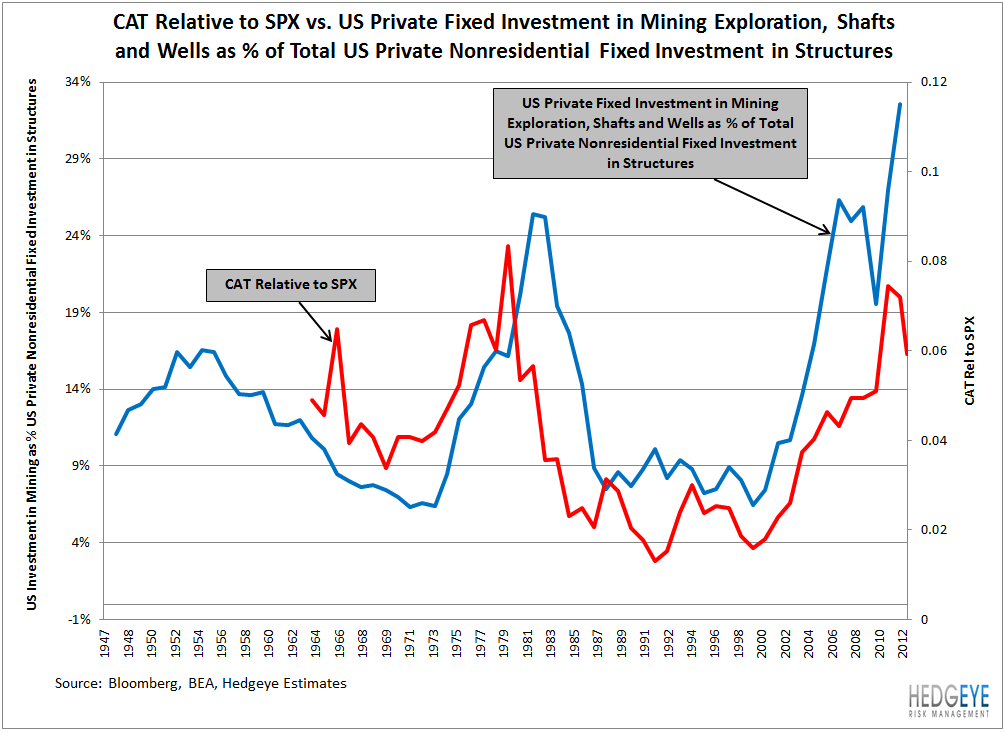

Chart of the Day: CAT in 70s Resource Investment Bubble

- Investment in mining and resources in the US and globally at cyclical highs, which has helped capital equipment producers like CAT.

- Below, we can see what happened to CAT when the 1970s resource investment boom gave way

- CAT upped its exposure to these markets with the acquisition of Bucyrus last year, at what looks like the peak of resource investment spending

- If history rhymes in this investment cycle, CAT holders may be looking at years of relative underperformance