“Comanches adapted to the horse earlier and more completely than any other plains tribe.”

-S.C. Gwynne

Man is competitive. So am I. As a team, we wake up to this world every risk management morning looking for a better way. That’s progressive. That’s how we evolve as a people. Anyone in this profession who does not get this will be left behind.

The aforementioned quote comes from the American Indian history book I have recently cited, Empire of The Summer Moon. It’s a stiff reminder of how harsh life has been. Not every man who attempted to settle in 18th century Texas was given a sticker.

Since launching our Q3 Global Macro Themes in early July, we’ve been riding the same horse that has had us calling for #GrowthSlowing since March. Our horse uses modern day math and machines. We don’t ask the Old Wall for permission to make calls on the direction of Growth Slowing’s Slope. We let Mr. Macro Market tell us which way our horse needs to ride next.

Back to the Global Macro Grind…

Evidently, shorting the SP500 at its 1375 TREND level was a better than bad risk management decision to make. Friday’s -1% selloff in the US stock market came on the heels of both Spain and Italy closing down -6.3% and -4.7%, respectively, week-over-week.

Not to be confused with the fictional storytelling that global growth is “decoupling”, one of our most stealth front-running horses of Global Economic Growth, South Korea’s KOSPI index, told us the same story as structurally impaired Western Europe did. The KOSPI was down -4.3% week-over-week, testing its YTD lows.

This morning, neither Asian nor European Equities are telling you that anything about #GrowthSlowing has changed. Neither is the US bond market. Nor are corporate revenues. Neither are the prices of oil and copper.

Before I come back to touching dogmatic taboo of “growth is fine and earnings are great”, let’s grind through some of the aforementioned risk management signals:

- US Equity Futures down 14 handles

- Japanese Stocks (Nikkei 225) = -1.9% (down -17% since March, remaining in a Bearish Formation)

- Chinese Stocks (Shanghai Comp) = -1.3% (down -13% since May, remaining in a Bearish Formation)

- Hang Seng -3.0%, KOSPI -1.8%, and India’s Sensex -1.4% (all Bearish Formations)

- European Stocks (EuroStoxx50) = -2.2% (down -16% since March, breaking TREND again)

- Spanish Stocks (IBEX) = -4.3% (crashing, down -33% since March)

- Italian Stocks (MIB) = -3.3% (crashing, down -26% since March)

- Russian Stocks (RTSI) = -3.2% (crashing, down -23% since March)

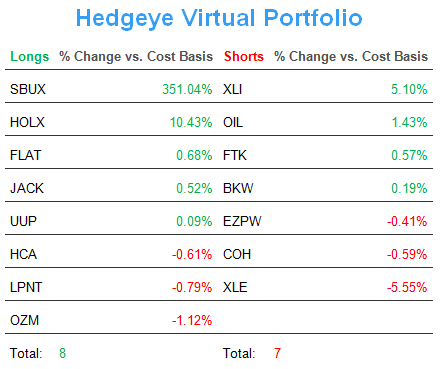

- Oil (Brent) = -3.2% (backing off hard from where we shorted it on Thursday)

- Copper = -2.7% (backing off at its intermediate-term TREND line of 3.64/lb, much like the SP500 did)

- Treasuries (UST 10yr) = down another -5bps this morning to 1.41% (new lows)

- Yield Spread (10s minus 2s) = down another -6bps this morning to 120bps wide (narrowest YTD)

- Euro (vs USD) = down, again, testing $1.20 (after snapping its 2010 lows last week and now confirming)

I’ll stop there, at lucky thirteen.

How about that beloved “earnings season”? With almost 200 of 500 companies in the SP500 having reported, at least 50% of them have already missed on revenue expectations (worst quarter since 2008). Two of the key Sectors in the SP500 (Financials and Industrials) look nothing like the “SP500 is flat for July” as they are down -1.8% (XLF) and -1.4% (XLI) for the month-to-date.

Oh, but never mind the revenues, ‘earnings are good.’ Really?

- Earnings are lagging indicator (not a leading one) anyway

- Revenues are leading indicators for Growth Slowing’s Slope

As our everything Financials guru, Josh Steiner, wrote in his research note to clients on Friday afternoon, the expectations mismatch between “reported” earnings and revenues is widening to the bearish side of Growth’s Slope:

1. EPS: 17 out of 33 companies (52%) have beat consensus EPS estimates, while 11 were in line, and 5 have missed. Keep in mind that we are looking at the optical (unadjusted) numbers.

2. Revenues: 6 out of 33 companies (18%) have beat consensus revenue estimates, while 20 were in line and 7 missed. For reference, we consider 2% or greater above the estimate a beat.

In other words, whether it’s GDP in Spain or the top line revenues of a company, get Growth’s Slope right, and you’ll get a lot of other things less wrong.

Oh, and if you’re in a performance foot race and want to be right instead of less wrong, ride a Global Macro horse.

My immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, and the SP500 are now $1, $103.01-108.16, $83.18-83.99, $1.20-1.22, 5, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer