This note was originally published at 8am on July 02, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“I only regret that I have but one life to lose for my country.”

-Nathan Hale

The quote above from Nathan Hale is by many thought to be one of the more patriotic statements made in American history. These words were spoken by Hale shortly before being hung by the British for spying. The 21-year old Yale graduate had been captured by the British after volunteering to go behind enemy lines to report on British troop movement during the Battle of Long Island. Clearly, a willingness to sacrifice your life for your country is the ultimate sacrifice.

Yesterday was Canada Day in Canada and Wednesday will be Independence Day in the United States. While most of us won’t be swearing to give our lives for our respective countries this week, for many of us our patriotism will nonetheless be on display. In many ways, patriotism is a great thing. On the other hand, extreme patriotism is in many instances the root of the more significant military conflicts in modern history. Ultimately at the root of patriotism is a deep seated perspective that your nation’s interests should come ahead of another nation’s interests.

The global equity markets have rallied aggressively over the last couple of days based on perceived positive developments from the European Union summit last week. This is the 20th summit since the European sovereign debt crisis began in 2010 and the ensuing storyline has become somewhat predictable. The leaders of the European Union meet, stories are linked about the possible bailout plans that are in the works, numerous MOUs are signed or agreed to at the end of the summit, and then the markets rally in anticipation of the end of the crisis. Eventually, though, market participants again realize there is no solution and that crisis is far from over. But who knows, perhaps this summit truly was different. Personally, I remain a skeptic.

The ultimate solution in Europe must come from a broad willingness for nations to give up sovereignty on fiscal and budgetary matters. As discussed above, national pride and patriotism run deep, particularly in Europe, therefore relinquishing even some sovereignty for collective fiscal and budgetary decisions will not be an easy matter. So, even if the headlines coming out of the most recent summit are positive, we need to keep in mind that any actual implementation of a broad based solution will not be simple, or quick.

On the economic data front, the Purchasing Managers Index for manufacturing in Europe came out this morning at 45.1. This is the 11th monthly decline and the rate of decline was comparable to that of May, which was the fastest monthly decline in almost three years. Overall, the average reading of 45.4 was the slowest reading since Q2 2009. Most disturbing is likely the fact that Germany is clearly no longer immune from growth headwinds as German PMI came in at 45.0 for the fourth consecutive month of declines. All in all, pretty somber news as it relates to growth, or lack thereof.

The larger emerging issue from Europe’s structural growth problem is that of unemployment. In May, the Eurozone unemployment rate came in at a new record of 11.1% with more than 17 million people unemployed in the 17-nation Eurozone. Consistent with its victory in the European Cup over the weekend, Spain continues to also lead on the unemployment front with unemployment at 24.6%, though is followed closely by Greece at 21.9% and Portugal at 15.2%. There is no question given the current state of the European Union, as most recently indicated by the PMI numbers outlined above, that we have not yet seen highs in unemployment.

Later this week both the European Central Bank and the Bank of England will meet and then give their most recent rate decisions. Similar to the Federal Reserve, both of these central banks are largely out of bullets. It is expected that both banks will cut rates by 25 basis points and approve a 50 billion pound bump in the asset purchase program, respectively. Based on the move we’ve seen in European equities and bonds in the last few days, it seems likely that even coming in line with expectations may actually be a disappointment.

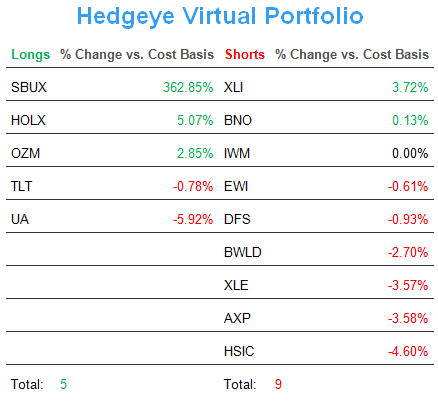

We continue to be very conservatively positioned in both the Hedgeye Asset Allocation Model with 91% cash and in the Hedgeye Virtual Portfolio that now has 5 longs and nine shorts. So, yes, we are now running net short in the Virtual Portfolio as Keith added the following shorts in Friday’s melt up: Discover Financial Services (DFS), Italian equities (via the etf EWI), the Russell 2000 (via the etf IWM), and Brent Oil (via the etf BNO).

As you head into July 4th and celebrate American independence with your friends and family, and despite some of the somber economic news coming out of Europe, it is important to remain optimistic and upbeat. As such, I’d like to leave you with quotes from two American Presidents, a Republican and a Democratic. They are as follows:

“There is nothing wrong with America that cannot be cured with what is right about America.”

-President Bill Clinton

“America has never been an empire. We may be the only great power in history that had the chance, and refused – preferring greatness to power and justice to glory.”

-President George W. Bush

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Germany’s DAX, and the SP500 are now $1583-1623, $92.82-97.66, $81.21-82.16, $1.25-1.27, 6269-6563, and 1336-1365, respectively.

Enjoy your holiday time this week.

Best,

Daryl G. Jones

Director of Research