on the Clean Air Act, 2pm

- House Oversight Committee hearing on federal privacy and data security, 10am

- Senate Committee on Commerce, Science Transportation markup to extend 2006 law to stop spam, spyware, fraud across borders; nomination of Michael Huerta, to be FAA admin., 2:30am

- Treasury Secretary Timothy F. Geithner speaks to the Los Angeles World Affairs Council on U.S, and world economies, 3pm

- David Cohen, Treasury’s undersecretary for terrorism and financial intelligence, speaks at department’s public hearing on plans to propose rules on customer due diligence requirements for financial institutions, 9:30am

- Senate Appropriations defense subcommittee drafts its version of the annual defense spending bill, 10:30am

- Air Force holds press briefing at Pentagon on latest assessment of oxygen-deficiency symptoms that have affected pilots flying Lockheed Martin’s F-22 Raptor, 3pm

- FERC Chairman Jon Wellinghoff discusses reliability of electric grid, EPA regulations, climate change in appearance at Platts Energy Podium, 1pm

- ITC hears evidence in a microprocessors patent-infringement case brought against Apple by Taiwan-based VIA Technologies, which is affiliated with HTC, 9am

WHAT TO WATCH:

- Federal Open Markets Committee begins 2-day meeting

- Euro-area unemployment rate reaches record 11.2%

- Apple said to prepare iPhone redesign for Sept. 12 release

- Yahoo Interim CEO Ross Levinsohn departs after Marissa Mayer gets CEO job

- BP 2Q net loss $1.39b vs net income $5.72b Y/y

- Cantor placed on review for cut by Moody’s amid trading weakness

- Japan’s unexpected drop in unemployment helps sustain growth

- UBS, Deutsche Bank profits decline, missing ests.

- Panasonic 1Q net income 12.8b yen, analyst est. 9.2b yen

- Honda 1Q net 131.7b yen, est. 150.7b yen

- Manchester United seeks as much as $333m in U.S. IPO

- Sanofi’s Genzyme unit sued by Teva over worker-raiding claims

- RealD fell as much as 21% after missing ests. due to costs to supply theaters with new eyeglasses

- Humana cuts profit forecast as rising Medicare costs surprise

- Lehman raises $4.7b in 2Q toward creditor payments

- Boeing 787’s debris-spewing GE engine to be dismantled in probe

- Ex-UBS Officers “lied and cheated’ on muni bond deals, U.S. says

EARNINGS:

- Yandex (YNDX) 6am, $0.16

- Tyco (TYC) 6am, $0.93; Preview

- Aetna (AET) 6am, $1.25

- NiSource (NI) 6:30am, $0.20

- Harris (HRS) 6:30am, $1.41

- Goodyear Tire & Rubber (GT) 6:30am, $0.45

- Cobalt International Energy (CIE) 6:40am, $(0.09)

- Foster Wheeler (FWLT) 6:45am, $0.43

- Delphi Automotive (DLPH) 7am, $0.92

- Thomson Reuters (TRI CN) 7am, $0.50

- Pfizer (PFE) 7am, $0.54; Preview

- Dentsply International (XRAY) 7am, $0.56

- Coach (COH) 7am, $0.85

- TRW Automotive Holdings (TRW) 7am, $1.55

- Archer-Daniels-Midland Co (ADM) 7am, $0.58

- Entergy (ETR) 7am, $1.41

- Discovery Communications (DISCA) 7am, $0.70

- United States Steel (X) 7:05am, $0.49

- Marathon Petroleum (MPC) 7:06am, $2.51; Preview

- Public Service Enterprise Group (PEG) 7:30am, $0.45

- Revlon (REV) 7:30am, $0.32

- Cummins (CMI) 7:30am, $2.28

- Valero Energy (VLO) 7:30am, $1.43; Preview

- HCP (HCP) 7:45am, $0.68

- Louisiana-Pacific (LPX) 8am, $0.05

- George Weston (WN CN) 8am, C$0.96

- Martin Marietta Materials (MLM) 8:05am, $1.01

- Ecolab (ECL) 8:25am, $0.72

- TransAlta (TA CN) 8:50am, C$(0.03)

- Toromont Industries (TIH CN) 11:13am, C$0.36

- Saputo (SAP CN) 11:58am, C$0.66

- Edison International (EIX) 4pm, $0.32

- WebMd (WBMD) 4pm, $0.123

- Electronic Arts (EA) 4:01pm, $(0.42)

- DreamWorks Animation SKG (DWA) 4:01pm, $0.25

- Solar Capital (SLRC) 4:01pm, $0.58

- Axis Capital Holdings (AXS) 4:01pm, $0.93

- Life Technologies (LIFE) 4:01pm, $0.97

- BMC Software (BMC) 4:05pm, $0.75

- Take-Two Interactive (TTWO) 4:05pm, $(0.66)

- ONEOK (OKE) 4:05pm, $0.33

- ONEOK Partners (OKS) 4:05pm, $0.70

- Allstate (ALL) 4:05pm, $0.52

- QEP Resources (QEP) 4:05pm, $0.33

- Genworth Financial (GNW) 4:07pm, $0.18

- Arthur J Gallagher (AJG) 4:09pm, $0.56

- Kimco Realty (KIM) 4:09pm, $0.31

- Verisk Analytics (VRSK) 4:10pm, $0.47

- Frontier Communications (FTR) 4:11pm, $0.05

- RenaissanceRe Holdings (RNR) 4:22pm, $2.48

- FMC (FMC) 4:30pm, $0.91

- Jones Lang LaSalle (JLL) 4:30pm, $1.24

- BRE Properties (BRE) 4:30pm, $0.58

- DDR (DDR) 5pm, $0.25

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – the #BailoutBulls are going for gold here into this week’s central planning events; TRADE resistance now support at $1606; long term-TAIL risk line up at $1679. Be careful what you beg for; another Qe will cut whatever is left of the US consumption growth phalanx to shreds.

- Most-Accurate Gold Forecasters Splitting After Rout: Commodities

- Oil Supplies Decline in Survey on Refining High: Energy Markets

- Grain Cargoes Seen Slowing Most in 19 Years on Drought: Freight

- Corn Climbs to Record as Futures Head for Best Month Since 1988

- Weak India Rains to Spur Record Cooking-Oil, Lentil Imports

- Rubber Demand in China to Contract 5% as Truck Sales Tumble

- Palm-Oil Shipments From Indonesia Set to Gain on Lower Duty

- WTI Crude May Slump to $83 Fibonacci Level: Technical Analysis

- Copper Rises as China Increases Spending on Railroad Network

- Gold Seen Extending Monthly Gain on Monetary Easing Stimulus

- Australia Wins as Buyers Shift to Wheat From Corn on Drought

- Rice Stockpiles in Japan Seen Declining, Boosting Prices

- Iron Ore Price Decline in China Seen by Arctic as Import Spur

- Gold-Backed Loans to Climb at Indonesian Banks: Islamic Finance

- Chinese Steelmakers Profit Tumbles 96% on Lower Demand, Prices

- Oil Rises, Set for First Monthly Gain in Three on Stimulus Talk

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – last day of the month, so why not throw some Chinese rumoring on top of the markup pile? Regardless, Chinese stocks make fresh new lows, down another -0.3% (down -14.5% since May); we do not think they cut rates w/ $106/barrel Brent Oil.

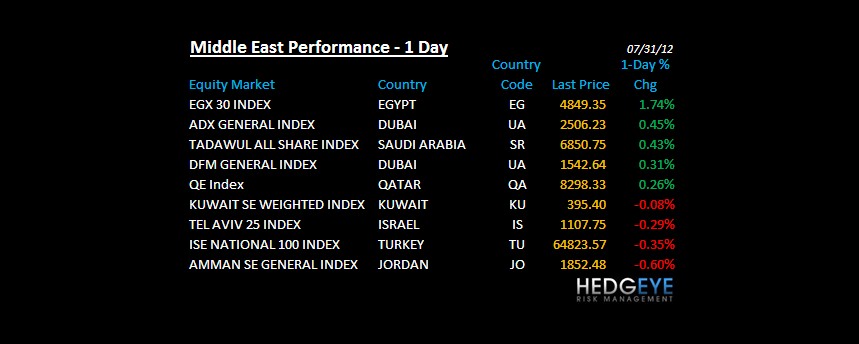

MIDDLE EAST

The Hedgeye Macro Team