This note was originally published at 8am on June 15, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Would it be excessive of me to ask you to save my life twice in a week?”

-Tyrion, Game of Thrones

I was speaking at a Canadian Economic Development dinner last night. At the end of my presentation I opened it up for the customary Q&A. Most of the questions were concerned with where Oil and Metal prices could go when Bernanke and Geithner run out of US Dollar Debauchery bullets.

Whenever talking about mean reversion and/or tail risks, the most obvious two-word risk factor that I explain (that neither Berrnanke or Geithner ever mention) is CORRELATION RISK. After I walked through that, a nice Scottish-Canadian man stood up and said, “this is more of a statement than a question – you are scaring the hell out of us.”

I politely replied (he was Canadian remember), “after what happened again out there into the US market close today, you should be scared.”

Back to the Global Macro Grind…

Yesterday’s stock and commodity markets were trading off into the close, and then completely reversed course to the upside after our overlords floated a headline to the market that central planners were “prepared to take coordinated action.”

Whew, thank God for that!

Fear is what central planners are feeding you. Without fear-mongering the citizenry, they can’t print, bail, and print. Without fear of being held accountable for their own policy moves (Growth Slowing, equity market outflows, crashing market prices, and no political re-election) they wouldn’t be making these ridiculous short-term decisions.

At this point, it’s clear that they have gone over The Wall. They cannot go back. And no, that doesn’t mean that it ends well when they realize what’s on the other side either.

In HBO’s latest mini-series hit, Game of Thrones, The Wall separates the known (centrally planned kingdom societies) from the unknown. It’s the perfect metaphor for how conflicted and compromised Keynesian politicians must feel right here and now in 2012. They fear what they cannot see. They fear letting free market prices clear.

We let losers win until The Wall no longer holds. In the meantime, Mr Market is already in motion in taking down the Old Wall.

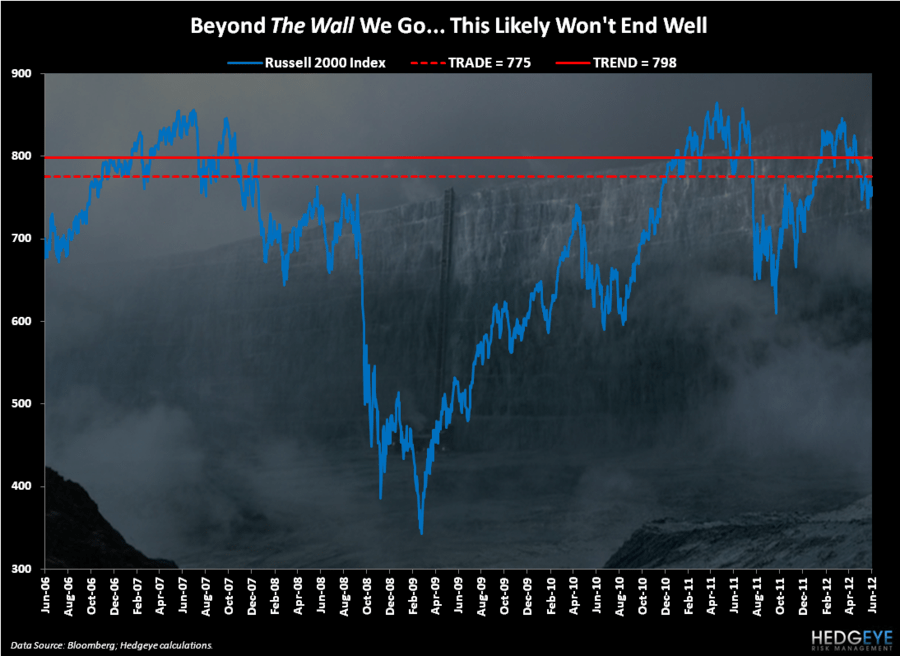

If you are afraid of a small part of The Wall coming down this weekend, you should be – because now these market morons have ramped expectations (market prices) right back up to the walls of Hedgeye’s immediate-term TRADE lines of resistance.

What does that mean?

That means that if market prices fail, again, at this interconnected wall of resistance, there is very little left in terms of Big Government Intervention catalysts and/or downside market price supports.

Across countries, commodities, and currencies, here are your immediate-term TRADE walls of resistance:

- SP500 = 1344

- Russell2000 = 775

- Euro Stoxx50 = 2179

- CRB Commodities Index = 280

- Japan’s Nikkei225 = 8731

- Shanghai Composite = 2348

- South Korea’s KOSPI = 1897

- Germany’s DAX = 6281

- Spain’s IBEX = 6797

- Greece’s ATG Index = 664

- Oil (Brent) = $104.87

- Gold = $1645

- Copper = $3.44

- 10yr UST Yield = 1.73%

- EUR/USD = $1.27

If, by chance, The Wall of resistance to do more of what has not worked is overcome, beyond that is another wall – The Wall of intermediate-term TREND resistance. Economic gravity is thick.

It remains unclear if these people making these short-term political decisions to manipulate market expectations have any idea about what I am talking about. It remains unknown if they ever had a proactive process of preparation to meet the challenges that remain outside The Wall of their leadership’s groupthink. It is a problem – it is them.

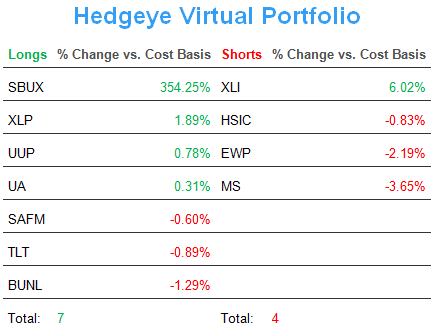

Fortuitously, in anticipation of some version of this political gong show, I got longer earlier this week. Don’t expect me to keep a 67% Cash position into this weekend though. I only have 4 SHORT positions left in the Hedgeye Portfolio. Expect that number to go up, maybe a lot, too.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1586-1634, $95.90-98.71, $81.73-82.36, $1.24-1.27, and 1310-1344, respectively.

Happy Father’s Day Dad – best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer