JP Morgan (JPM) reported its second quarter earnings last week while still reeling from the London Whale trading loss (now amounting to $5.8 billion). Profits fell 9% and one of the worst trades of all time could balloon to $7 billion.

But the real story here isn’t the London trading loss. There are other gears in motion that do not help JP Morgan out in the long run. The LIBOR scandal that continues to plague the industry will soon spill over to JPM (along with Citigroup and Bank of America) and overall weakness in capital markets is a sign of the times.

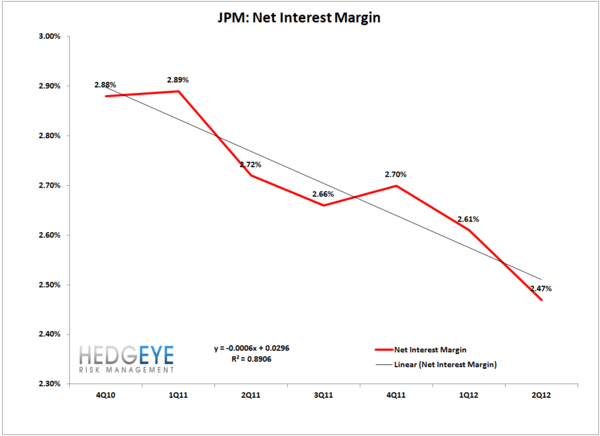

Revenues are coming under pressure and expenses are growing. The efficiency ratio is the total expenses as a percentage of total revenue – take a look at the chart we’ve provided for the full story. Expenses are catching up and quickly. The stock was up 5 to 6% on Friday. We look at the results and are asking: are they really that great? They cut guidance. Four months ago at investor day, they said that operating expenses would fall 1 to 2% in the back half of 2012. Now they say that they’re going to be flat.

The story here is that while JPM is cheap relative to earnings, the company (and industry) as a whole faces significant challenges in the back half of the year. The data says it all.