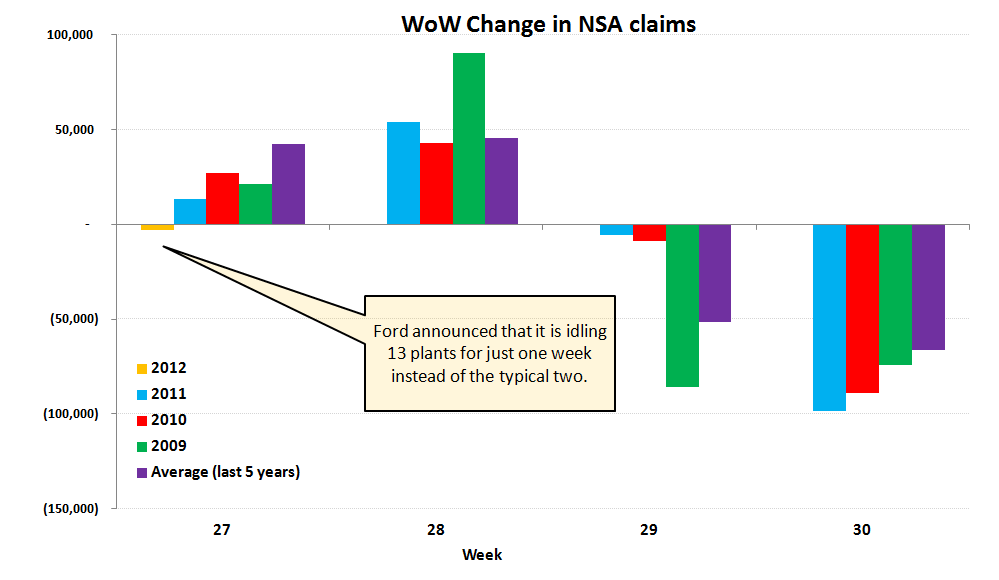

Claims Strength Attributable to Ford Not Idling Plants - A Healthy Sign

This morning's jobless claims number was better than expected primarily because of a decision by Ford to idle 13 plants for just one week this summer instead of two. Factory workers are allowed to collect unemployment insurance during these idling periods. As the chart below shows, weeks 27 and 28 normally reflect large increases in NSA claims while the plants are closed. This reverses in weeks 29 and 30 as the plant resume production. The average WoW rise in NSA claims in the comparable week over the last five years has been 42k compared to the decline in NSA claims of 3k in this morning's print.

Initial jobless claims fell 12k last week to 374k. Incorporating the 2k upward revision to the prior week's data, claims fell 14k. Rolling claims fell 1.5k WoW to 386k. On a non-seasonally adjusted basis, claims fell 3k. NSA rolling claims are improving at a rate of ~7% YoY, which is a further decline in the rate of YoY improvement - a worrisome sign.

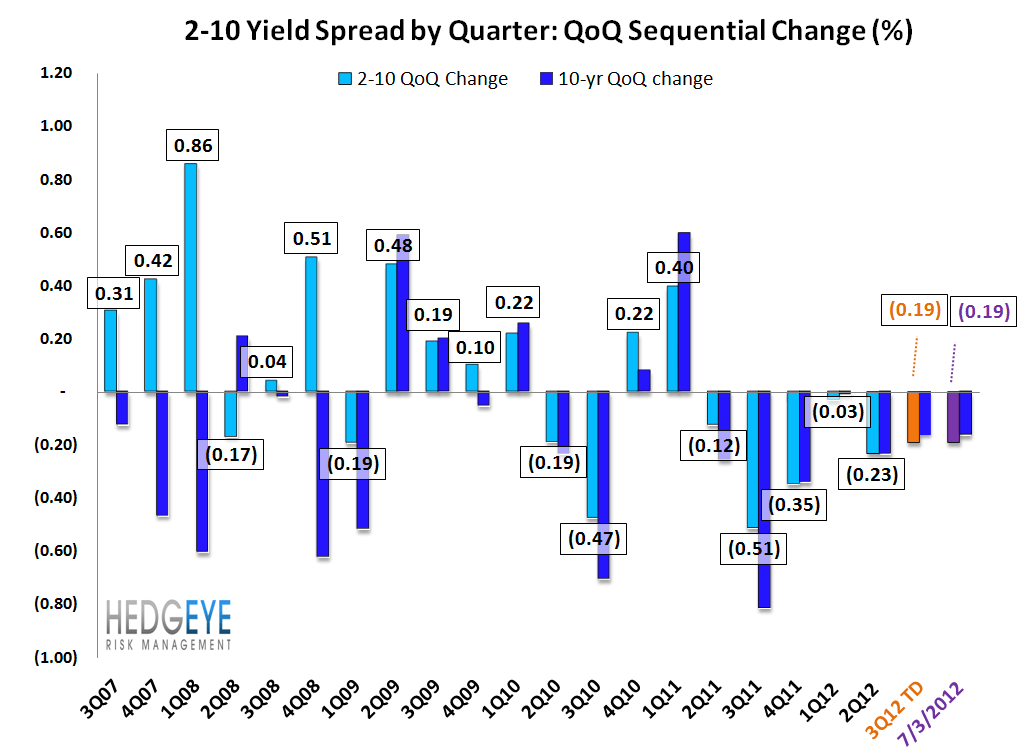

The 2-10 Spread

The 2-10 spread widened 1 bp WoW to 132 bps, while the ten-year treasury yield rose 1 bp to 163 bps.

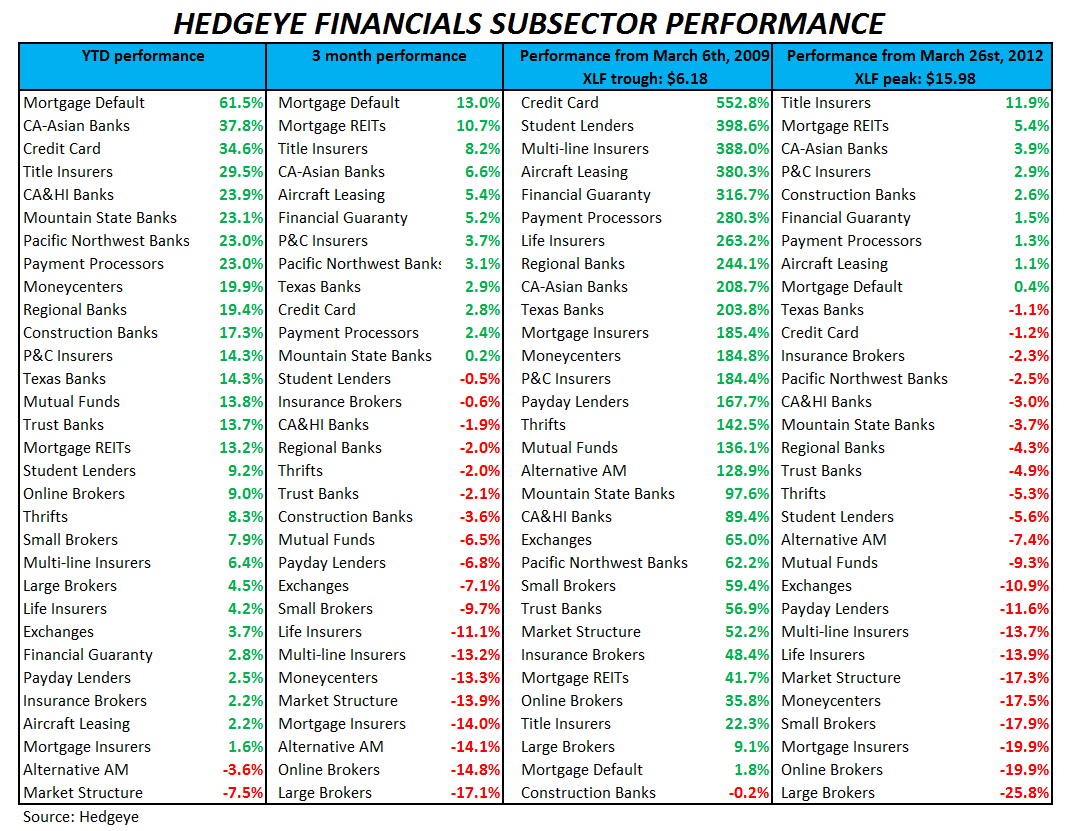

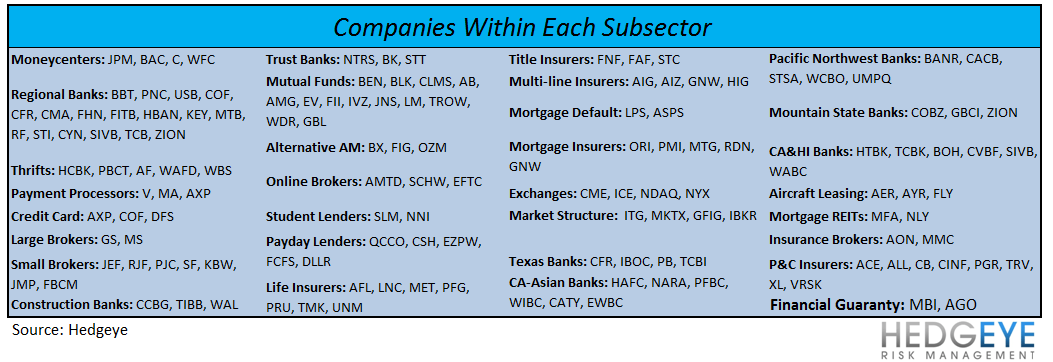

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.