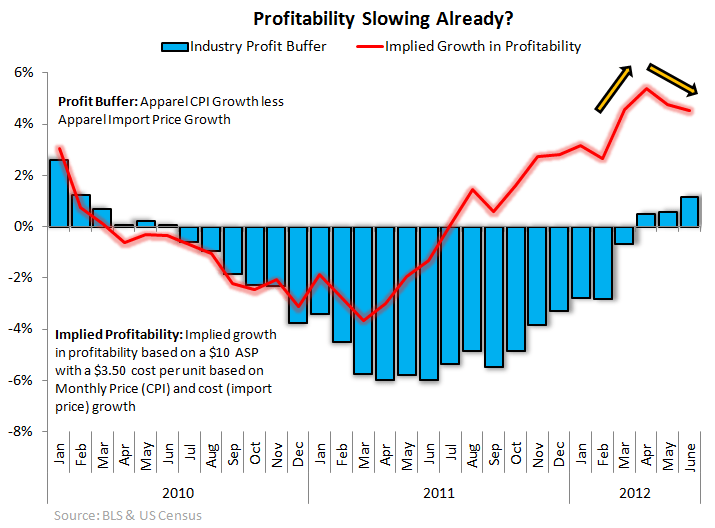

The shift in the delta between costs and prices suggests that profitability is slowing sequentially.

A 120bps sequential slowdown in the Apparel import price index (+2.7% in June vs. +3.9% in May) seems bullish in the face of a 50bp slowdown in Apparel CPI (+3.9% yoy in June relative to +4.4% in May). But that's not so.

The average retail price of a unit of apparel is about $10 while the cost is only $3.50. So a 50bp slowdown in price equates to ($0.50) per unit, while a 120bp slide in cost is +$0.42. That's a net negative $0.08 per unit.

This is not a doomsday scenario, but it is an incrementally negative change that most CEOs could care less about -- until they have to.