I just wanted to send out a thank you note to the CEO of DNKN, Nigel Travis, for validating my research process here at Hedgeye Risk Management. Unfortunately, I was not allowed the opportunity to ask a question on the conference call this morning, but I would have thanked him personally over the phone had the chance arisen.

I knew I had touched a nerve on the last conference call. Two things I have learned during my career:

- When a management team calls out an analyst’s research as “nonsense”, the analyst is often correct.

- When a management team purports to paternalistically protect investors from their own analytical ineptitude, they’re usually not doing that to protect the stock from becoming over-inflated.

Consider this quote from Nigel Travis, to me, on the most recent earnings call:

“We took a decision when we went public that we weren't going to release pipeline information. We think that's the right thing because it can be interpreted in all kinds of ways.”

On the back of some stronger-than-expected 1Q12 numbers, Travis attacked our thesis on his stock and our view that there was a lack of evidence that the company can grow in line with his guidance and the Street’s expectations. To be clear: our thesis has, from the start, included the caveat that we can only work with the data management provides publically: the Store Development Agreements (SDA’s) on the investor relations website. This data is limited, but the information regarding openings on the company’s investor relations website suggests a shrinking backlog of stores. This “nonsense” thesis that we were communicating was based, in part, on the assumption outlined above in point two, above.

On 3/19/12, we wrote: “The evidence for our view is as follows: announced new unit openings are lagging actual openings, which is leading to a decline in the backlog of potential new units being opened. Until we are proven wrong by greater disclosure from Dunkin’, we will continue to be bearish on the company’s growth prospects per the announcements of new contracted openings by the company.”

As our clients know, our view has been based on a lack of evidence – concrete evidence – that the backlog of new unit openings was growing in line with the necessary growth rate required to meet company growth targets. Call us crazy, but erring on the side of caution seemed most appropriate to us when valuing a stock that is being sold hand over fist by insiders while management shirked away from disclosing information on the most important component of its long term outlook. Our stance on this stock has been solely aimed at providing a sober, transparent, and logical approach to a growth story that – to this day – is sorely lacking in transparency. And the insiders have been selling, presumably out of a sense of civic duty to their fellow investors.

It is still a little early to say, but it seems that our thesis could be correct. Looking at the 2Q12 numbers released today, it appears that management is likely going to be hard-pressed to meet its Dunkin’ Donuts growth targets in the U.S. Gross openings were flat year-over-year in the second quarter, while net openings of U.S. Dunkin’ Donuts units came to 19 versus 54 expected by the Street, according to Consensus Metrix.

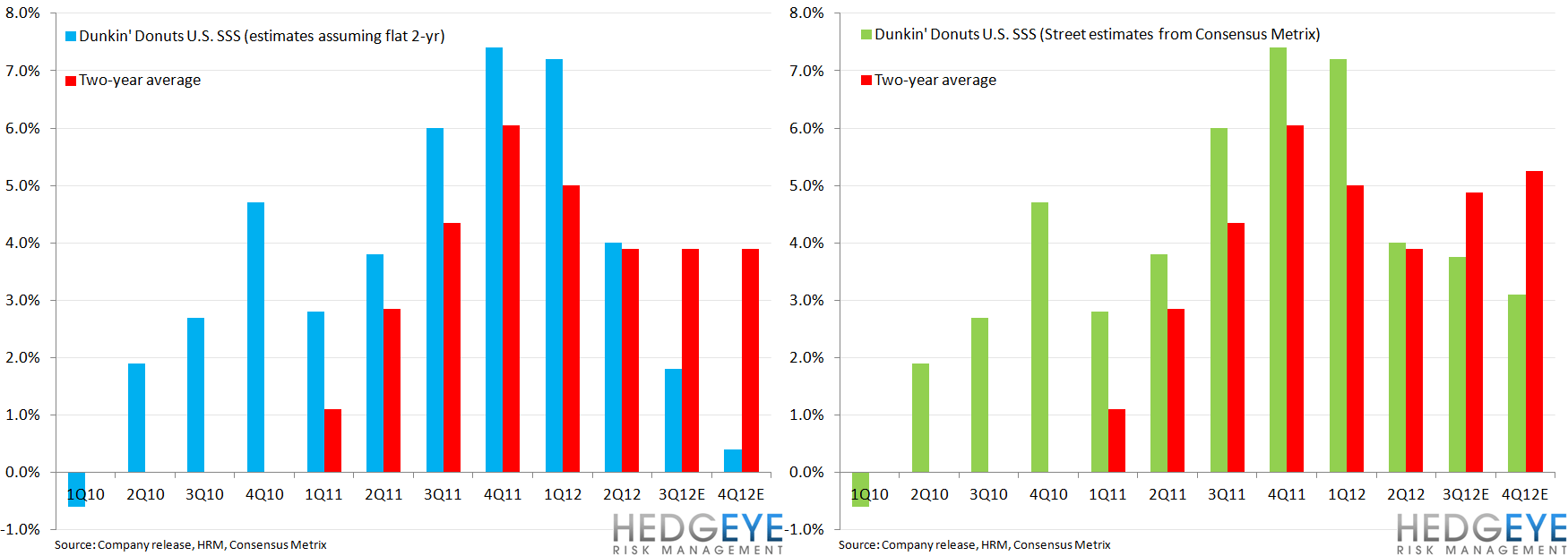

The bulls have shifted from “growth” to “comps” and now have nowhere to go. The issue of unit openings is not the end for Dunkin’ Brands. Same-store sales missed expectations by a wide margin; meeting full-year comps estimates will require a strong sequential acceleration in two-year average trends. If you have a list of consumer companies that is going to see a V-Bottom in two-year average trends in the back half of this year, I bet that list is short and Dunkin’ is not on it. Consensus is expecting that, as the chart on the right, below, illustrates. Even maintaining flat two-year average trends is likely overly-bullish but that scenario, illustrated by the chart on the left, shows comps missing consensus by 190 and 270 basis points in 3Q and 4Q, respectively. We don’t think comps are overly material for Dunkin’ Brands; it is a franchised business whose future earnings growth is primarily predicated on unit growth. Nevertheless, we do not think the same-store sales numbers over the remainder of the year will help franchisee demand for the Dunkin’ Donuts brand, however good Mr. Travis “feels” about it.

Howard Penney

Managing Director

Rory Green

Analyst