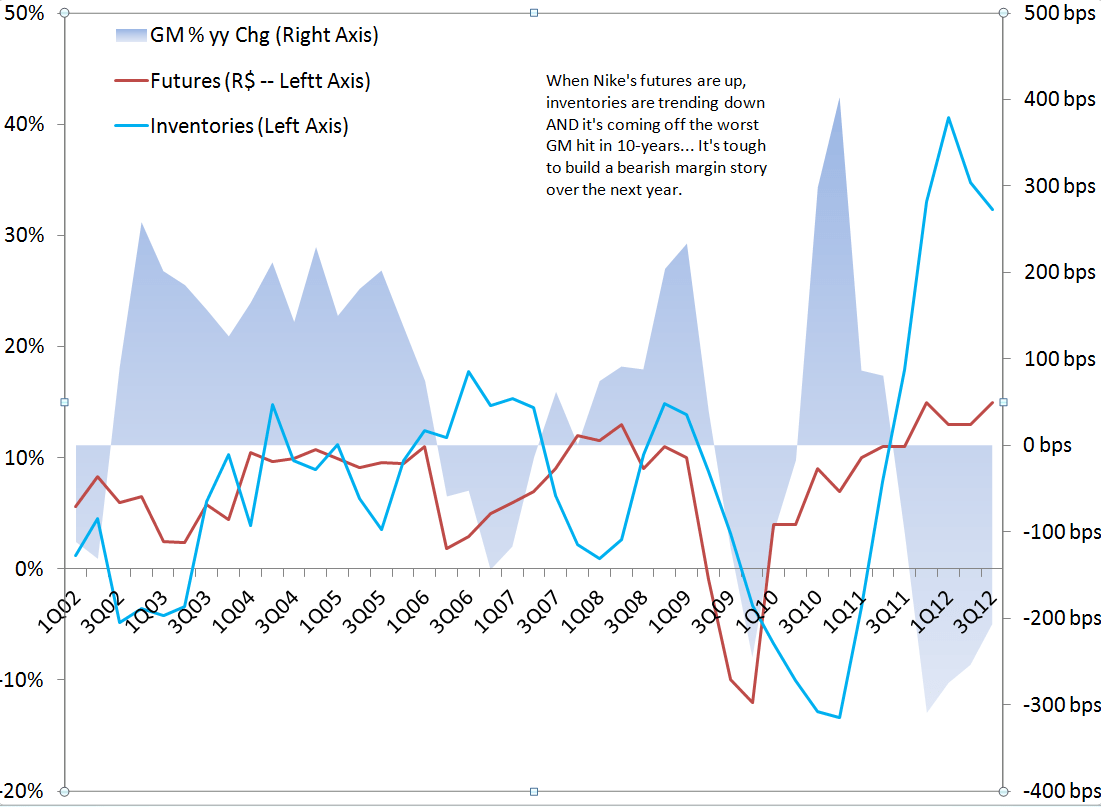

When Nike's futures are up, inventories are trending down AND it's coming off the worst Gross Margin hit in 10-years, it's tough to build a bearish margin story over the next year.

When Nike's futures are up, inventories are trending down AND it's coming off the worst Gross Margin hit in 10-years, it's tough to build a bearish margin story over the next year.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.