“Without continual growth and progress, such words as improvement, achievement, and success have no meaning.”

-Benjamin Franklin

Last night I attended a launch party for the first book to be released from the Bush Institute, which is the non-for-profit that President George W. Bush started after leaving office. The launch was held at the Canadian Consulate in Manhattan, so I felt right at home. The book, for those of you who haven’t read the news clippings, is called, “The 4% Solution: How Can America Regain Its Economic Strength?”

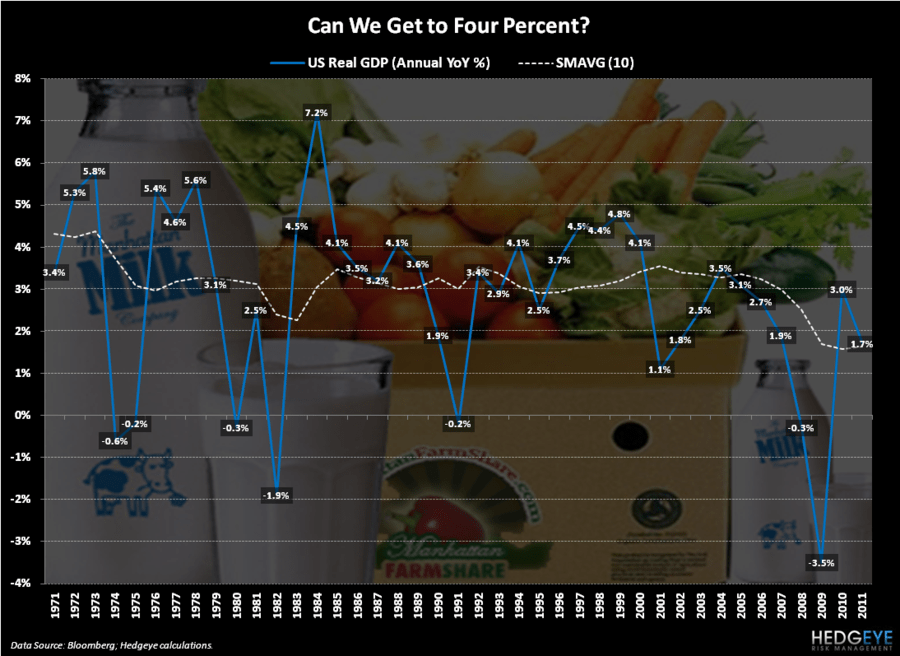

In the Chart of the Day, we show real year-over-year GDP growth going back to 1945. The moral of the story is that four percent GDP growth is no small task. Since World War II, the average year-over-year GDP growth in the U.S. has been right around 3%. Over the last decade, of course, it has been significantly lower.

In the forward to the book, the former President Bush makes no bones about the fact that growth began to slow under his tenure. In fact, he writes:

“While the causes of the 2008 crisis will be debated by scholars for decades to come, we can all agree that excessive risk taking by financial institutions, irresponsible decisions by lenders and borrowers and market-distorting policies all played a role. The question now is which policies should we adopt to fix the problems, speed the recovery, and lay the foundation for another long, steady recovery.”

Obviously, it is a worthy question, especially in the short term as we wake up to even more incremental data points that growth is and will slow both in the U.S. and globally. Some of these include:

1. Company specific reports – I’d like to include Apple in this since the company “disappointed” the consensus estimates of the Old Wall, but the reality is that Apple still sold 26 million iPhones (good for 28% year-over-year growth) and iPad sales grew more than 80% year-over-year. In aggregate, though, corporate earnings, especially on the top line where it matters, have been validating a slowing global economy.

2. European yields – Over the past couple of weeks, European sovereign debt yields in the periphery have gone to new highs. Specifically, Spanish 10-year yields, even if marginally off their highs of the morning, are north of the 7.5% line. The implication of this signal is that European governments need to do two things, both of which will slow growth in the short term, cut more spending and likely add more debt to their balance sheets to stay solvent.

3. Consumer confidence – The global economy is driven by consumer spending. The latest negative data point comes from South Korea. This morning South Korean consumer confidence fell to the lowest level in five months. Unless consumers globally have confidence, they won’t spend and economic growth will remain anemic.

Despite the global economic malaise that is being reinforced every morning, President Obama’s re-election chances remain relatively positive. In fact, a NBC News / Wall Street Journal poll out this morning shows that President Obama holds a 10-point lead on the question: who would make a better Commander in Chief? At the same point four years ago, a Pew poll showed that McCain led Obama on the same question by 15 points.

This perspective is confirmed by our Hedgeye Election Indicator that shows Obama’s re-election chances are at 57%. This corresponds with the Presidential predictive market at InTrade that shows a similar reading with Obama having a 57.3% re-election probability. So, what does Romney have to do to narrow this race? According to the partisan crowd last night, he has to move the discussion away from Bain Capital, focus entirely on the economy, and introduce a differentiated economic plan to get the U.S. economy back on a growth trajectory.

A consensus view of many of the economists last night, albeit they were more conservative leaning, is that economic policy will fail if it is thought of as a welfare policy. On some level, it is hard not to disagree with this point. While we harp on it daily, relying on government to be the solution is, in fact, the problem. To wit, I received a morning note today from a friend that runs a large institutional trading firm. His note led off by saying that European markets and U.S. futures are “holding on” in hopes of government / central bank action. How sad is that?

I’ll answer my own question: it is very sad. Nonetheless, we have to play the game in front of us. So for those of you who are looking for a government related catalyst of one kind or another, there are few dates to keep in mind:

- Aug 1st – Federal Reserve meetings in the U.S.;

- Aug 23rd – 25th – The annual central bankers confab in Jackson Hole; and/or

- September 13th – Federal Reserve meets again.

You want catalysts? We got catalysts!

Unfortunately, government induced catalysts don’t do much for inducing real and sustainable growth, even if they do at times arrest economic gravity. Although according to some recent analysis from our own Josh Steiner, even that point is questionable.

The most recent round of short selling bans in Europe made Josh look back at the last times governments intervened in the free markets to ban short selling. On August 8th, 2011, France, Italy, Spain, and Belgium banned short selling. The Euro Stoxx Bank Index went on to lose 21% over the next month. Even more noteworthy was the SEC short selling ban on September 8th, 2008 of the financial sector, which led to subsequent 76% decline in financials over the next six months.

So, what’s my plan for growth? For the central banks and central planning governments to do one thing: stop.

Our immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1, $99.45-103.98, $83.36-84.17, $1.20-1.22, and 1,

Best of luck out there today,

Daryl G. Jones

Director of Research