“I am the literary equivalent of a Big Mac and fries.”

-Stephen King

I’m not going to admit this because my brother is a McDonald’s franchisee. I am going to put it out there because this is really the key to what you really need to know this morning – I love the Big Mac!

As are all things here in the Haven, that’s a multi-factor, risk managed, statement. Not only do I eat Big Macs (weekly), but I wear the Big Macro jersey for Hedgeye with pride.

I am right fired up for our Big Macro Quarterly Themes Call this morning. We’ll be hosting it (49 slides in 40 mins) with the customary anonymous client Q&A at 11AM EST.

As a reminder, last quarter my team nailed the #GrowthSlowing and #BernankeBubbles popping (Gold, Oil, etc.) calls. I’d be lying to you if I said we weren’t looking to land a few fat TAIL risked whales this morning too.

Our Top 3 Themes are going to be as follows:

- Growth Slowing’s Slope – what our GDP models see in Q3 for USA, China, and Germany vs consensus.

- The Cliff – as in the 112th Congress kind; will #GrowthSlowing pull forward the Debt Ceiling Debate?

- Obama vs Romney – pickles or no pickles? You do need a risk management plan under either scenario.

Back to the Global Macro Grind…

After 4 consecutive down days (another 33 point draw-down), the SP500 storytellers who have been telling you to buy stocks “because they are cheap” at VIX 15-16 are going to get one of the many opportunities to buy’em cheaper again this week.

Growth Slowing matters. Most people get that by now. But the narrative of #EarningsExpectations becoming a big market liability has finally perforated the almighty media’s top headlines.

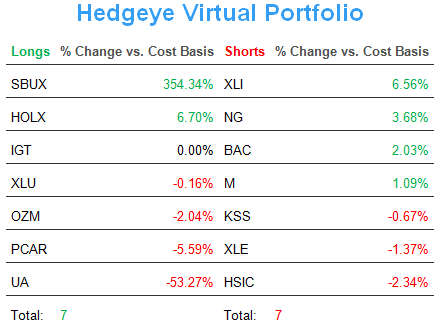

We’ve been saying short pro-cyclical Sectors (Industrials, Basic Materials, Energy) since we made our #GrowthSlowing call in March. That’s not a victory lap – that’s just the score. These S&P Sectors are getting pounded on #EarningsExpectations in July.

Only 10 days in, here’s the S&P Sector scoreboard for Q3 to-date:

- Industrials (XLI) = down -2.94%

- Basic Materials (XLB) = down -2.49%

- Energy (XLE) = down -2.12%

But, but, the Dow is “up for the YTD.” So everything is just fine, right?

Right. Right.

There’s a reason why Canadian McDonald’s franchisees refuse to launch anything that resembles eating a yellow snow cone too. Whether you think the average human being on this earth is “smart” or not, there are some things people just get.

The world’s economic growth is not fine. Neither is the perma contention of the Q1 bulls that “people are too bearish.” Maybe at 27 VIX in May (when the II Bull/Bear Spread pancaked to flat) consensus was bearish enough. Not here.

If you bought stocks at 1374 SPX and VIX 16 last week, you certainly didn’t get that call from us. Anything in the area code of 14-16 VIX has been the closest sell signal you can find to a layup as there has been in US Equities since 2008.

Back to the II Bull/Bear Survey, check this thing out (reported this morning):

- Bulls rise from 42.5% to 44.7%

- Bears are unchanged at 24.5%

- Bull/Bear Spread = 2020 basis points wide!

Away from what I am watching and eating, that’s the super little secret of my risk management morning. The general population of investors who are telling themselves consensus is Bearish Enough are simply lying to themselves inasmuch as I would be if I told you I don’t also love the Filet O’ Fish.

If you’d like access to this morning’s Q3 Big Macro Themes call, please email .

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, German DAX, and the SP500 are now $1, $97.56-103.01, 82.61-83.81, $1.21-1.24, 6, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer