In an effort to evaluate performance and as a follow up to our YouTube, we compare how the quarter measured up to previous management commentary and guidance

OVERALL

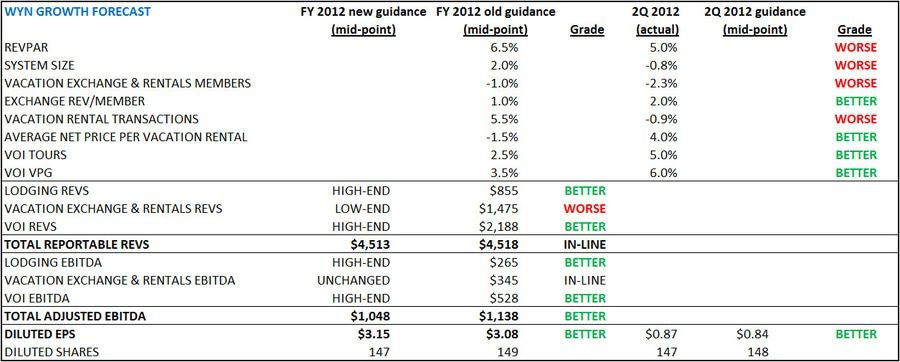

- BETTER: WYN produced a 2 cent beat over prior guidance and continued to deliver on their promise of returning cash to shareholders

EUROPE RENTAL BUSINESS OUTLOOK

- LITTLE WORSE: Excluding the impact of currency, the quarter was flat YoY on a SS basis. Rentals transaction volume was down though but constant currency increases in price per transaction were better due to mix.

- PREVIOUSLY: “We continue to see a stable environment for our rental businesses over in Europe. We've said that that's what we expected. When we entered the year, we said that's what we saw through the first quarter after the first quarter call, and now with April and May in the books, we'll see the exact same thing."

VPG GROWTH

- BETTER: 2Q VPG was 6% higher, ahead of FY2012 guidance of +3.5%. Management says it’s likely that VPG will come in close to the top-end of the 2-5% guidance range for 2012. Business is still on pace to add 27k new owners in 2012.

- PREVIOUSLY:

- “We had expected kind of a mid-single digit VPG growth and we ended up with a, I think, 11% VPG growth for the first quarter. We're not suggesting that that's the pace that we're going to remain at going forward.”

- We expect VPG growth to moderate somewhat throughout the year as we lap the rollout of the credit prescreening program. Consistent with last year, we expect to add 27,000 new owners in 2012.

TIMESHARE CAPEX STRATEGY

- SAME: Management still expects to spend about $125MM developing timeshare for the foreseeable future

- PREVIOUSLY:

- I don't see us going back, ever going back to the model we had before where we were building at a pace of $600 million of build a year in order to fuel the kind of growth that that business was on. Right now, we're spending $125 million a year to finish the development of inventory that we already have on our balance sheet. And that's a pace that we'll be at for the next eight to 10 years. And then after that we may go more heavily on this WAAM model and not even have that much development in the future

BUYBACK

- SAME: WYN repurchased 3.8MM shares for $190MM in 3Q and continues to see value in their stock at current levels

- PREVIOUSLY:

- We continue to believe that share repurchase offers a compelling return, and with the $750 million increase as of market close yesterday, we have $940 million available in our share repurchase program

APOLLO INITIATIVES

- SAME: We've made significant progress over the past two years with one of our key Apollo initiatives, brand.com. Revenue in room nights across the brand portfolio are up approximately 20% from this channel year-to-date in part due to improved content and Web functionality.

- PREVIOUSLY:

- Wyndham Hotel Group continues to make progress in executing its Apollo initiatives, which is a series of technology projects focused on improving our value proposition to franchisees. Our franchisees will be able to measure our results by the number of direct room nights we deliver to overall bookings, primarily through online strategy. Our goal is to capture the maximum amount of online traffic and then convert these online visitors to stay-in guest. Remember that the launch of our new hotel brand websites and improved content were the first step in our Apollo plan to drive more room nights through our online direct distribution channels. Preliminary results have exceeded our expectations with brand booking increases averaging over 10%

CONSOLIDATION OF RENTAL WEBSITES

- SAME: They launched the 2 planned initiatives on schedule; namely consolidation of their 23 ResortQuest rental sites into an single platform under the Wyndham Vacation Rentals brand umbrella and an integrated reservation platform for the UK cottage and parts brands.

- PREVIOUSLY: In the second quarter, we expect to launch two significant initiatives. First, in North America, we will consolidate 23 Rental websites into a single improved site. Second, in Europe, we will integrate the inventory and reservation platform of our UK cottages, parts and lodges brands into a common property management system, a change the will enable further yield management and operational efficiencies

IMPROVEMENT TO RCI ONLINE BOOKING CAPABILITIES

- SAME: Completed another successful launch of RCI.com with improved click to chat functionality. Expect online transactions to improve exchange margins by 225bps from where they were in 1Q 2008 when they started initiatives. In 2Q, 41% of transactions were booked online compared to just 13% when they started the project.

- PREVIOUSLY: The strength of RCI's technology continues to pay off with online transaction penetration growing to over 40%, up more than 400 basis points from last year.