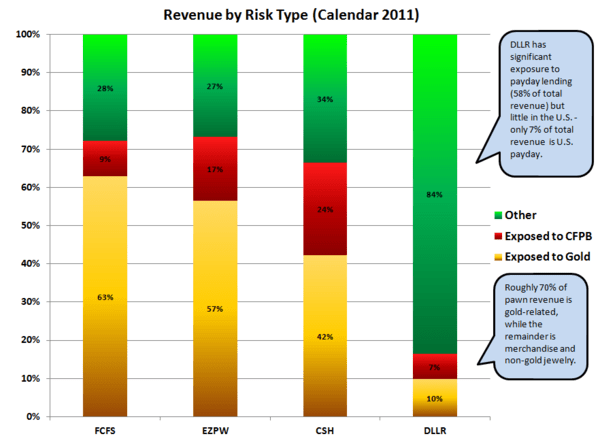

Pawn shops and gold buyers have been on a huge tear over the past two years. It appears that everywhere we drive, someone has put up a “BUY GOLD” sign. The whole fanatical attitude over pawn shops is fading fast and as a result, we are reiterating our bearish case for names like CSH, EZPW and FCFS in the back half of 2012.

Essentially, gold prices are weakening along with volumes. While EZPW and CSH hedge their gold prices (out 3 months and 6 months, respectively), FCFS does not. For gold-sensitive lenders, the current reversal in commodity prices does not bode well for future earnings. Additionally, customers are running out of gold to pawn. Most gold has been purchased by pop-up gold buyers and thus ends up as scrap. This does not bode well for the pawn shops operating actual loan agreements with gold as collateral.

We bring to your attention a paragraph from a note our financials team put out July 2:

“Gold averaged $1,602/oz in June, up 4.8% YoY and up 0.8% from the average price in May of $1,590. In the second quarter gold averaged $1,613/oz, which is 6.8% higher than comparable period last year. This is a marked slowdown from the first quarter's year over year growth rate of 22%. Holding gold at its current price of $1,604 would imply a YoY decrease of 7.0% in 3Q12 and a negative 5.0% YoY change in 4Q12. This will be in addition to negative gold volume trends running in the mid-to-high teens for EZPW and FCFS on a per store basis. Consensus revenue expectations do not reflect this dynamic. This will be the slowest gold price tailwind for the sector in 12 quarters (since 2Q09).”

When the quantitative setup is right, we will go short pawns. Post-summer numbers should highlight the difficult environment that lies ahead for pawn lenders.