-- For specific questions on anything Europe, please contact me at to set up a call.

No Current Positions in Europe

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.3% week-over-week vs +1.9% last week. Top performers: Ukraine +7.5%; Greece +4.5%; Czech Republic +3.4%; Denmark +3.2%; Russia (MICEX) +2.0%; UK (FTSE) +1.6%. Bottom performers: Cyprus -9.2%; Spain -5.1%; Italy -3.8%; Hungary -1.4%; Austria -0.9%; Germany -0.1%.

- FX: The EUR/USD is down -3.14% week-over-week vs +0.69% last week. W/W Divergences: RUB/EUR +1.71%; GBP/EUR +1.65%; SEK/EUR +1.56%; NOK/EUR +0.31%; CHF/EUR +0.06%; DKK/EUR -0.05%; PLN/EUR -0.25%; CZK/EUR -0.60%; HUF/EUR -1.22%.

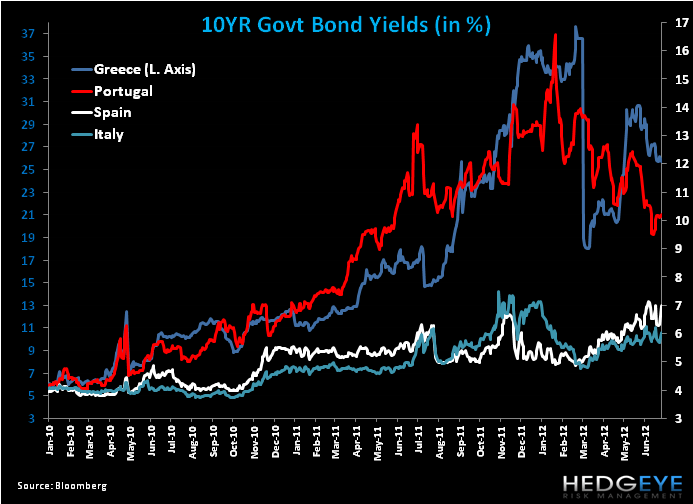

- Fixed Income: 10YR Yields busted back out for yet another week for the peripheral countries following the market’s optimism after last Friday’s EU Summit. Week-over-week, Spain’s 10 YR yield saw the biggest move of +67bps to 7.00%. Italy gained +22bps to 6.04% and Portugal gained +5bps to 10.21%. Conversely, French yields fell -28bps to 2.41%, followed by Germany at -20bps to 1.38% and Greece declined -10bps to 25.73%.

Changing Tides:

It was a week ago today that markets rallied hard on the EU Summit “conclusions”. Last week’s note titled “Not in my Lifetime” pointed out just how little substance the three paragraph statement actually contained. In this vein, there’s very little from a policy perspective that needs updating versus last week, because frankly Eurocrats don’t move that fast and as we’ve stated hundreds of times over, there’s a long road ahead for Europe to fix its sovereign and debt imbalances, and still a looming question if the Eurozone can sustain its current 17 member fabric. To the latter point, we expect Eurocrats to throw every kitchen sink and scrap for every available band-aid to keep their jobs and the structure together.

As we can see from peripheral yields and CDS spreads, as well as equity performance, there was quite a turn in sentiment this week? In particular, Spain’s 10YR yield is back up to that dangerous 7% mark. As a continuation of our work, the two main issues right here and now are the scope of the ESM (how it’s directed at bank recapitalizations and the implications if lending is through the sovereign, including with existing EFSF funds) and the scope of a pan-European banking authority (how’s it structured and what banks are included?). Yesterday in the ECB press conference President Mario Draghi gave little color on a European banking authority, including if the ECB would be a backstop for the future facility (see yesterday’s note July ECB Presser YouTubed).

Yesterday’s interest rate cuts from the ECB may prove marginally beneficial, yet again it’s a stretch to think that the cuts will have any impact on the existing sovereign and banking imbalances. After all, the LTROs proved highly ineffective. One point to stress, that the market may be looking towards, is any increased lending given the drop in the deposit rate to 0.00%, which is in essence begging banks to do something with their money besides park it for zilch. We expect the credit flow to broadly remain constrained for a protracted period as fundamentals and confidence continue to be bombed out.

EUR-USD:

Below is an updated EUR/USD price level chart. Our immediate term TRADE and intermediate term TREND support level is $1.22 and resistance is $1.25. Our call is that if $1.22 breaks, look out below! However, we’re not EUR parity folks because we see Eurocrats stepping in to prevent it.

Call Outs:

Germany - Chancellor Merkel’s approval rating rises to 66% = highest level since 2009 after last week’s EU Summit.

France - French Finance Minister Pierre Moscovici cut the government's growth forecasts to +0.4% in 2012 (vs the prior forecast of +0.5%) and between +1% and +1.3% for 2013 (versus estimate of +1.7%).

Cyprus - Officially becomes the EU president (it rotates every 6 months).

France - Needs as much as €43 billion in savings this year and next, the national auditor said, setting the stage for budget cuts by Hollande.

Greece - The new government dropped a plan to seek softer terms for its second bailout following warnings that it would be rejected by international lenders. Finance minister Yannis Stournaras said, "The program is off-track and we can't ask for anything from our creditors before we get it back on course."

Italy - The government approved €4.5B ($5.58B) in spending cuts for 2012, aimed at slashing the size of Italy's public sector and delayed a new tax increase until after the first half of 2013. The size of the cuts is slightly larger than the €4.2B in cuts the government originally projected for this year. The cuts for 2013 are projected at €10.5B, and €11B for 2014.

Ireland - The country returned to the debt markets this week for the first time since its bailout in September 2010. It sold €500 million of 3-month bills, in line with the target, at an average yield of 1.8%.

Slovenia - According to Bloomberg, Slovenia is headed toward becoming the 6th Eurozone nation to seek a bailout.

Spain - Spanish Economy Minister Luis de Guindos said Madrid will pass additional measures in order to achieve its annual deficit target. (Spain has said that it will cut its deficit to 5.8% of GDP in 2012 from 8.9% last year). Unconfirmed sources say Spain's government is putting finishing touches to an up to €30 billion package of spending cuts and tax hikes to help it meet this year's deficit targets, which could be announced next week.

Risk Monitor:

Like sovereign yields, sovereign CDS were mixed on the week. Portugal rose +45bps to 853bps, followed by Spain at +16bps to 568bps. Italy gained +6bps to 514bps. For a second straight week Ireland saw the largest decline in CDS w/w at -49bps to 533bps, followed by France -8bps to 185bps and Germany -4bps to 100bps.

Data Dump:

Eurozone PMI Composite 46.4 JUN (exp. 46) vs 46 MAY

Eurozone Unemployment Rate 11.1% MAY vs 11% APR

Eurozone PPI 2.3% MAY Y/Y (exp. 2.5%) vs 2.6% APR [-0.5% MAY M/M vs 0.1% APR]

Eurozone Retail Sales -1.7% JUN Y/Y (exp. -1%) vs -3.4% MAY

Germany Industrial Production 0.0% MAY Y/Y (exp. -1.2%) vs -0.6% APR [1.6% MAY M/M (exp. 0.2%) vs -2.1% APR]

Germany Factor Orders -5.4% MAY Y/Y (exp. -6.0%) vs -3.4% APR

UK PPI Input -2.2% JUN M/M (exp. -2.1%) vs -2.6% [-2.3% JUN Y/Y (exp. -2.2%) vs 0.0% MAY]

UK PPI Output -0.4% JUN M/M (exp. -0.2%) vs -0.2% MAY (fall most since 2008 in June) [2.3% JUN Y/Y (exp. 2.4%) vs 2.9% MAY]

UK PMI Construction 48.2 JUN (exp. 52.9) vs 54.4 MAY

UK M4 Money Supply -4.1% MAY Y/Y vs -4.0% APR

UK Halifax House Prices -0.5% JUN Y/Y (exp. -0.8%) vs -0.1% MAY

UK New Car Registrations 3.5% JUN Y/Y vs 7.9% MAY

Italy Unemployment Rate 10.1% MAY vs 10.2% APR

Spain Industrial Output WDA -6.1% MAY Y/Y vs -8.3% APR (falls for the 9th month)

Spanish Registered Unemployment -98.8k in June (est -51.6k) ahead of tourist season

Portugal Industrial Sales -1.3% MAY Y/Y vs -7.0% APR

Switzerland CPI -1.2% JUN Y/Y vs -1.1% MAY

Switzerland Retail Sales 6.2% MAY Y/Y vs 0.2% APR

Belgium Unemployment Rate 7.2% MAY vs 7.4% APR

Holland CPI 2.5% JUN Y/Y vs 2.5% MAY

Sweden Service Production 1.9% MAY Y/Y (exp. -0.4%) vs -0.7% APR

Norway Industrial Production 13% MAY Y/Y vs 7.5% APR

Norway Industrial Production Manufacturing 1.7% MAY Y/Y vs 1.9% APR

Norway Credit Indicator Growth 6.7% MAY Y/Y vs 6.7% APR

Ireland Consumer Confidence 62.3 JUN vs 61.0 MAY

Ireland Unemployment Rate 14.9% JUN vs 14.7% MAY

Ireland Industrial Production 4.4% MAY Y/Y (exp. 2.8%) vs 2.2% APR

Ireland New Vehicle Licenses 7320 JUN vs 9895 MAY

Interest Rate Decisions:

(7/4) Riksbank Interest Rate UNCH at 1.50%

(7/5) BOE Interest Rates UNCH 0.50%

(7/5) BOE Asset Purchase Program increased 50B Pounds to 375B Pounds

(7/5) ECB CUT the main refinancing operations by 25bps to 0.75%; CUT the interest rates on the marginal lending facility by 25bps to 1.50%; and CUT the deposit facility 25bps to 0.00%.

The Week Ahead:

Sunday: Jun. UK Employment Confidence

Monday: Aim to present a memorandum of understanding a European bailout of 100B Euros for Spain to the Euro group of Finance Ministers; Eurozone Sentix Investor Confidence; Jun. UK BRC Sales Like-For-Like, RICS House Price Balance; Germany Wholesale Price Index (Jul. 9-12); May Germany Exports, Imports, Current Account, Trade Balance; Jun. France BoF Business Sentiment; Jun. Greece Consumer Price Index

Tuesday: Jun. UK NIESR GDP Estimate; May UK Industrial Production, Manufacturing Production, Visible Trade Balance, Trade Balance Non EU, Total Trade Balance; May France Industrial Production, Manufacturing Production; May Italy and Greece Industrial Production

Wednesday: Jun. Germany Consumer Price Index – Final; May France Current Account; May Spain House Transactions

Thursday: Jun. Eurozone ECB Monthly Report Published; May Eurozone Industrial Production; Jun. France CPI; Apr. Greece Unemployment Rate

Friday: Jun. Spain and Italy CPI – Final

Extended Calendar Call-Outs:

19 July: ECB governing council meeting

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst