No Current Positions in Europe

Conclusion: the deposit level inflection is noteworthy, yet a long way from a signal of credit expansion

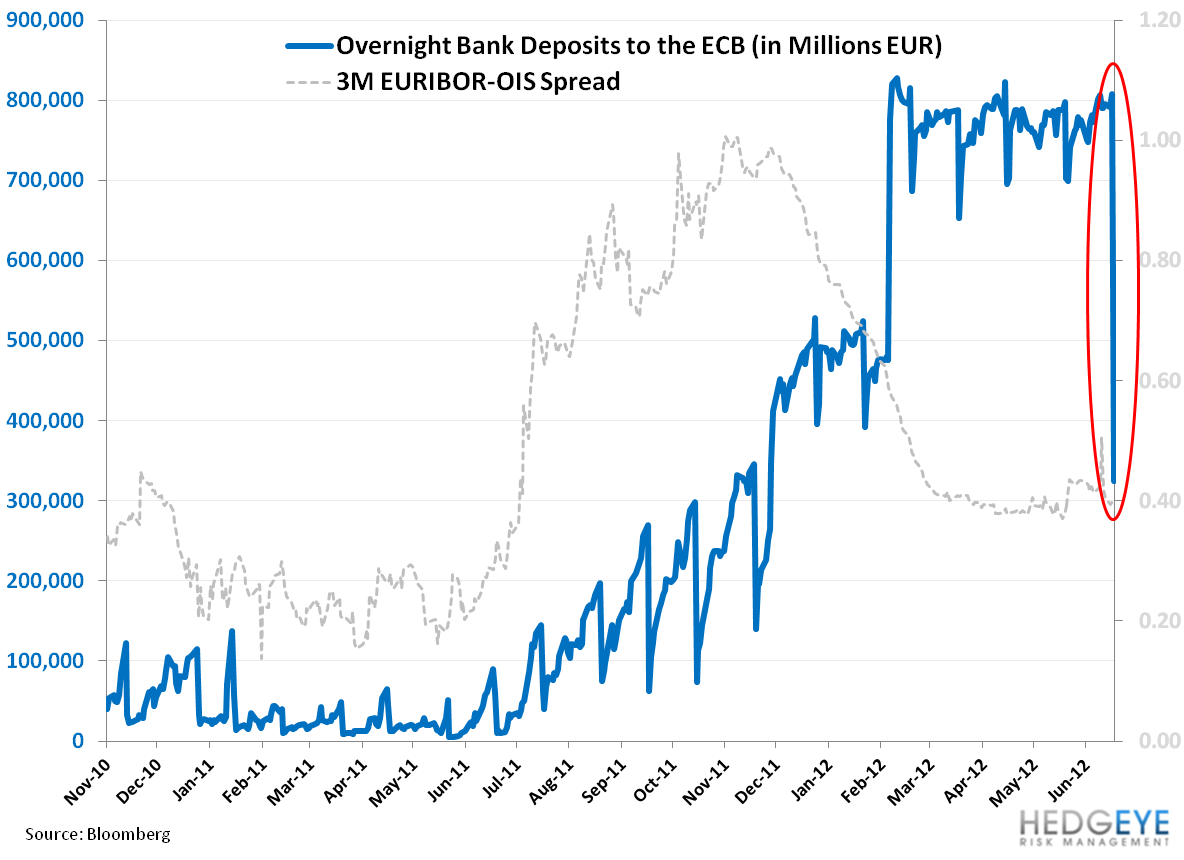

There was a notable inflection in deposits held at the ECB’s overnight window yesterday, the first day the central bank’s recently announced 0.00% deposit rate went into effect. As we show in the chart below, deposits fell from €808.5B on Tuesday to €324.9B on Wednesday (down -60%), according to the most recently reported figures from the ECB.

As a reminder, on 7/5 the ECB also cut the interest rate on the main refinancing operations by 25bps to 0.75% and the interest rates on the marginal lending facility by 25bps to 1.50%.

While on the margin, the decline in deposits, if sustained, could be a positive signal that funds are being “put to work” for broader public and private lending, we think the "pass-through" is inconclusive and that collectively the rate cuts issued by the ECB offer little incremental stimulus given how low rates already are.

Our view is that encouraging more borrowing through cheaper money is not the solution to Europe's problem of over-indebtedness.

To this end, we see the EUR/USD cross challenged over the intermediate term as there are no major planned catalysts on the calendar. Our call-out in the chart below is that the cross just broke through our TREND support line of $1.22. While we don’t see the cross going to parity, as we’d expect Eurocrats to step in to prevent it, the most recent news that Germany’s Constitutional Court could push out a ruling on the ESM and the fiscal pact until the fall (versus the original target of July 1), could add much consternation to the cross and European capital markets over the intermediate term. Our immediate term TRADE range is $1.21 - $1.24.

Matthew Hedrick

Senior Analyst