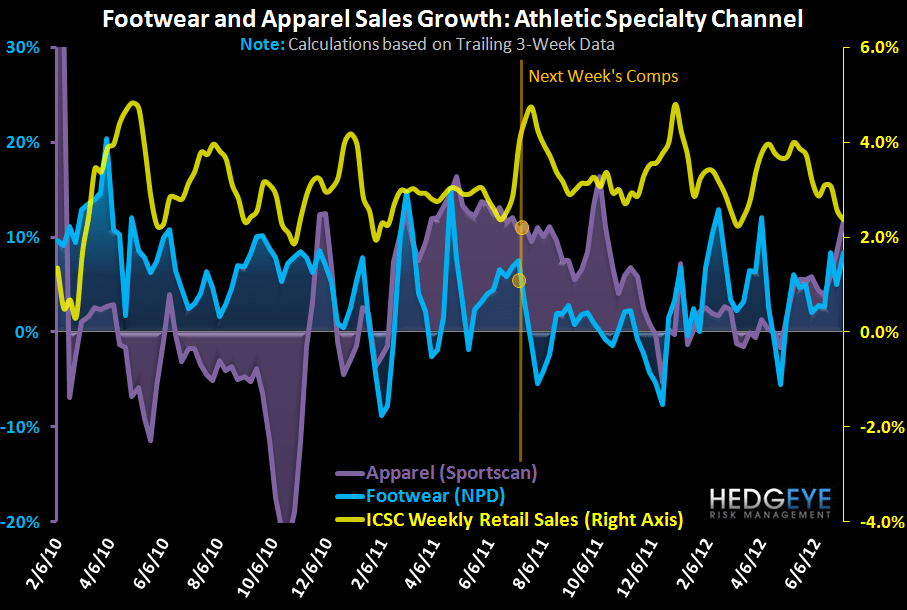

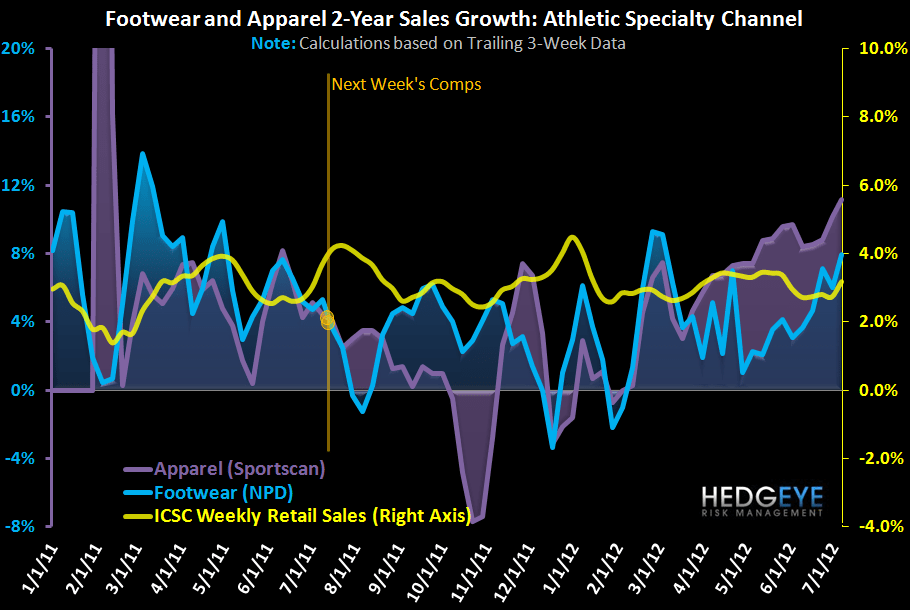

Athletic Footwear and Apparel sales accelerated into the first week of July. The month started off strong, on top of tough compares last year. Starting next week, both apparel and footwear yy comparisons become significantly more favorable. Underlying fundamentals would need to seriously erode in order to show disappointing headline results for the duration of the summer.