This note was originally published at 8am on July 12, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“You are on your own and you must take ownership of your own destiny.”

-Hugh Hendry

No, that wasn’t the new marketing pitch from President Obama. That’s from one of Scotland’s finest – the one and only Hugh Hendry. He runs Eclectica Asset Management.

Eclectica isn’t a word that spell-checks on this word processor – that’s why you just have to love the name. This guy couldn’t give 2 deflated Canadian copper cents about what other people think about him and/or his Global Macro process.

“For me, this has always meant being detached from the sell-side community. It is not a question of respect, it is just that I prefer not to engage in their perpetual dialogue of determining where the “flow” is. I cannot be reached by telephone… not one buddy, not one phone call, not one instant message. I am not seeking that kind of “edge”…” (Manager Commentary, April 2012)

Back to the Global Macro Grind…

What’s our edge? Math.

Every single Global Macro thought, theme, and position we consider putting our name on is driven by what the market tells us. We don’t tell the market what to think. We aren’t that “smart.” The market tells us.

When I started in the hedge fund business in 1998, “smart” meant something that’s a lot different than what it means today. Smart is as performance does. It doesn’t mean coming up with a “value” idea, pitching it to all your favorite “smart” friends (after you bought it), getting them to buy it, and then promoting it on TV.

Modern Global Macro Risk Management (i.e. post 2007) uses computers. I hear a lot of whining about this – “it’s the machines”… I mean get real already. If it’s the machines, hire more super smart people to build better machines to front run the other machines.

Front-run?

Yep, I just wrote that. And I can because A) I don’t run a prop desk B) I don’t run a bank and C) I don’t run a broker-dealer. Front-running the machines is simply having a repeatable math-based decision making process that keeps you 1, 2, and hallelujah if it’s 3 steps ahead of the smartest guys/gals in the room.

In other words, understand what the other machines will act on, and act ahead of their most probable behaviors. If someone legitimately believes that the 50-day Moving Monkey is a risk management process, great. Let them – and more importantly, don’t interrupt them while they get whipped around by it.

Been there, done that.

I saw (I don’t hear, I use Twitter) more “flow” yesterday about the 50-day moving average being “intact” (it’s at 1335) than just about anything that was flowing into yesterday’s market close.

What, precisely, does that mean to people? Do they actually run other people’s money using a 1-factor simple moving average that my 4-year old son could replicate with his iPad and bang out conclusions on any ticker I give him?

That’s the biggest risk to our profession. The simple reality is that, since 2007, a lot of people have not changed what it is that they do. That’s sad and exciting. Sad because sad is as sad does; exciting because it provides for creative destruction – the guts of what we do.

What’s our edge?

Like I said, it’s math. And what I mean by that is that I am constantly re-modeling a baseline 3-factor model with dynamic price, volume, and volatility data across 3 core durations (TRADE, TREND, and TAIL).

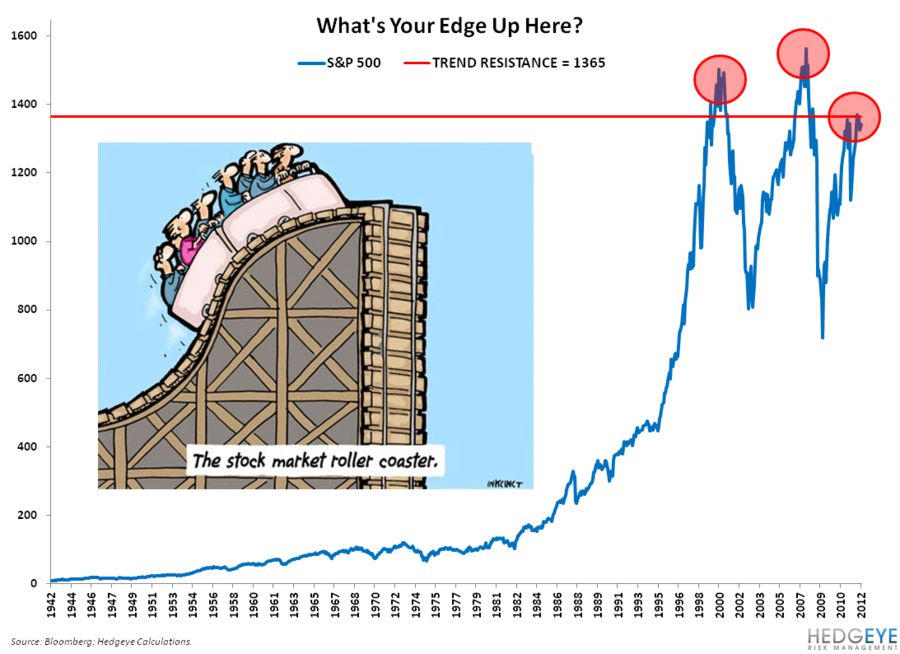

Currently, looking at the SP500 for example, here’s what I see:

- Intermediate-term TREND resistance overhead (that’s bearish) at 1365

- Immediate-term TRADE support below last price (that’s bullish) at 1333

- An intermediate-term risk management range of 1286-1365

We’re Duration Agnostic. So you tell me what the duration of your risk is, and we’ll tell you what the risk of the range within your duration is. This gives us a very simplified edge that is our own. Our edge is making decisions at the highest probability points within our defined duration and range. It doesn’t mean we are always right; it means we don’t swing at outside pitches.

Our edge is by no means easy to derive. I have a team of 27 analysts constantly pumping me with quantitative inputs that I can add and/or subtract from our models. Constantly re-modeling; constantly changing – that is what I do. And I’m very humbled by the idea that I can attempt to explain our edge to you each and every day. Being held accountable to our process can only make us better.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1549-1587, $98.24-103.01, $82.61-83.96, $1.21-1.24, and 1333-1354, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer