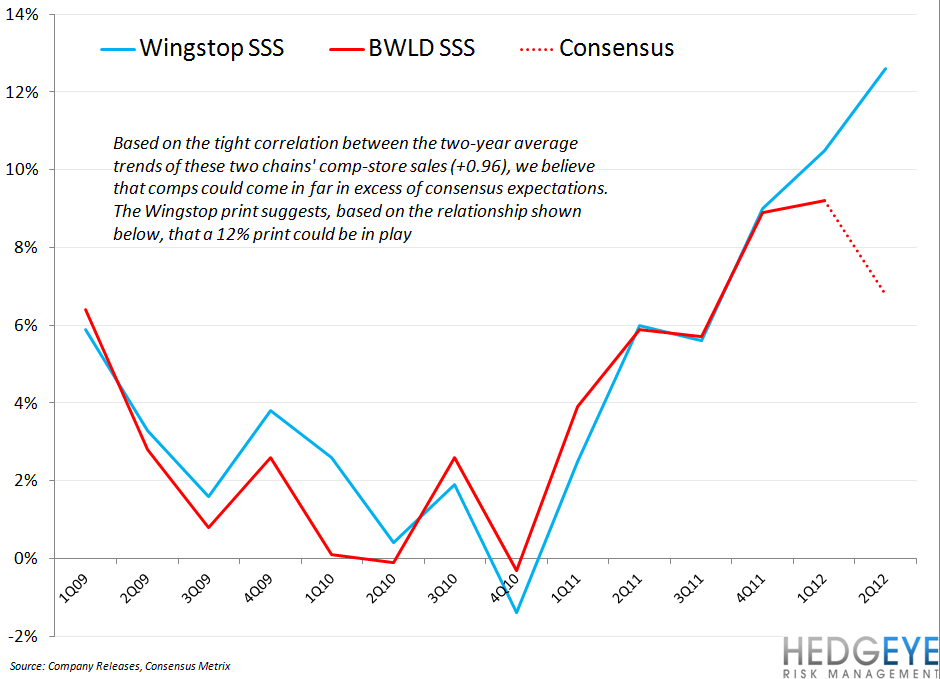

Wingstop comps are pointing to an upside surprise for Buffalo Wild Wings’ 2Q12 same-restaurant sales.

Buffalo Wild Wings has been a name we have liked on the short side for some time. Our call to stay short into the most recent earnings report, on April 24th, was correct as comps came in below expectations and the stock traded lower on the news. We were wrong on 4Q11 earnings, however, and don't want to make the same mistake twice. Heading into 2Q12 earnings on 7/20, we would advise not to be short heading into the quarter. Keith has traded this name very well in the Hedgeye Virtual Portfolio, covering for a gain yesterday, but we will not be advising him to revisit on the short side until this earnings report is out of the way.

Wingstop, a concept similar to Buffalo Wild Wings with 600 units in 31 states, posted strong same-restaurant sales of +12.6% for the second quarter. This is important because of the strong correlation between the two year averages of these concepts’ same-restaurant sales. If the relationship holds or – merely – doesn’t reverse, BWLD could print comps as high as 12% for the second quarter when it reports on 7/20. This would obviously negate our short thesis on the stock, which is predicated on cost pressures lowering EPS expectations and/or guidance over the remainder of 2012. With short interest at 12.4% of the float and the heightened likelihood of a substantial upside surprise in same-restaurant sales, we think a squeeze between now and when earnings is released has become a distinct possibility.

Howard Penney

Managing Director

Rory Green

Analyst