Conclusion: A great print from UA. One of the few companies to up guidance without any mention of the words economy’, ‘slowdown’ or ‘headwinds’. We were concerned about a potential CMG scenario headed into this print and hedged our positive TAIL exposure. That caution was misplaced.

- Great, clean quarter from UA – definitely did not pull a CMG or NKE, which was a distinct possibility.

- Revenue was in-line with our estimate of 28% growth – 600bp better than the Street.

- To our surprise, there were literally no cautionary statements thrown out by management about economic headwinds. In fairness (and in irony), part of UA’s resilience is due to its own failure to penetrate International markets to date. But regardless, the lack of any form of caution is clearly noteworthy. International remains only 5.6% of sales, down slightly from 1Q and up 80bps from ly.

- Direct to consumer revenue is up to 29%. Nike is drooling over this staggering statistic. This is a stealth part of this story that people are not focused enough on.

- The company is maintaining its 300bp-500bp estimate for EBIT growth above revenue growth – but on a 200bp-300bp better top line growth rate (22%-24%).

- UA took up the year by $20mm in revenue guidance, despite beating 2Q by $12mm. Granted, it did not provide this 2Q guidance. So for all we know the consensus simply printed a number below a conservative plan. But still, this delta is notable.

- Footwear came in guardedly positive. Top-line growth was 44%, but the 2-year comp accelerated by 16 points to 37%.

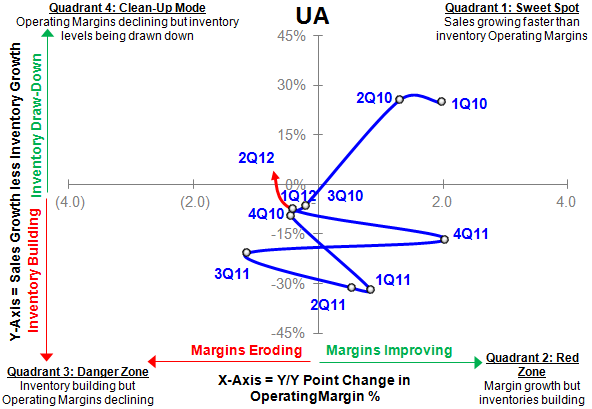

- The balance sheet clearly improved, with the sales/inventory spread poking its head in positive territory for the first time in 7 quarters, which is gross-margin bullish for 2H.

- Tough to poke holes in this one.