Conclusion: This is the first chink in the armor for CRI. It’s still one of our top shorts.

- CRI beat and we won’t take it away from them. Carter’s wholesale revenue and profitability looked good, but the implication of lower margins in 2H is the first chink in the armor that we’ve been concerned about.

- They took down 2H EPS guidance to $1.58-$1.68, we were at $1.50 vs. the Street at $1.84 and we’re likely staying there.

- While wholesale looks good, the weaker than expected retail comps are a concern and is something that management is going to have to give an answer to on the call. Particularly due to the fact that as we’ve been saying, this is a brand with little delineation, or product differentiation by channel, which will impact owned-retail in the 2H.

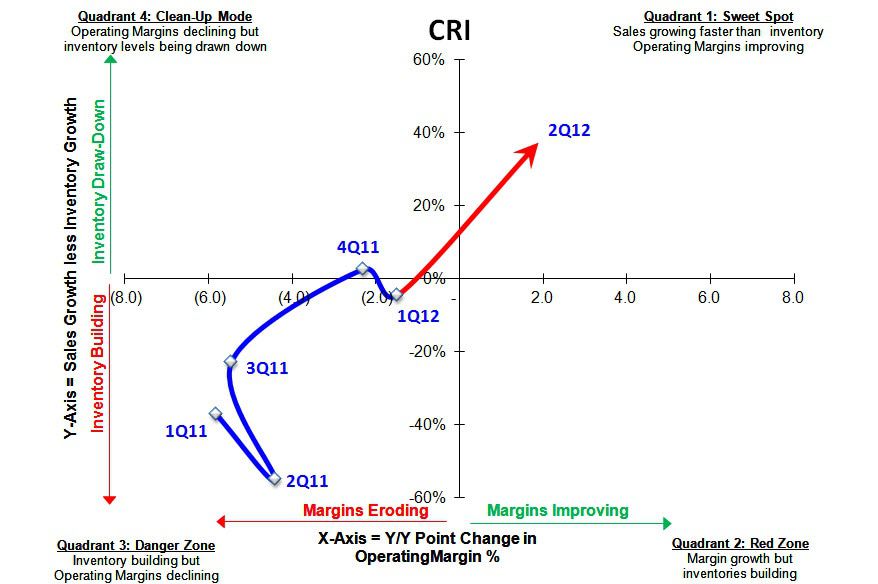

- Inventories looked good on a sequential basis, but keep in mind that the Bonnie Togs acquisition closed on the last day of the quarter last year. While reported inventories were down -18%, excluding BT they were up +11%. This still suggests a 14pt improvement in sales/inventory spread to +9%, but is not as gross margin bullish as implied.