“Every child begins the world again.”

-Henry David Thoreau

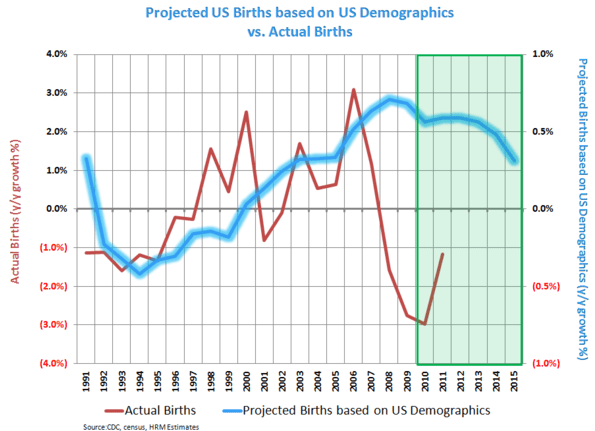

Deciding to start a family is an incredibly hopeful act and one that reflects in part the national mood. It should be no surprise then that birth trends in the United States peaked in 2007 and then began a long period of deceleration and decline over the subsequent 5 years. Births were still declining in 2011 and look likely to continue to slow in 2012, reflecting the shifting landscape of global economic concerns. There are glimmers of hope, however, and a recovery bodes well for many stocks in Healthcare, but in particular Hosptials.

There is a large body of academic work that describes how individuals and families consume, save, and plan over their lifetime. The broad name of the field is Life-Cycle Hypothesis (http://en.wikipedia.org/wiki/Life-cycle_hypothesis). In the simplest terms, an individual behaves in predictable ways over their lifetime. They buy a home, invest in stocks, have children, reach their peak income, among many things, in predictable ways over their lifetimes. For Healthcare, they also age, which begins an accelerating cycle of doctor visits, medications, and hospital stays. The key point though is that theses consumption patterns are distinct at discrete age groups. Looking then at the historic pattern of peaks and troughs of births tells a story of predictable consumption in the future.

What makes understanding these consumption patterns worth thinking about is the wide variation in birth trends over the last 100 years, including the last five years of declines in the United States. Birth trends fell in the 1920s and 1930s, which has been a present day problem for Nursing Homes and Senior Living in recent years as the growth in their key customer base has slowed. The Baby Boom following WWII led to the great healthcare boom of the 1990s and early 2000s as Boomers aged through the period in their life when healthcare consumption begins to accelerate in earnest. It helped too that they had reached peak earnings (late 40s) and peak disposable income (50s).

For Hosptial companies birth trends play a major role in admission trends, making up over 20% of the total hospital admissions. While there have been many issues facing hospitals including reimbursement pressure from states cutting Medicaid, cuts to Medicare writen into the Affordable Care Act, and pressure from private insurers through rates and rising out of pocket expenses for their enrollees, the slowdown in births has been the least discussed.

Our analysis shows that over the last 5 years, the differnece between the predicted number of births, based on per capita birth rates by age and the number of women entering child bearing years, and actual births has created a cummulative deficit of between 530,000 and 1,600,000 babies not being born. Considering that there were 4.3M births in 2007, the magnitude is indeed relevent. Further, uncovering where the inflection point of a recovery lay in the furture will be a meaningful catalyst for admission trends for Hosptials. In addition to slowing birth related admissions, Hosptials have experienced pressure on admissions from everything from Knee Replacements to Cardiovascular surgeries.

Our best forecast about the timing of a recovery in births in the United States is that we will see them turn positive in Q412. However, over the next two quarters, trends will remain soft and in fact appear to be weakening further sequentially. This will have a negative impact on Hospital admission trends, revenues, and earnings. Weighing the short term weakness against the longer term acceleration will be our key focus over the next few quarters.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Germany’s DAX, and the SP500 are now $1, $97.47-101.71, $81.59-82.39, $1.24-1.26, 6, and 1, respectively.

Tom Tobin

Managing Director Healthcare