JCP is pulling one of its levers – i.e. monetizing the majority of its REIT portfolio – to get the cash they’ll need. Chances are they’ll need to do it again while Ron Johnson & Co. work to right-size the ship, but we’re not going to beat them up for monetizing an investment that’s up +30% over the past year. To be fair, it’s the smaller of the two with JCP’s real estate worth an estimated 7x-10x more, but notable in that JCP’s next step should it need additional cash will be to monetize at least some portion of its real estate portfolio.

Here’s some context on the sale of JCP’s Simon holdings today:

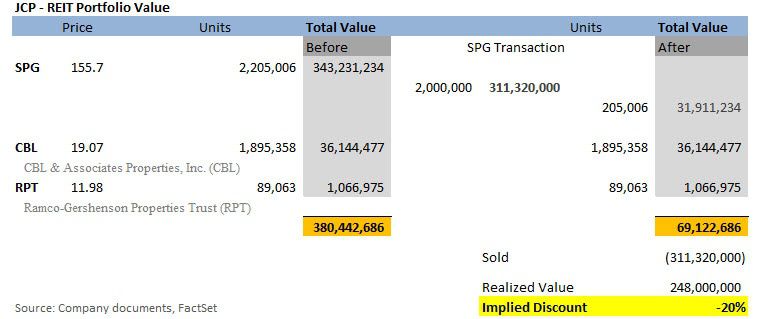

Structural impact:

- The value of JCP’s REIT portfolio accounted for nearly 6% of overall EV at ~$380mm, now = ~1%

- JCP has a stake in 3 REITs listed below with SPG accounting for ~90% of entire portfolio

- They sold ~90% of that stake today (still own 205k units – had owned 2.2mm)

- Proceeds of the deal of $248mm are at a 20% discount to market value of $311mm and = ~$1.13 in value/share

- This will be modestly offset by SPG’s $1/share dividend that has generated $2mm in annual Pretax profit (less than $0.01 in EPS)

FCF impact:

- JCP guiding to $1bn in CFFO and $800mm in CapEx in 2012 = ~$200mm in FCF

- Over last 5yrs, JCP has generated less than $200mm in FCF in 4 of 5 years

- In 2011, JCP generated negative FCF of -$50mm

- This deal will provide a ~$250mm cushion. Keep in mind, when they report earnings in another 3-weeks they will have likely burned through ~$1Bn in free cash flow (nearly $700mm in Q1) - so they need it

What this means for JCP:

Realizing $1/share in value will likely offer some support to the stock over the immediate-term. But with the value of the operational retail business eroding in value, it’s worth revisiting the value of JCP’s primary asset in the event it too gets monetized.

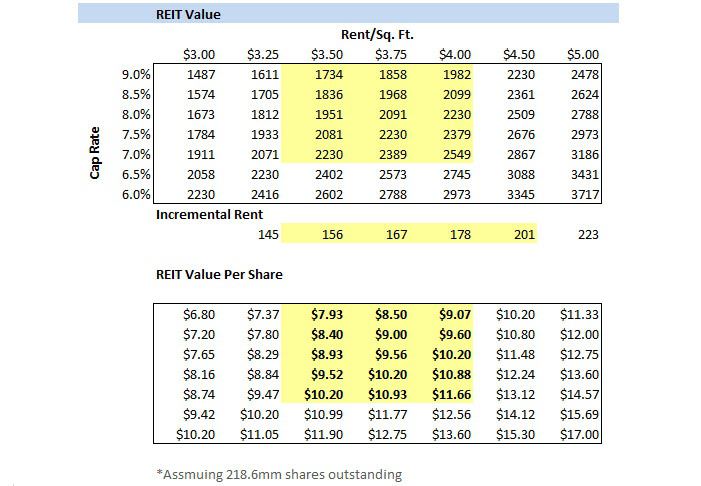

With Cap rates in the high 7%s and taking into consideration the lower end of the average rent these locations typically command – in the $3.25-$4.00 rent/sq. ft. range, we think JCP’s real estate portfolio is worth $1.8-$2.1Bn in value or $7-$9 per share. This equates to 40%-50% of JCP current market value of $4.4Bn making this asset increasingly more relevant with the stock hovering around $20.

To be clear, this scenario would not be a positive event as it would suggest the need for additional capital inflow implying further erosion in the core retail business. But it does remain an option nonetheless given JCP owns ~40% of its current store base.