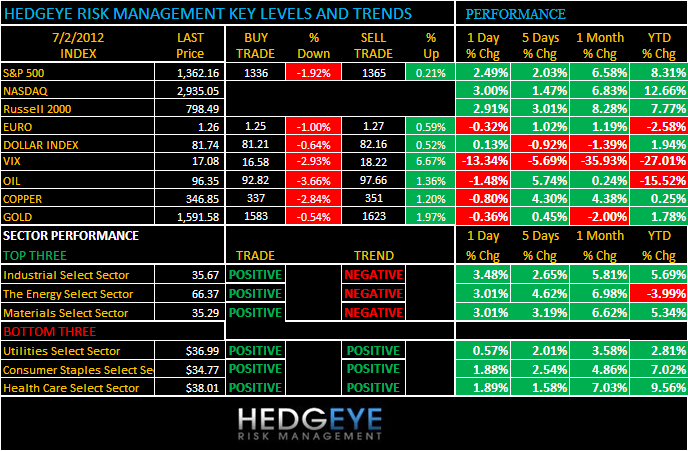

TODAY’S S&P 500 SET-UP – July 2, 2012

As we look at today’s set up for the S&P 500, the range is 29 points or -1.92% downside to 1336 and 0.21% upside to 1365.

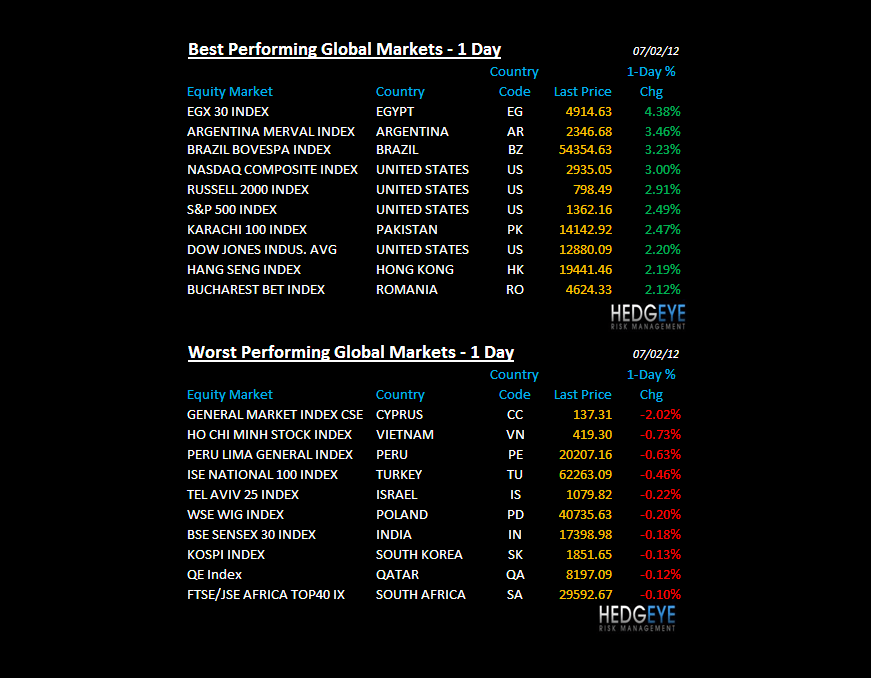

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/29 NYSE 2281

- Up from the prior day’s trading of 397

- VOLUME: on 6/29 NYSE 1094.36

- Increase versus prior day’s trading of 20.71%

- VIX: as of 6/29 was at 17.08

- Decrease versus most recent day’s trading of -13.34%

- Year-to-date decrease of -27.01%

- SPX PUT/CALL RATIO: as of 6/29 closed at 1.35

- Down from the day prior at 1.85

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.64

- Unhanged from prior day’s trading

- YIELD CURVE: as of this morning 1.33

- Down from prior day’s trading at 1.34

MACRO DATA POINTS (Bloomberg Estimates):

- 8am: Markit US PMI Final, June

- 9:30am: Intl Grains Council monthly crop report

- 10am: ISM Manufacturing, June, est. 52 (prior 53.5)

- 10am: ISM Prices Paid, June, est. 45.7 (prior 47.5)

- 10am: Construction Spending, May, est. 0.2% (prior 0.3%)

- 11:30am: U.S. to sell $30b 3-mo. bills, $27b 6-mo. bills

- 1:15pm: Fed’s Williams to speak in San Francisco

GOVERNMENT:

- House, Senate not in session

- White House has no public events scheduled

WHAT TO WATCH:

- Bristol-Myers Squibb to buy Amylin for $31-shr cash

- Linde to buy respiratory-care company Lincare for $3.8b

- Dell said to be near buying Quest to add data-ctr software

- Euro-Area Unemployment Climbs to Record 11.1% on Spanish Cuts

- Barclays Chairman Agius said poised to quit after Libor fine

- Fund-Manager Pay Rules Included in EU Response to Madoff Fraud

- Pena Nieto Claims Win in Mexico Election as PRI Returns to Power

- American Electric forecasts a week to fix storm blackouts

- Airbus to Invest $600 Million in Alabama Facility, Reuters Says

- Japan Tankan Confidence Improves Even as Yen Limits Exports

- BNP Said to Mull Plan for $50 Billion Spain-Italy Funding Gap

- Weekly agendas for Media/Entertainment, Industrials, Finance, Energy, IPOs, Transports, Real Estate, Consumer, Health, Tech, Rates, Canada Mining, Canada Oil & Gas

- U.S. Jobs, Tankan, Mexico President: Wk Ahead June 30-July 7

EARNINGS:

- Acuity Brands (AYI) 8:30am, $0.79

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Speculator Bullish Oil Wagers Rose Before Rally: Energy Markets

- Platinum Slump Seen Spurring China’s Jewelers: Chart of the Day

- Corn Extends Rally as Hot, Dry Weather Threatens Midwest Yields

- Hedge Funds Win on Bull Bets Before Biggest Rally: Commodities

- Oil Declines After Biggest Gain Since 2009 on Europe Concerns

- Copper Falls on Signs of Worldwide Manufacturing Deterioration

- Iran-Oil Sanctions Risk Biggest OPEC Export Loss Since Libya

- Gold Set to Decline as Biggest Gain in Four Weeks Spurs Sales

- U.S. Natural Gas Futures Slide From Highest Price Since January

- Isramco Says ‘Significant’ Natural Gas Signs at Shimshon Site

- German 2013 Power Declines as European Coal, Carbon Permits Drop

- Japan’s LNG Imports May Rise 6.5% to 88.6 Mln Tons, IEEJ Says

- Russian Oil Output Falls on Month, Holds Near Post-Soviet High

- EU’s Iranian Ban Will Push Up Demand for Sour Crude, JBC Says

- Dubai Backwardation Rises Amid Iran Sanctions Start: Asia Crude

- Hedge Funds Win on Bull Bets Before Rally

- Goldman Raises Price Forecasts for Corn, Soybeans, Wheat

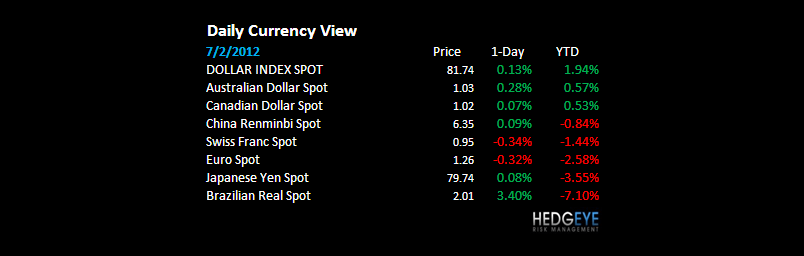

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

<CHART7>

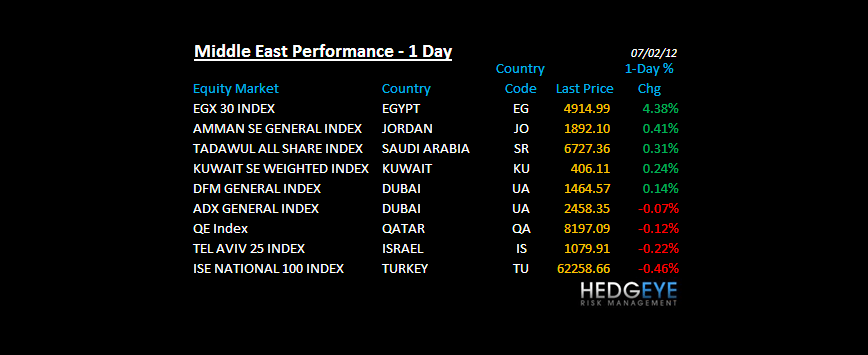

MIDDLE EAST

The Hedgeye Macro Team