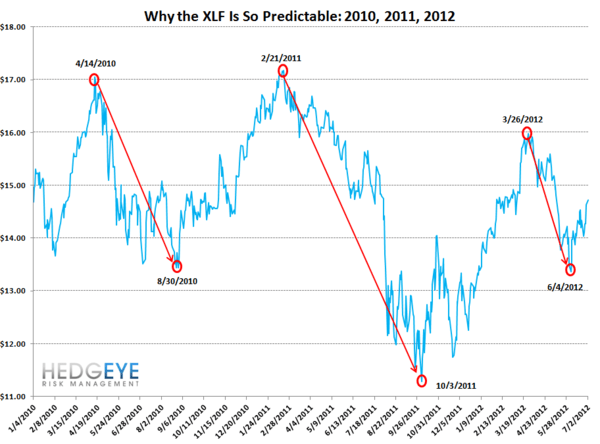

Financials have had one rollercoaster of a ride over the last six years – and that’s putting it rather lightly. This morning we took notice of the XLF (financials SPDR) and what’s been going on there over the last three years. Essentially, this ETF has seen consistent drawdowns in terms of three factors: timing, magnitude and duration. There is a cycle that has been setup which will continue for the foreseeable future that relies heavily on monetary policy put forth by central planners (read: The Fed).

Since 2010, what happens is that in Q2 and Q3, fears begin to mount about a major recession and investors essentially get scared as seasonal adjustments of government data come in. So the market then begins to look to Ben Bernanke and the Federal Reserve for a crutch to help them out in terms of lower rates, extensions of existing market operations (Twist) or another dose of quantitative easing. This happens in the fall and then for Q4 of that same year and leading into Q1 of the following year, the market becomes overly bullish. Then the same Q2/Q3 fears kick in again and the cycle repeats itself

Hence, the drawdown pattern in the XLF. Life’s good when Bernanke has your back (until he doesn’t).