CAT: Backlog Decline Implies Weak Orders

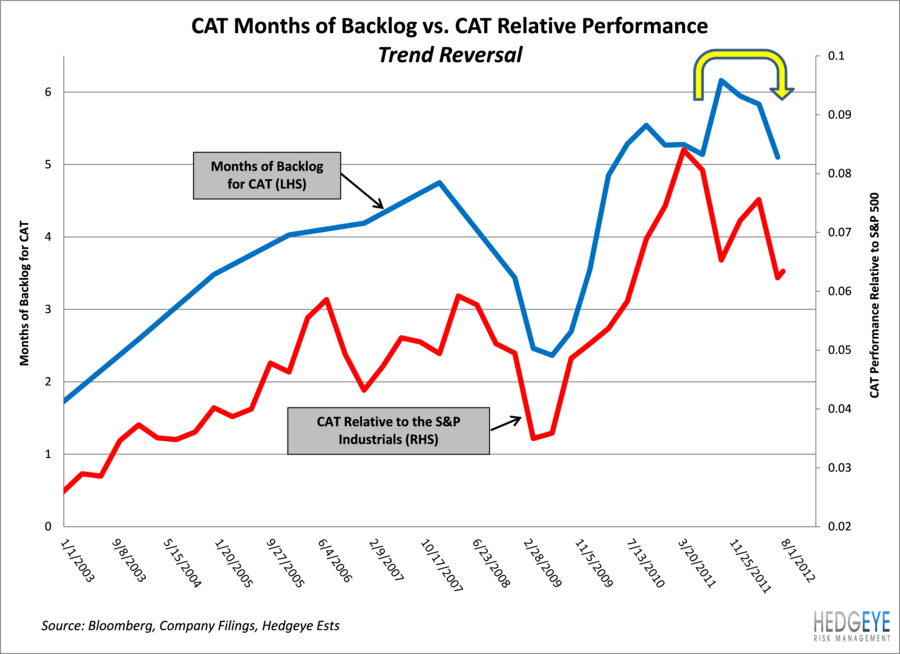

- Despite the move up in CAT today, which we view as short covering driven, weak backlog trends support recent underperformance in the shares.

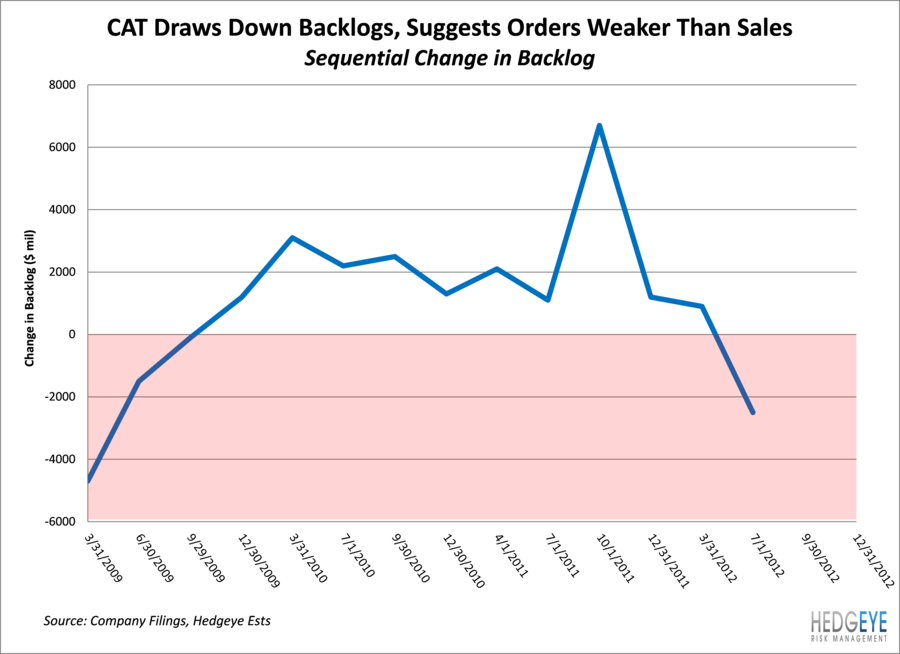

- Backlogs declined for first time since 3Q 2009, as the company drew down backlogs in todays “beat.”

- As shown below, months of backlog are highly correlated with CAT’s relative performance.

- Implied orders (estimated as change in backlogs plus revenue) declined 3.0% y-o-y after posting 12.2% growth y-o-y in 1Q2012. That is a significant deceleration.

- Something has to give: orders will need to rebound, production will have to be cut, or backlogs will be drawn down. The current macro data does not suggest a near-term order rebound to us.

- CAT has been one of the primary beneficiaries of what we view as unsustainably high levels of resource capital investment. Slowing activity in China is a risk to mining capital spending.

- Though CAT has an excellent competitive position and a strong franchise, we believe that the shares are overvalued from a cyclically adjusted perspective.

- While the months of backlog is still relatively high, historically that has presented an exit opportunity.

Orders vs. Revenue: Implied orders rates now trail revenue, as indicated by backlog declines.

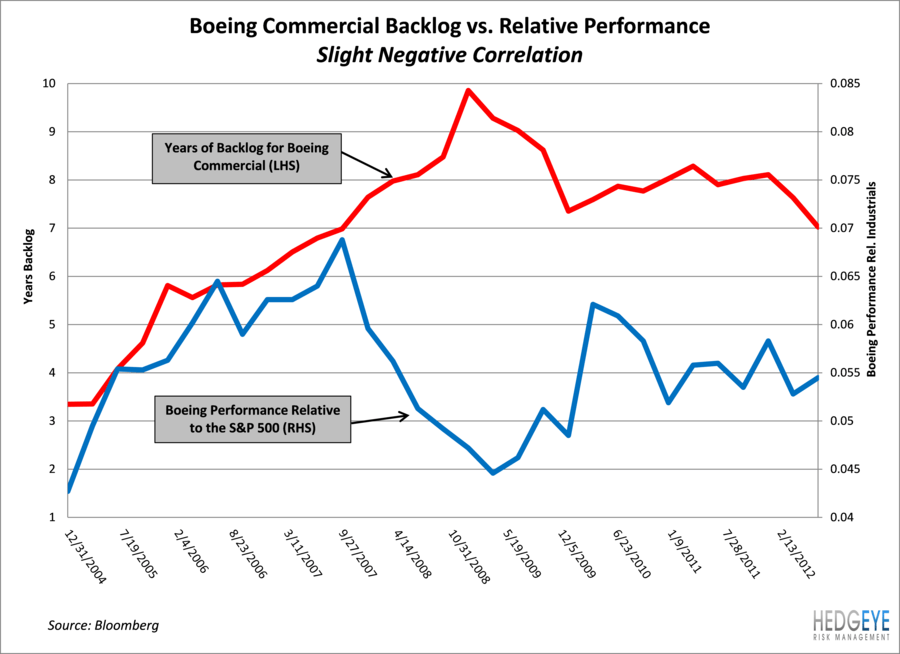

BA is not CAT: For those noting a slight decline in years backlog at Boeing Commercial Aerospace this quarter, that metric is negatively correlated with relative performance. A change in a 5 month backlog has more relevance than a change in a 7 year backlog. Though we are well into the commercial aerospace cycle, we think Boeing still has room to run.