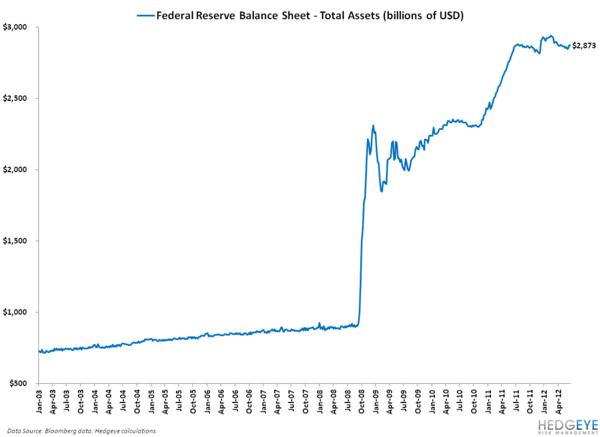

Once upon a time someone remarked “bigger is better.” A lot of people would kindly disagree with the originator of that statement. Since 2007, the Federal Reserve and the European Central Bank (ECB) have been in a race of sorts to add as many assets to their balance sheet as humanly possible. Looking at the chart of the Federal Reserve’s balance sheet fluctuations below, you can see the original “bazooka” of $800 million that former Treasury Secretary Hank Paulson used in mid-2008.

From there, when we have gone one direction: up. When things go wrong and the US doesn’t like it, we slap it on the Fed’s balance sheet. And despite constant asset sales, including the Maiden Lane portfolios that we built from the sewers of AIG, we have yet to reduce the Fed’s balance sheet in earnest.

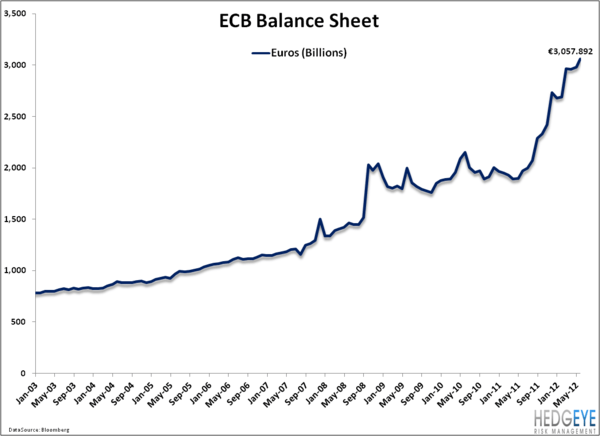

The same goes for the ECB, save for the huge 2008 spike. It has been a gradual climb into 2011 upon which everyone else in the world realized that Greece, Spain, Italy, etc. were all corrupt, out of money and needed bailouts. So now the ECB has a bigger balance sheet from the Fed and Italy has yet to official default or come begging for a bailout yet. Expect the pain to keep coming as the balance sheet continues to rise at the ECB.

If we accept that the future direction of the size of the central bank’s balance sheet is a decent proxy for either more hawkish or more dovish monetary policy, then there are a couple of scenarios:

1. QE3 is imminent – In effect, the currency market is pricing in incremental quantitative easing from the Federal Reserve. Based on the most recent commentary from the Federal Reserve, this seems to be an unlikely scenario in the intermediate term as they did nothing last week but extend Operation Twist. In effect, this action is merely equivalent to not tightening.

2. QE3 is not imminent and intervention in Europe continues – If the monetization of debt / lender of last resort continues to be an ECB led activity, the balance sheet of the ECB should continue to expand. Given the situation in the European banking system, this seems a very likely scenario. In fact, as we’ve highlighted, Italy and Italian banks are the next potential shoes to fall in Europe with massive pending maturities and accelerating credit default swaps. It is highly likely that the ECB will continue to have to step up and support its banking system.

Welcome to 2012: the year of the bailout.