On Friday (7/27) Keith made a number of trades in our Hedgeye Virtual Portfolio related to Europe. He shorted the EUR/USD via the etf FXE, shorted Italy via EWI (note that on Friday the short selling ban on stocks trading on the FTSE MIB was extended to September 14th), and went long German Bunds (BUNL).

Keith’s trading calls are tactically taking advantage of the current price dislocation and not major changes in our broader theses across Europe. We saw these “dislocations” into and out of ECB President Mario Draghi’s comment on Thursday that “the ECB is ready to do whatever it takes to preserve the euro.”

In short we believe Draghi’s “whatever” comment could boost broader European capital markets, including the EUR/USD, going into Thursday’s ECB meeting because Draghi has put himself in a box in which he has to deliver to the market something on the monetary and/or fiscal fronts.

However, we expect any announcement from Draghi to under-deliver based on market expectations for a bazooka. Specifically, we think Draghi should reengage the SMP, a positions the Germans are still against. We see a very low probability of another long-term LTRO being issued (due to the lack of success the last two had) and we see a split probability on a 25bp cut to the main interest rate. Yet even if the rate was cut, we’d expect it to have very little lasting impact on the markets.

Keith covered FXE today in the Virtual Portfolio to take a gain on the short side. Our immediate term TRADE levels for the EUR/USD are $1.20-1.23. As we mention above, we expect Draghi’s “whatever” comment to put support in the cross until Thursday morning’s ECB press conference at 8:30am EST.

As it relates to the BOE’s interest rate decision on Thursday, we expect no change in the main rates, and no additional asset purchases following a £50 Billion increase on 7/5 when the Bank last met (to take total purchases to £375 Billion), despite continued challenged economic fundamentals.

Below we show our levels with Keith’s commentary on all three securities recently traded:

EWI - I've seen some ridiculous 1-2 day moves in the last 5yrs. This one might take the cake. Italy right back to immediate-term TRADE overbought.

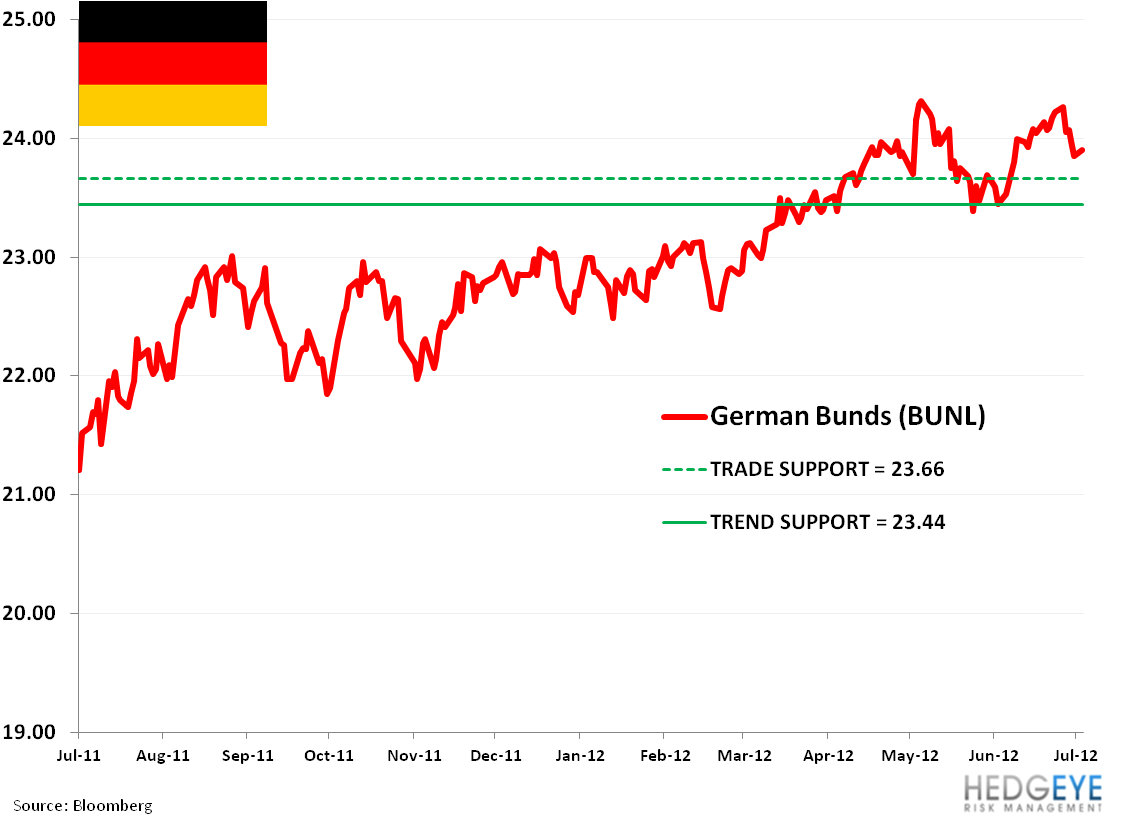

BUNL - German Bunds are immediate-term TRADE oversold within their bullish intermediate-term TREND.

FXE - Whatever it takes right back at you Mr. Draghi. Re-shorting the Euro at the top end of our immediate-term TRADE range (of $1.23).

Matthew Hedrick

Senior Analyst