TODAY’S S&P 500 SET-UP – July 16, 2012

As we look at today’s set up for the S&P 500, the range is 27 points or -1.38% downside to 1338 and 0.61% upside to 1365.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/13 NYSE 2044

- Up versus the prior day’s trading of -792

- VOLUME: on 07/13 NYSE 683

- Decrease versus prior day’s trading of -10.58%

- VIX: as of 07/13 was at 16.74

- Decrease versus most recent day’s trading of -8.67%%

- Year-to-date decrease of -28.46%

- SPX PUT/CALL RATIO: as of 07/13 closed at 1.62

- Up from the day prior at 1.31

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 36

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.48%

- Decrease from prior day’s trading at 1.49%

- YIELD CURVE: as of this morning 1.25

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, July, est. 4 (prior 2.29)

- 8:30am: Advance Retail Sales, June, est. 0.20% (prior -0.2%)

- 9:30am: IMF releases updates to global economic forecasts

- 10am: Business Inventories, May, est. 0.2% (prior 0,4%)

- 11am: Fed to purchase $1.5b-2b notes maturing Aug. 15, 2022- Feb. 15, 2031

- 11:30am: U.S. to sell $30b 3-mo bills, $27b 6-mo bills

- 7:30pm: Fed’s George speaks on monetary policy and farmland values in Kansas City

GOVERNMENT

- President Obama holds campaign event in Ohio

- Senate in session, House not in session

- Dominion Resources CEO Thomas Farrell speaks at House Energy panel field hearing on proposed EPA greenhouse gas new source performance standard for utilities, 9am

WHAT TO WATCH:

- Citigroup to post 2Q results; watch investment bank, trade rev.

- Sales at U.S. retailers probably rose 0.2% in June

- U.K. FSA Chairman, Barclays ex-COO to testify at House of Commons committee on Libor-rigging scandal

- IMF to revise global growth forecasts; Lagarde has said forecasts will be lowered from April’s 3.5% projection

- Glaxo raises Human Genome bid to $14-shr: Reuters

- Visa, MasterCard in settlement w/ total value $7.25b on merchants’ antitrust swipe-fee suit; convenience-store assn. rejects settlement, Natl Retail Fed. says not party to suit

- Calpers to release preliminary performance results for past yr

- WTO set to issue ruling on U.S. complaint against China’s restrictions on U.S. electronic-pymt svc suppliers, 10:30am

- Trial of SEC vs. Brian Stoker, former Citigroup dir., begins

- Weekly agendas: Finance, Tech, Media/Entertainment, Industrials, Energy, Transports, Health, Real Estate, Consumers, IPOs, Rates, Canada Mining, Canada Oil & Gas

- Bernanke testifies, China housing, Google: Week Ahead

EARNINGS:

- Citigroup (C) 8am, $0.89 - Preview

- Gannett (GCI) 8:15am, $0.53 - Preview

- JB Hunt Transport (JBHT) 4pm, $0.66

- Cintas (CTAS) 4:07pm, $0.60

- Brown & Brown (BRO) 4:50pm, $0.31

- Packaging Corp. of America (PKG) 5pm, $0.46

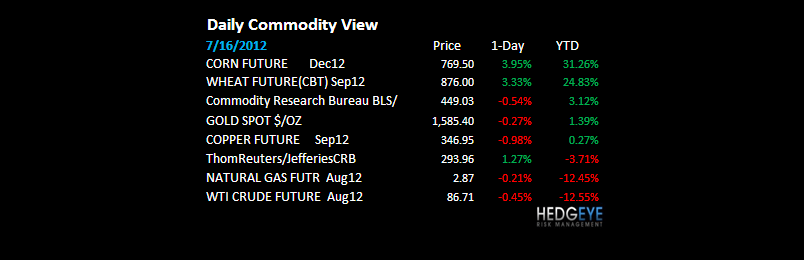

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Funds Bet Right Before Longest Winning Streak: Commodities

- Speculators Cut Bullish Oil Wagers Before Rally: Energy Markets

- Wilbur Ross Says U.S. Coal Is Facing Years of Headwinds: Energy

- Corn at 10-Month High, Soybeans Costliest Since 2008 on Drought

- Oil Declines From One-Week High on China Slowdown, Hormuz Bypass

- Sugar Falls as Producer Supplies Seen Advancing; Cocoa Declines

- Worst-in-Generation Drought Dims U.S. Farm Economy Bright Spot

- Gold Set to Fall in London as Europe’s Debt Crisis Aids Dollar

- Soybean Meal Surges to Record as Drought Withers U.S. Harvest

- Copper Drops for First Day in Four on China Consumption Concern

- Gold Demand in India to Drop as Buyers Prefer to Hoard Cash

- Gulf Oil Less Crucial in Storms as Shale Grows: Chart of the Day

- BP Said to Buy Fuel Oil Cargo From Hindustan Petroleum for July

- Ghana’s Cocoa Mid-Crop May Be as Much as 80,000 Tons This Year

- Deficient Monsoon Challenges India’s Record Food Grain Harvests

- Soybeans May Set Record, Break Resistance: Technical Analysis

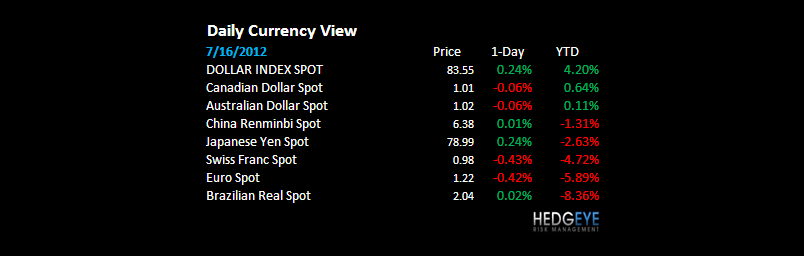

CURRENCIES

EURO – failed to hold Friday’s no-volume gains and is also failing to hold the 2010 closing lows; the Euro could go a lot lower; and the USD a lot higher (see our Q3 Macro Theme slides for the update on why); refreshed risk range for EUR/USD = 1.20-1.23

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – Friday’s no-volume USA rally on the lowest consumer confidence print in 7 months was based partly on a rumor China was going to cut again this weekend – but they didn’t, and Chinese stocks got cut to fresh YTD lows, down another -1.7% after Wen said that it needs to be “clearly understood” that #GrowthSlowing is accelerating on the downside.

MIDDLE EAST

ISRAEL – jumping off my risk factoring page this morning for reasons I am not sure of (down -0.6% testing new lows at -3.2% YTD) with plenty of rumoring by the British on possible “attacks” (Iran); something to think about re Oil (+3.1% last wk) keeping a bid during the USD’s recent upswing; middle east tension has been out of the mainline news for a while now.

The Hedgeye Macro Team