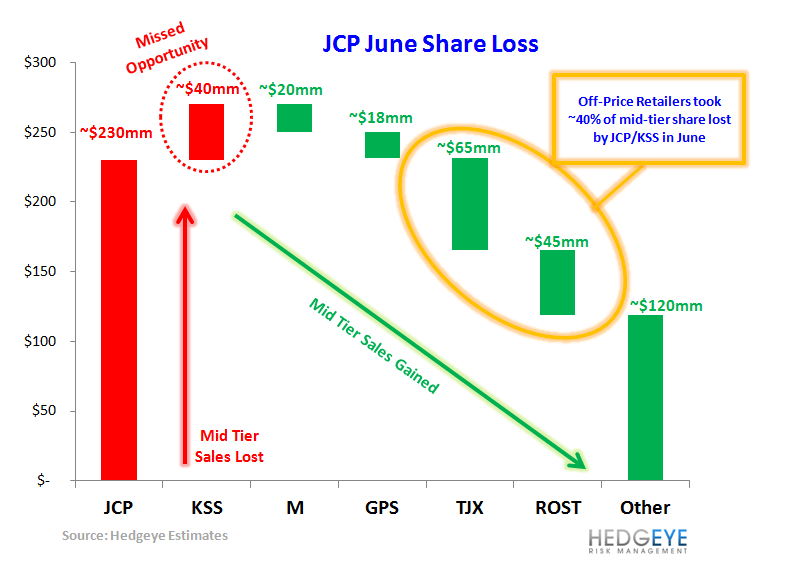

With nearly $270mm in mid-tier share up for grabs in June, the off-price channel is the big share gainer.

If we assume that the underlying 2yr revenue trend of ~-8% from JCP’s first quarter remained consistent in June, this would imply revenues down ~14% for the month creating a loss of ~$230mm. Adding on the $40mm in sales that KSS ceded in June at a time when it should be benefiting from JCP's strategic mishaps, we estimate a total of $270mm in mid tier share was up for grabs.

With M’s revenue growth slowing from +$80mm to +$20mm in June, we think the off price retailers have been the biggest beneficiaries of JCP's & KSS’ lackluster execution. Assuming half of ROST & TJX’s domestic dollar growth was in categories overlapping with JCP/KSS, the two combined account for ~40% of the share ceded in June. As we've been saying, Ron Johnson better be aware that the off price competition is indeed snagging a large portion of the sales he’s losing. It won’t be easy to recapture these customers from the off-price channel even if the new strategy gains traction in 2H.