If you’re thinking of investing in bank stocks, you should understand net interest margin, or “NIM” for short. It refers to the dollars of interest income less the dollars of interest expense divided by the average interest earning assets in the period. This is a very important metric for us when we look at the health of the big banks like Bank of America (BAC), JP Morgan (JPM), etc. When a company’s NIM changes, even by a few basis points, it puts a hurting on earnings power.

Take Bank of America, for example, who saw its NIM compress 30 basis points quarter-over-quarter. Per Hedgeye’s Managing Director of Financials Josh Steiner:

“To put this in perspective, the company lost $1.27 billion in quarterly earnings power, or roughly $5 billion in annual earnings power in just one quarter! On a per share after-tax basis, that works out to $0.34 cents in full-year earnings per share. While that may not sound like a lot, Bank of America is only expected to earn $0.55 in 2012 and $0.94 in 2013, so taking a hit of $0.34 in a single quarter is big deal. Remember, that hit is recurring, not one time.”

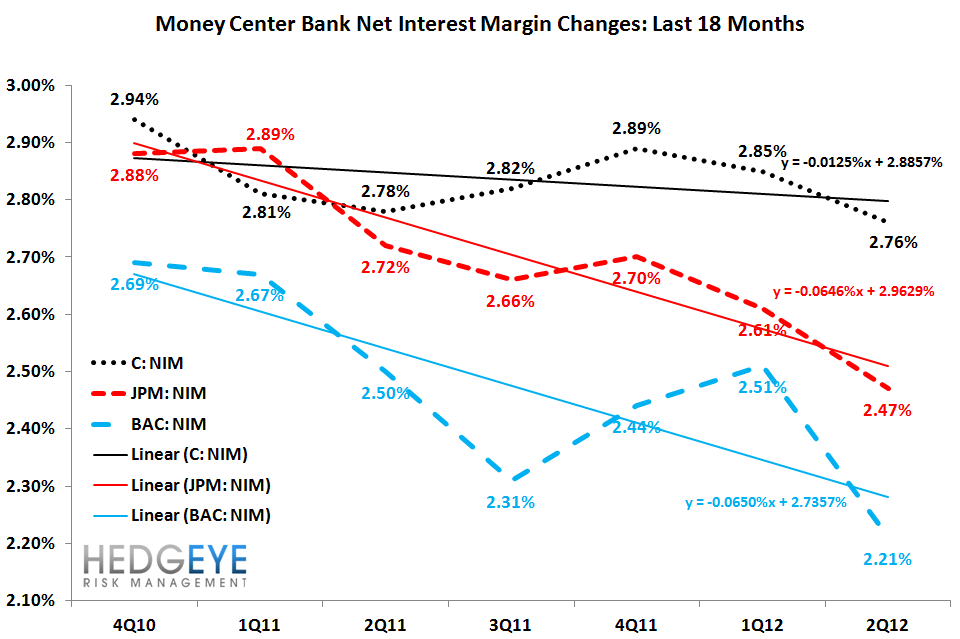

The above chart represents the six quarters “performance” of NIM for some of the biggest banks out there. It gives you an idea of why banks’ earnings are getting squeezed as NIM compresses; they’re essentially losing out on a big chunk of money every report.

On the macro side of things, remember that we’re currently in a low-yield, low-rates environment courtesy of the Federal Reserve. Ever heard of bankers doing 3/6/3? Borrow at 3%, lend at 6%, be on the golf course by 3pm. That doesn’t really work the same way anymore. It’s harder to earn interest in this environment and there’s no longer a 300 basis point spread like there used to be back in the day.

What’s the end game to all this?

So long as the long end of the curve keeps falling (which it is), and banks remain asset sensitive (which they are), then you should reasonably expect to see NIM come under greater and greater pressure, which, in turn, puts pressure on bank earnings. Bank earnings, NIM – remember to keep your eye on this come Q3.