TODAY’S S&P 500 SET-UP – June 29, 2012

As we look at today’s set up for the S&P 500, the range is 17 points or -0.68% downside to 1320 and 0.60% upside to 1337.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/28 NYSE 397

- Down from the prior day’s trading of 1589

- VOLUME: on 6/28 NYSE 906.61

- Increase versus prior day’s trading of 32.45%

- VIX: as of 6/28 was at 19.71

- Increase versus most recent day’s trading of 1.34%

- Year-to-date decrease of -15.77%

- SPX PUT/CALL RATIO: as of 6/28 closed at 1.85

- Up from the day prior at 1.56

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – US Treasury Bonds continue to be the only sober asset class not being whipped around by central planning headlines. At 1.62% this morning, yields haven’t budged (the 10yr is actually down 5bps on the wk and the Yield Spread (10s/2s) is 6bps narrower. More bailouts only slow growth further; that will be obvious in July/August.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.64

- Increase from prior day’s trading at 1.58

- YIELD CURVE: as of this morning 1.33

- Up from prior day’s trading at 1.28

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Fed’s Rosengren speaks on banking crisis in Amsterdam

- 8:30am: Fed’s Dudley speaks in Puerto Rico

- 8:30am: Personal Income, May, est. 0.2% (prior 0.2%)

- 8:30am: Personal Spending, May, est. 0.0% (prior 0.3%)

- 8:30am: PCE Deflator M/m, May, est. -0.2% (prior 0.0%)

- 8:30am: PCE Core M/m, May, est. 0.2% (prior 0.1%)

- 9:45am: Chicago Purchasing Mgr, June, est. 52.3 (prior 52.7)

- 9:55am: University of Michigan consumer sentiment, June final, est. 74.1 (prior 74.1)

- 11am: Fed to purchase $4.25-5.25b notes in 6/30/2018-5/15/2020 range

- 12:05pm: Fed’s Bullard speaks on U.S. economy in Arkansas

- 1pm: Baker Hughes rig count

- NAPM-Milwaukee, June, est. 55.2 (prior 57.7)

GOVERNMENT:

- House, Senate in session

- President Obama travels to Colorado for wildfires

- EPA Asst. Administrator Gina McCarthy speaks at House

- Energy panel hearing on EPA’s greenhouse-gas regulations, 9am

- Last day to submit comments to CFTC on agency’s proposal to ease part of Dodd-Frank regulations limiting speculation in oil, natural gas, wheat and other commodities

WHAT TO WATCH:

- EU summit continues in Brussels; Euro-area leaders agreed to relax conditions on emergency loans for Spanish banks and possible help for Italy

- Anheuser-Busch InBev buys rest of Modelo for $20.1b

- Basel said to agree on draft changes to bank liquidity rule

- Personal spending probably stalled in May, household purchases est. unchanged after 0.3% gain in April

- Melrose to buy Elster for $20.50/shr. or $2.3b

- Credit Suisse says it expects to be profitable in 2Q

- Nomura cuts executive pay, halts some business on insider leaks

- Ford said pretax oper. profit will be “substantially lower” in 2Q

- JPMorgan allowed CIO Ina Drew to retire with $21.5m in stock, options

- RIM drop puts pressure on co. to “sell, break up or die”

- Apple Says Dan Riccio to run hardware as Bob Mansfield retires

- Melrose to buy Elster Group for $2.3b

- Peter Madoff, the younger brother of Bernard L. Madoff, is set to plead guilty to conspiracy and fraud

- Qualcomm CEO Paul Jacobs said he wouldn’t rule out owning a manufacturing plant or tapping its cash pile

- Bain Capital said to raise $2.3b for 2nd Asia fund

- Nissan adding Sentra output, 1k jobs at Mississippi plant

- Today is last trading day of month, quarter, half-year

- U.S. Jobs, Tankan, Mexico Presidency: Wk Ahead June 30-July 7

EARNINGS:

- Constellation Brands (STZ) 7:30am, $0.39

- KB Home (KBH) 8am, $(0.35)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Traders Extend Bullish Streak on Debt Crisis: Commodities

- Commodities Up Most in Six Months as Europe Eases Credit Rules

- Oil Rises From Nine-Month Low on Europe Measures, Supply Concern

- Corn Poised for Biggest Weekly Gain Since 2008 on U.S. Drought

- Copper Rises Most in Two Weeks Amid Reduced Debt-Crisis Concern

- Palm-Oil Exports From Indonesia Set to Advance on Ramadan

- Gold Pares Worst Quarterly Loss in Eight Years on Europe Deal

- Raw Sugar Rises Before ICE July Futures Expiry; Coffee Advances

- Rio Tinto Sees China Growing 8% in 2012 as Euro Crisis Deepens

- Drought Rivaling 1980s Won’t Produce More U.S. Farm Assistance

- Iran Offers to Ship Crude to South Korea on its Own Oil Tankers

- Gas Drop to $2 Seen After Worst-to-Best Rebound: Energy Markets

- European Carbon Permits Are Fastest-Rising Commodity in June

- Alcoa Plans Job Cuts in Australia to Lower Cost, Retains Smelter

- China, Singapore Granted U.S. Exemptions From Iran Sanctions

- Oil May Rise After Imposition of Iran Sanctions, Survey Shows

CURRENCIES

EURO – get the EUR/USD right, you get all the Correlation Risk trades right – and that’s pretty much the biggest reason why everything from Copper to the Spanish IBEX are ripping. At +1.2% the Euro is having one of its biggest up days of Q2 here, so that is going to train wreck anyone who nailed the quarter, on the last day of the quarter. Nice.

EUROPEAN MARKETS

GERMANY – probably the most important lines to watch are Euro $1.26 (immediate-term TRADE resistance) and DAX 6251 (immediate-term TRADE line); for the DAX, holding above that line would be as bullish as it looked bearish below the line only 24hrs ago. Guys running billions can probably flip their entire book upside down in 24hrs, right?

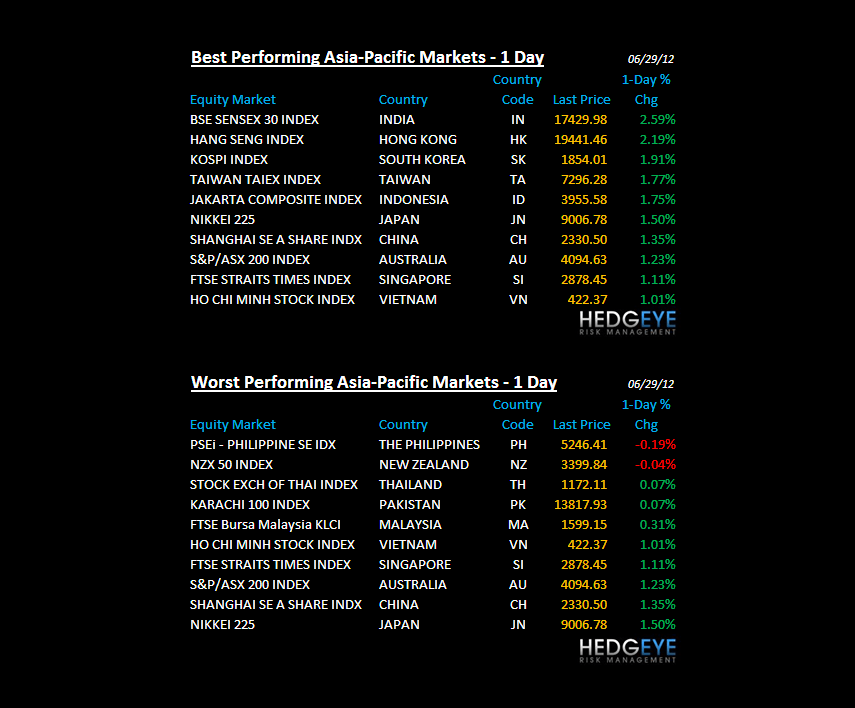

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team