-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Short EUR/USD (FXE); Short Italy (EWI); Buying German Bunds (BUNL)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +0.6% week-over-week vs +0.7% last week. Top performers: Spain +5.9%; Russia (RTSI) +5.1%; Italy +4.1%; Finland +2.8%; France +2.7%; Sweden +1.7%; Germany +0.9%. Bottom performers: Cyprus -13.6%; Greece -7.1%; Portugal -3.0%; Ireland -1.9%.

- FX: The EUR/USD is up +1.04% week-over-week vs -0.74% last week. W/W Divergences:HUF/EUR +1.95%; CZK/EUR +1.13%; PLN/EUR +1.04%; DKK/EUR +0.01%; CHF/EUR +0.00%; SEK/EUR -0.24%; RUB/EUR -1.18%.

- Fixed Income: There were significant moves in sovereign yields this week, all of which may be less clear on a week-over-week basis. Nevertheless, Greece saw the largest move, up a monster +196bps w/w to 27.46%. Portugal rose +85bps to 11.35%.

On Monday Spain and Italy issued short selling bans on all stocks for a duration of 3 months and one week, respectively. This influenced yields early in the week. Spanish yields rose to an all-time high of 7.62% on Tuesday but declined following Draghi’s comments on Thursday (more below). The Spanish 10YR actually declined -46bps on the week to finish at 6.81%. Italy declined -15bps on the week, but also moved to 6.46% on Tuesday before closing down today at 5.93%. Germany saw an inflection to the upside with the yield climbing +17bps on the week to 1.35%. France followed, gaining +15bps to 2.18%.

Draghi to the Rescue!??

What a difference a week makes. Check, this isn’t a unique statement – it can be said for almost every week in the last two years of European trading. Up, down, and sometimes sideways. European capital markets for most weeks have been manic alongside investors hanging on to every headline and fumes of hope around Eurocrat actions. This week, Draghi stole the podium, but then again what exactly did he promise? -- Nothing! He said at an investment conference in London on Thursday that: “within our mandate, the ECB is ready to do whatever it takes to preserve the euro,” adding , “believe me, it will be enough.” And the market rallied!

This comment followed a Draghi interview on Monday with the French newspaper, Le Monde, in which he said that the euro is not in danger, saying that some analysts “don't recognize the political capital that our leaders have invested in this union and Europeans' support," and added that the euro is "irreversible".

Humm! We too have not discounted the resolve of Eurocrats to fight the fires and keep the Union intact to maintain job security. The issue here, though, is that Draghi hints at possessing some bazooka that he’s been concealing for all this time. We frankly don’t think there is one, particularly because we can’t envision what one grand bazooka would look like. Certainly there are a number of programs with loose strings, undefined terms, and a lack of consensus (like the Fiscal Compact; Pan-European Deposit Insurance; Eurobonds/-bills; European Redemption Fund; European Financial Transactions Tax; SMP; and the terms and scope of the ESM), all or part of which, if better defined and agreed upon, could buoy capital markets, yet can do little to turn around Europe’s weak growth fundamentals over the near to intermediate term. The most immediate question mark is if Draghi will reengage the SMP to buy secondary bonds from Italy and Spain after 19 straight months of the facility being dormant.

Fundamentals Stink

I’d encourage you to check out the section below labeled Data Dump. While this week’s high frequency data is no exception from recent weeks (in the move lower), it’s worth highlighting a few points. Germany, a country looked to for relative growth this year, had a number of weak figures: preliminary PMI Manufacturing came in at 43.3 for JULY (exp. 45.1) vs 45.0 JUN and Services dropped to 49.7 JUL Prelim (exp. 50.0) vs 49.9 JUN. And whether it was the German IFO or GfK confidence surveys, across most all subcategories, numbers declined month-over-month. In particular, Germany’s IFO Expectations fell to 95.6 in JULY (exp. 96.8) vs 97.2 JUN.

Other highlights include Q2 GDP results that came in lower for Spain and the UK. While this data is “stale” and isn’t a huge surprise, the results confirm our forecast of slower growth across most of Europe. Spain’s Q2 GDP fell -0.4% Q/Q vs -0.3% in Q1 (or -1.0% Y/Y vs -0.4%). UK’s Q2 preliminary GDP fell -0.7% Q/Q vs consensus -0.2% and prior -0.3% (or -0.8% Y/Y vs consensus -0.3% and prior -0.2%).

Europe’s August Away Message and the Looming Dark Catalyst Calendar

It’s worth mentioning that a number of key European heads of state are taking vacation in August, including Germany’s Angela Merkel and her finance minister Wolfgang Schaeuble; France’s Francois Hollande; Italy’s Mario Monti; and Portugal’s Pedro Passos Coelho according to a Bloomberg article. As Keith would say, if Eurocrats are not going to accomplish anything on their five hour lunches, they’re certainly not going to get anything done sitting at the beach!

From a calendar perspective we continue to express the importance of 12 September when Germany’s Constitutional Court rules on the constitutionality of the ESM and Fiscal Compact. If Germany doesn’t pass the ESM, in particular, the program is back to square one, and leaves the region further in stitch as the EFSF funding ticks down (and is massively undercapitalized to deal with potential sovereign and banking bailout needs/risks on the horizon). Please note that as of now, even if the German Court passes, there is no specific language governing the scope of the ESM, beyond the three vague paragraphs issued at the June 28-29 Summit Meeting.

Some catalysts to keep front and center that may influence capital markets:

20 August - Greece has a payment of a €3.2B bond (held by the ECB) that matures. Payment is still being discussed.

September - Troika officials will return to Greece in September to complete their final assessment of the implementation of the bailout program. Could there be another debt restructuring?

Late September - According to La Tribune, Moody's will evaluate the consequences of the Eurozone crisis on France's AAA rating by the end of Q3. We think a downgrade to AA is a real probability.

Mid- October - There’s a possibility of a German Sovereign credit rating downgrade, especially should France be reduced by a notch beforehand.

Spain - Debt maturity schedule scares as the Treasury is bumping up against sovereign debt maturities of €20.27 of debt maturing on two days, on 29-Oct and 31-Oct.

The Ridiculous Statement of the Week

German Finance Minister Wolfgang Schaeuble and Spanish Economy Minister Luis de Guindos issued a joint statement that said the recent spike in [Spanish] interest rates does not reflect “the fundamentals of the Spanish economy, its growth potential and the sustainability of its public debt”.

Portfolio Moves:

Today Keith made a number of trades in our Hedgeye Virtual Portfolio related to Europe. He shorted the EUR/USD via the etf FXE, shorted Italy via EWI (note there is a selling short ban against stocks trading on the FTSE MIB that ends today), and went long German Bunds (BUNL).

Keith’s trading calls are tactically taking advantage of price dislocation and not major changes in our broader theses across Europe. Note that Draghi’s comments greatly impacted market prices this week.

Keith’s comments are below:

EWI - I've seen some ridiculous 1-2 day moves in the last 5yrs. This one might take the cake. Italy right back to immediate-term TRADE overbought.

BUNL - German Bunds are immediate-term TRADE oversold within their bullish intermediate-term TREND.

FXE - Whatever it takes right back at you Mr. Draghi. Re-shorting the Euro at the top end of our immediate-term TRADE range (of $1.23).

Call Outs:

Moody’s - Changes Aaa-Rated Germany, Netherlands, Luxembourg Outlook to Negative, putting them in line with Austria and France which have been on a negative outlook since February 13, 2012. France - President Francois Hollande’s transaction tax is set to take effect Aug. 1, not all investors will be paying it. To escape the tax, many institutional investors will turn to so-called contracts for difference, or CFDs, offered by prime brokers that let them bet on a stock’s gain or loss without owning the shares. Traders have used it successfully to skirt the U.K.’s stamp duty.

EFSF - Moody's changes outlook on the provisional AAA long-term rating of the EFSF to negative from stable.

ESM - ECB council member Ewald Nowotny said in an interview that there are arguments in favor of giving the ESM, the Eurozone's permanent bailout mechanism, a banking license. However, he added that he is not aware of any specific discussions on the matter within the ECB at this point.

SMP - The FT said that Spain's insistence that the ECB to reactivate its SMP is unlikely to elicit a near-term policy response from the central bank. The article noted that the bank believes that its balance sheet should be used as a last resort and any bond buying should first be done by the Eurozone's bailout mechanism.

Moody’s - The Agency changed the outlook on 17 German banking groups to negative (reflecting sovereign outlook).

Spain - Der Spiegel noted that Süddeutsche Zeitung reported on Thursday that the EU is considering using the EFSF to buy Spanish bonds from private banks. The paper cited an unnamed EU diplomat who said that "If Madrid submits a request we are prepared to act". It added that sources close to the German government said that Berlin was not opposed to bond purchases in principle.

Spain - Reuters, citing sources, reported that Spain is not considering seeking immediate help from the EU to ease its surging borrowing costs, despite German and Italian newspaper reports on Thursday that said Madrid was ready to ask the EFSF to buy its bonds. However it added that the Eurozone is considering possible action for later this year.

Spain - ECB data noted that Spanish banks trimmed their holdings of government bonds by €1.3M in June, the third consecutive month of decline. The article pointed out that in the four years to March, that figure had increased by €77B.

Greece - Citi raised its probability of Greece leaving the euro in the next 12 to 18 months to ~90% from its earlier estimate of 50-75%. The firm said that an exit would most likely happen in the next two to three quarters.

Eurozone banks - Eurozone debt makes up ~8% of the total holdings of the 10 largest US prime money-market funds, or ~$49B, down from 30%, or $230B in May 2011.

Ireland - Ireland on Thursday returned to the bond market for the first time in nearly two years. Recall that Ireland was forced to secure a bailout in 2010. The National Treasury Management Agency sold €4.19B of a new five-year bond, along with another bond that matures in 2020.

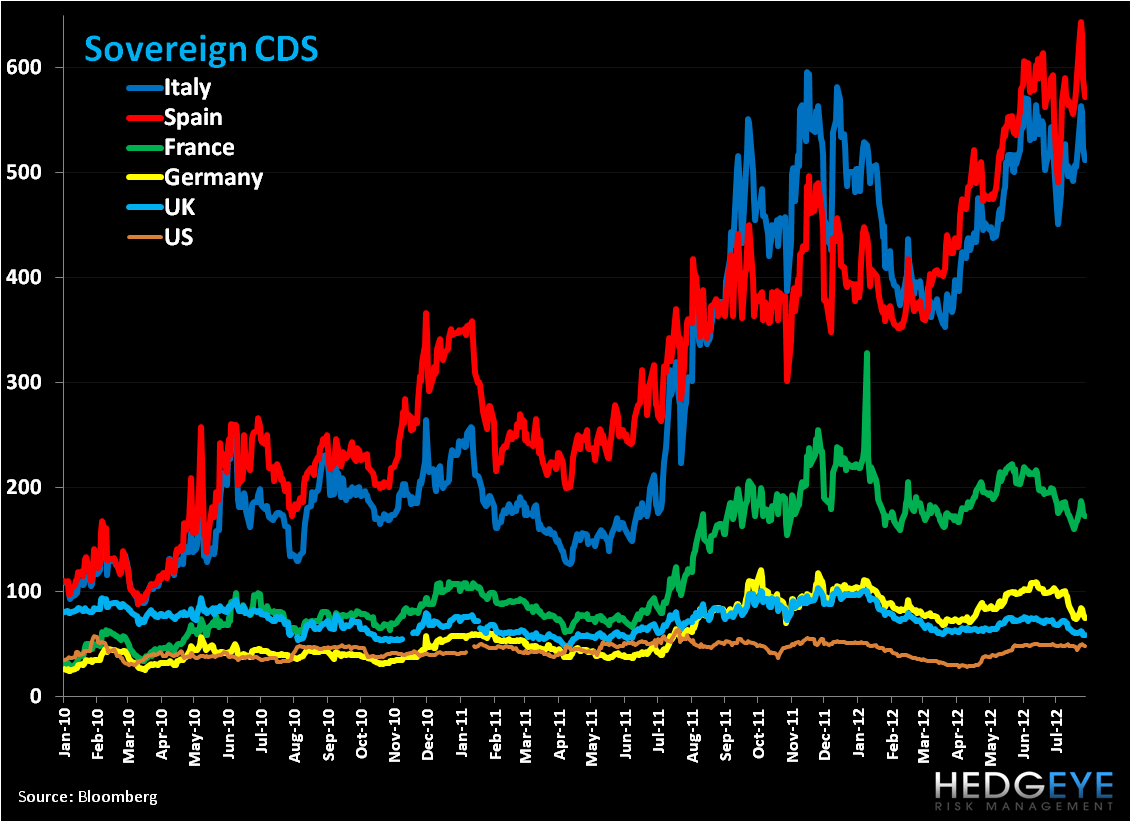

Risk Monitor:

Sovereign CDS were mixed across the peripheral countries this week. On a week-over-week basis Portugal rose the most, up +29bps to 856bps, followed by France +4bps to 172bps. Ireland saw the largest decline (-28bps) to 534bps, followed by Spain (-22bps) to 572bps.

Data Dump:

Eurozone PMI Composite 46.4 JUL Prelim (inline) vs 46.4 JUN

Eurozone PMI Manufacturing 44.1 JUL Prelim (exp. 45.2) vs 45.1 JUN

Eurozone PMI Services 47.6 JUL Prelim (exp. 47.1) vs 47.1 JUN

Eurozone Consumer Confidence -21.6 JUL Prelim (exp. -20) vs -19.8 JUN

Eurozone M3 3.2% JUN Y/Y (exp. 2.9%) vs 3.1% MAY

Germany PMI Manufacturing 43.3 JUL Prelim (exp. 45.1) vs 45.0 JUN

Germany PMI Services 49.7 JUL Prelim (exp. 50.0) vs 49.9 JUN

Germany IFO Business Climate 103.3 JUL (exp. 104.5) vs 105.2 JUN (28-month low)

Germany IFO Current Assessment 111.6 JUL (exp. 113.0) vs 113.9 JUN

Germany IFO Expectations 95.6 JUL (exp. 96.8) vs 97.2 JUN

Germany GfK Consumer Confidence 5.9 AUG (exp. 5.8) vs 5.8 JUL

Germany Import Price Index 1.3% JUN Y/Y (exp. 1.9%) vs 2.2% MAY

Germany CPI 2.0% JUL Prelim Y/Y (exp. 1.9%) vs 2.0% JUN [0.4% JUL Prelim M/M (exp. 0.4%) vs -0.2%]

France Business Survey Overall Demand -24 JUL vs -2 JUN

France Consumer Confidence 87 JUL (exp. 90) vs 89 JUN

France PMI Manufacturing 43.6 JUL Prelim (exp. 45.5) vs 45.2 JUN

France PMI Services 50.2 JUL Prelim (exp. 47.5) vs 47.9 JUN

France Own-Company Production Outlook -8 JUL (exp. -6) vs -5 JUN

France Production Outlook -45 JUL (exp. -35) vs -35 JUN

France Business Confidence 90 JUL (exp. 92) vs 91 JUN

UK Q2 preliminary GDP -0.7% Q/Q vs consensus -0.2% and prior -0.3

UK Q2 preliminary GDP -0.8% Y/Y vs consensus -0.3% and prior -0.2%

Spain Producer Prices 2.5% JUN Y/Y (exp.3.1%) vs 3.2% MAY

Spain Mortgages on Houses -30.5% MAY Y/Y vs -31.3% APR

Spain Mortgages-capital Loaned -32.4 MAY Y/Y vs -26.4% APR

Spain Unemployment Rate 24.63% in Q2 vs 24.44% in Q1

Italy Consumer Confidence 86.5 JUL (exp. 85) vs 85.4 JUN

Italy Business Confidence 87.1 JUL (exp. 88.5) vs 88.7 JUN

Italy Retail Sales -2.0% MAY Y/Y (exp. -4.7%) vs -6.8% APR

Sweden Consumer Confidence 5.6 JUL (exp. 2.5) vs 3.1 JUN

Sweden Manufacturing Confidence -2 JUL (exp. -5) vs -5 JUN

Sweden Economic Tendency 96.1 JUL (exp. 98) vs 98.4 JUN

Sweden Household Lending 4.5% JUN Y/Y vs 4.6% MAY

Sweden PPI 0.4% JUN Y/Y vs 0.3% MAY

Sweden Unemployment Rate 8.8% JUN vs 8.1% MAY

Sweden Retail Sales 0.9% JUN Y/Y (exp. 1.5%) vs 4.6% MAY

Finland Business Confidence -6 JUL vs -6 JUN

Finland Consumer Confidence 0.1 JUL vs 5.8 JUN

Finland PPI 0.5% JUN Y/Y vs 0.9% MAY

Finland Unemployment Rate 7.9% JUN vs 9.5% MAY

Denmark Consumer Confidence 0.1 JUL (exp. -3.0) vs -2.6 JUN

Ireland Property Prices -14.4% JUN Y/Y vs -15.3% MAY

Ireland Retail Sales (volume) -5.5% JUN Y/Y vs -2.0% MAY

Switzerland KOF Swiss Leading Indicator 1.43 JUL vs 1.15 JUN

Austria Industrial Production 2.6% MAY Y/Y vs 1.5% APR

Netherlands Producer Confidence -5.2 JUL (exp. -4.7) vs -4.8 JUN

Poland Unemployment Rate 12.4% JUN vs 12.6% MAY

Poland Retail Sales 6.4% JUN Y/Y (exp. 9.0%) vs 7.7% MAY

Poland Core Inflation 2.3% JUN Y/Y (exp. 2.4%) vs 2.3% MAY

Hungary Economic Sentiment -23.2 JUL vs -24.5 JUN

Hungary Business Confidence -13.3 JUL vs -14.6 JUN

Hungary Consumer Confidence -51.4 JUL vs -52.6

Hungary Retail Trade -2.5% MAY Y/Y vs -2.8% APR

Czech Republic Business Confidence 2.3 JUL vs 4.6 JUN

Czech Republic Consumer and Business Confidence -3.8 JUL vs -2.2 JUN

Czech Republic Consumer Confidence -28.3 JUL vs -29.3 JUN

Croatia Unemployment Rate 17.3% JUN vs 18.0% MAY

Turkey Foreign Tourist Arrivals 2.7% JUN Y/Y vs -1.5% MAY

Interest Rate Decisions:

(7/24) Hungary Base Rate UNCH at 7.00%

The Week Ahead:

Monday - Jul. Eurozone Consumer Confidence – Final, Business Climate Indicator, Economic Confidence, Industrial Confidence, Services Confidence; Jul. UK CBI Reported Sales, GfK Consumer Confidence Survey; Jun. UK Net Consumer Credit, Net Lending Sec. on Dwellings, Mortgage Approvals, M4 Money Supply; Jul. Spain CPI - Preliminary; May Spain Total Housing Permits; 2Q Spain GDP – Preliminary

Tuesday - Jul. Eurozone CPI Estimate; Jun. Eurozone Unemployment Rate; Jul. Germany Unemployment Data Released by Federal Labor Agency, Unemployment Change and Rate; Jun. Germany Retail Sales; Jul. UK BRC Shop Price Index; Jun. France Producer Prices, Consumer Spending; Jun. Spain Retail Sales, Budget Balance; May Spain Retail Sales; Jul. Italy CPI - Preliminary; Jun. Italy Unemployment – Preliminary, PPI; May Greece Retail Sales

Wednesday - Jul. Eurozone PMI Manufacturing – Final; Jul. Germany PMI Manufacturing – Final; Jul. UK Nationwide House Prices, PMI Manufacturing; Jul. France PMI Manufacturing – Final; Spain Manufacturing PMI; Jul. Italy Manufacturing PMI, New Car Registrations, Budget Balance; Greece Manufacturing PMI

Thursday - ECB Announces Rates; Jun. Eurozone PPI; UK BoE Asset Purchase Target, BoE Announces Rates; Jul. UK PMI Construction; Jul. Spain Unemployment

Friday - Jul. Eurozone PMI Services and Composite - Final; Jun. Eurozone Retail Sales; Jul. Germany PMI Services – Final; Jul. France PMI Services – Final; Jul. UK PMI Services, Official Reserves; Spain Services PMI; Jul. Italy PMI Services

Extended Calendar Call-Outs:

12 September: Germany’s Constitutional Court rules on the constitutionality of the ESM and Fiscal Compact

Late September: According to La Tribune Moody's will evaluate the consequences of the Eurozone crisis on France's AAA rating by the end of Q3. We think a downgrade to AA is a real probability.

Mid- October: Possibility of German Sovereign credit rating downgrade.

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst