McDonald’s is releasing 2Q12 earnings before the market open on Monday morning. Investors will be listening keenly for commentary on the global economy. Our view is that MCD is likely to miss the Street’s expectations for sales in June.

On April 24th, 2012, we wrote, “we see plenty to be concerned about” regarding McDonald’s top-line trends going forward. Price is running at roughly 3% in the United States and 2-3% in Europe. While the price points at McDonald’s are compelling for consumers relative to much of the competition, when we consider that Food Away from Home CPI in the U.S. is running at ~3% this year, McDonald’s may be taking less share this year on account of its price points than in years past. The company is now pricing in line with Food Away from Home CPI whereas last year, that difference was roughly -50 basis points. We remain unconvinced that traffic trends will be sufficient to bring the overall June comp in line with consensus for the U.S. division.

Callout

On the topic of "Growth Slowing", which Hedgeye Macro was ahead of the competition on, we want to highlight the two charts below. We won't be calling comps on a month-to-month basis on the back of these charts, the numbers are trailing twelve month averages, but they clearly highlight how economic activity does impact the fundamental performance of the McDonald's business.

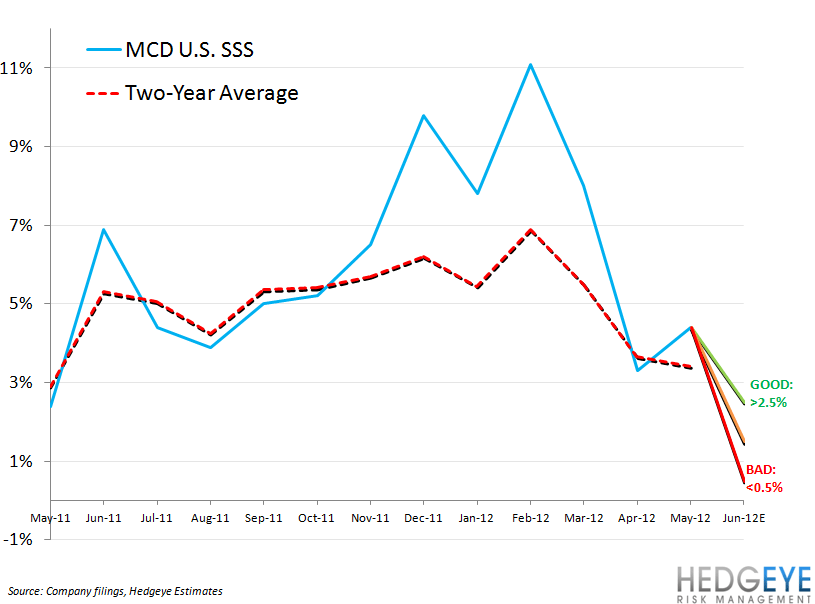

Below we go through our take on what comparable restaurant sales numbers will be received as good, bad, and neutral by investors. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to June 2011, June 2012 had one less Wednesday, one less Thursday, one additional Friday, and one additional Saturday. We expect a positive calendar shift impact in McDonald’s June results.

U.S. – facing a difficult compare of 6.9%, including a calendar shift of between 0.2% and 0.5%, varying by area of the world:

We expect that MCD U.S. same-restaurant sales grew +1.0-1.5% in June.

GOOD: A print of higher than 2.5% would be strong results, in our view, as it would imply a sequential acceleration in the calendar-adjusted two year average trend. Commentary across the restaurant space indicates that the operating environment for restaurant companies has been deteriorating in the United States. While a +2% print would imply negative traffic/mix, we believe that investors are taking that as a given considering the extremely strong traffic trends posted last year as a result of the beverage line offering.

NEUTRAL: A print of +1.5% would be considered a neutral result as it would imply roughly flat calendar-adjusted two-year average trends on a sequential basis.

BAD: A result of less than +1.5% growth in same-restaurant sales would imply a significant slowdown in two-year average trends on a calendar-adjusted basis and would likely cause the stock to sell off further. While we do believe that McDonald’s sales trends are slowing, we do not believe that the number will be below +1%.

Europe - facing a difficult compare of +9.1%, including a calendar shift of between 0.2% and 0.5%, varying by area of the world:

We expect that MCD Europe same-restaurant sales declined by between -1% and -1.5% in June.

GOOD: A positive same-store sales number would, in our view, be positive for MCD Europe as it would imply a sequential acceleration in calendar-adjusted two-year average trends. Other companies in the consumer space have cited lower-than-expected sales lift from the Euro 2012 soccer tournament.

NEUTRAL: A print of between -1% and 0% would be considered a neutral result as it would imply two year average trends picking up slightly from trough levels in May. Investors will be eager to see some stability in the Europe business’ trends.

BAD: Same-restaurant sales below -1% would imply little or no sequential improvement in calendar-adjusted two-year average trends from low levels in May.

APMEA - facing a compare of +4.8%, including a calendar shift of between 0.2% and 0.5%, varying by area of the world:

We expect that MCD APMEA same-restaurant sales grew by +1% in June.

GOOD: Same-restaurant sales growth of more than 1% would be a strong result, in our view, because it would imply a sequential acceleration in the calendar-adjusted two-year average trend following three consecutive months of decline. Macro concerns around China were assuaged, to a degree, by YUM meeting analyst expectations of 9.8% comps in 2Q with a 10% print.

NEUTRAL: A print between 0% and 1% would be a “neutral” result as it would imply a sequential stabilization of two-year average trends. That said, the low level of growth would remain a concern.

BAD: Comparable restaurant sales growth below 0% for McDonald’s APMEA division would imply a continuation of sluggish two-year average trends.

Howard Penney

Managing Director

Rory Green

Analyst