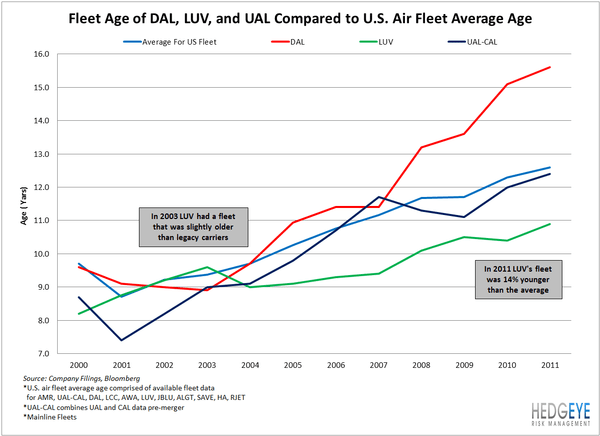

- LUV fleet has aged, but less quickly than the fleets of legacy carriers. The gap has widened.

- Airlines are aging their operating assets unsustainably, so current free cash flow is not sustainable.

- This should eventually be good news for aircraft OEMs with respect to US demand.

Expert Call/Sector Event: We are hosting an expert call on Industrial sector antitrust policy, with a focus Airline industry consolidation. We will focus specifically on US Airways bid for AMR, as well as changes in antitrust policy with respect to the Industrials sector. Our expert will be Lisa Harig, a Partner at McBreen & Kopko and head of the firm’s Washington D.C. office. She is a former in-house counsel for Trans World Airlines, Inc. and BearingPoint, Inc. Ms. Harig represents domestic and international clients, including airlines, manufacturers and individual aircraft owners. Her practice focuses on a wide range of corporate, transactional, compliance and regulatory matters, including representation before the U.S. Department of Transportation and Federal Aviation Administration. Please contact us or your Hedgeye Sales representative to participate. The call is scheduled for July 10th at 11AM.

Sector Comment: Chinese heavy equipment sales continue to deteriorate – falling 20% to 30% year over year across the board. This is not a vote of confidence for future construction activity. This might impact commodity prices, but it also is a negative for competitors like CAT and Komatsu with exposure to the market. Weak demand at home may eventually force SANY and Zoomlion further into developed markets. Our macro team has done excellent work on growth in China.