TODAY’S S&P 500 SET-UP – June 28, 2012

As we look at today’s set up for the S&P 500, the range is 16 points or -0.89% downside to 1320 and 0.31% upside to 1336.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/27 NYSE 1589

- Up from the prior day’s trading of 833

- VOLUME: on 6/27 NYSE 684.49

- Decrease versus prior day’s trading of -3.90%

- VIX: as of 6/27 was at 19.45

- Decrease versus most recent day’s trading of -1.37%

- Year-to-date decrease of -16.88%

- SPX PUT/CALL RATIO: as of 6/27 closed at 1.56

- Up from the day prior at 1.55

CREDIT/ECONOMIC MARKET LOOK:

USA – got “de-coupling”, c’mon already. The Bond market has had this right for a long time, and the 10yr has it right again this morning, looking to break 1.60% again as the Yield Spread (10s-2s) threatens to break-down to new YTD lows. Yield Spread is down -7bps wk-over-wk. Bank earnings (cash, not trading condors) going lower.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.60

- Decrease from prior day’s trading at 1.62

- YIELD CURVE: as of this morning 1.30

- Down from prior day’s trading at 1.31

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: GDP Q/q, 1Q revised, est. 1.9% (prior 1.9%)

- 8:30am: Personal Consumption, 1Q rev., est. 2.7% (prior 2.7%)

- 8:30am: GDP Price Index, 1Q revised, est. 1.7% (prior 1.7%)

- 8:30am: Core PCE QoQ, 1Q revised, est. 2.1% (prior 2.1%)

- 8:30am: Initial Jobless Claims, June 23, est. 385k (prior 387k)

- 8:30am: Continuing Claims, June 16, est. 3280k (prior 3299k)

- 9:45am: Bloomberg Consumer Comfort, June 23 (prior -37.9)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas change

- 11am: Kansas City Fed Manf. Act., June, est. 4 (prior 9)

- 11am: Fed to sell $8-8.75b notes in 11/15/2014-6/15/2015 range

- 11:30am: Fed’s Pianalto speaks in Cleveland

- 1pm: Treasury to sell $29b 7-yr notes

- 7pm: Fed’s Fisher speaks in Aspen, Colorado, on U.S. economy

GOVERNMENT:

- U.S. Supreme Court will issue its health-care ruling, 10am

- House, Senate in session

- Senate Commerce Committee holds a hearing examining whether online advertising industry self-regulation of consumer privacy is providing adequate protections, 10am

- House Financial Services subcommittee holds hearing, “Fractional Reserve Banking and the Federal Reserve: The Economic Consequences of High-Powered Money” 2pm

- The American Enterprise Institute for Public Policy Research

- holds a discussion on “Do Money Market Funds Create Systemic Risk?” 2pm

- SEC Chairman Mary Schapiro to testify before House Oversight subcommittee hearing on Jobs act, 9:30am

- Interior Dept to announce final 5-year program for offshore oil, gas dev.; Secretary Ken Salazar holding conf. call at 3pm

- CFPB releases report on reverse mortgages

WHAT TO WATCH:

- News Corp. board said to approve plan to split up company

- Google unveils $199 tablet in bid to vie with Apple, Amazon

- Apple said to prepare iTunes changes to improve storage, sharing

- Watch suppliers, rivals as GOOG unveils ASUS-designed tablet

- Europe’s leaders today cap their latest effort to check the financial crisis that claimed Cyprus this wk as its 5th victim

- Nine of the biggest banks are set to deliver plans this wk for how their businesses could be unwound after a collapse

- Peter Madoff to plead guilty to fraud in brother Bernard Madoff’s Ponzi scheme

- Amazon.com said to add social features to digital games for tablet

- T-Mobile USA CEO Philipp Humm will quit, leaving Deutsche Telekom’s U.S. division in search of a replacement as it tries to recover from a failed sale to AT&T last yr

- AMR says ruling on voiding union contracts delayed by pilot vote

- Veolia sells U.K. water unit for $1.9b to reduce debt

- Fed to boost Operation Twist with QE3 jolt: Bank of America

- Euro-area June eco. confidence falls to 89.9, est. 89.6, is lowest since Oct. 2009

- Italy sells 2022 bonds to yield 6.19% vs 6.03% on May 30; sells 2017 bonds to yield 5.84% vs 5.66% on May 30

- U.K. 1Q GDP falls 0.3% in line with previous estimate

- South Korea cut growth est. for this yr to GDP may expand 3.3% vs Dec. est. +3.7%, announced 8.5t won ($7.4b) of spending

- Lending to Europe puts U.S. home loan banks at risk, says audit

EARNINGS:

- Family Dollar Stores (FDO) 7am, $1.07

- MSC Industrial Direct (MSM) 7:30am, $1.11

- Shaw Communications (SJR/B CN) 8am, $0.43

- Worthington Industries (WOR) 8:15am, $0.52

- Empire (EMP/A CN) 8:50am, $1.16

- Accenture (ACN) 4pm, $0.99

- TIBCO Software Inc (TIBX) 4:04pm, $0.23

- Research In Motion (RIM CN) 4:15pm, $(0.07)

- Nike (NKE) 4:15, $1.37

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Glencore Courts Qatar as Xstrata Tweaks Merger Pay: Commodities

- Corn Extends Biggest 4-Day Rally in 14 Months as U.S. Crops Wilt

- Oil Drops in London on Speculation Europe’s Outlook Will Worsen

- Sugar Ends Rally as Surplus Overwhelms Demand; Coffee Declines

- Copper Seen Falling as German Unemployment Fans Crisis Concern

- Gold Erases Gains in London as Dollar’s Strength Erodes Demand

- Oil Over $100 Seen After Worst Quarter Since ‘08: Energy Markets

- Koreans Await Monsoon Rains to Break Worst Drought in a Century

- Corn Peak in 1988 Drought Hints Rally May End: Chart of the Day

- Hog-Herd Expansion Signaling Losses After Corn Surge Boosts Cost

- World’s Largest Atomic Plant to Be Started, Tepco Says: Energy

- Chinese Steel Prices Drop to Two-Year Low on Weakening Demand

- Thailand Seeks Rubber-Export Limits With Indonesia, Malaysia

- Monsoon Worst Since 2009 Threatening Crop Prospects in India

- Indian Exchange Seeks to End Guar Futures Ban Before Sowing

CURRENCIES

EUROPEAN MARKETS

GERMANY – been calling this out this week, and it’s really obvious this morning – Germany has more risk now (to the downside) than Spain on our TRADE/TREND equity market signal. After failing at its TRADE line yesterday (6259), the DAX is back into a Bearish Formation, down -1.3%, leading European losers this morning.

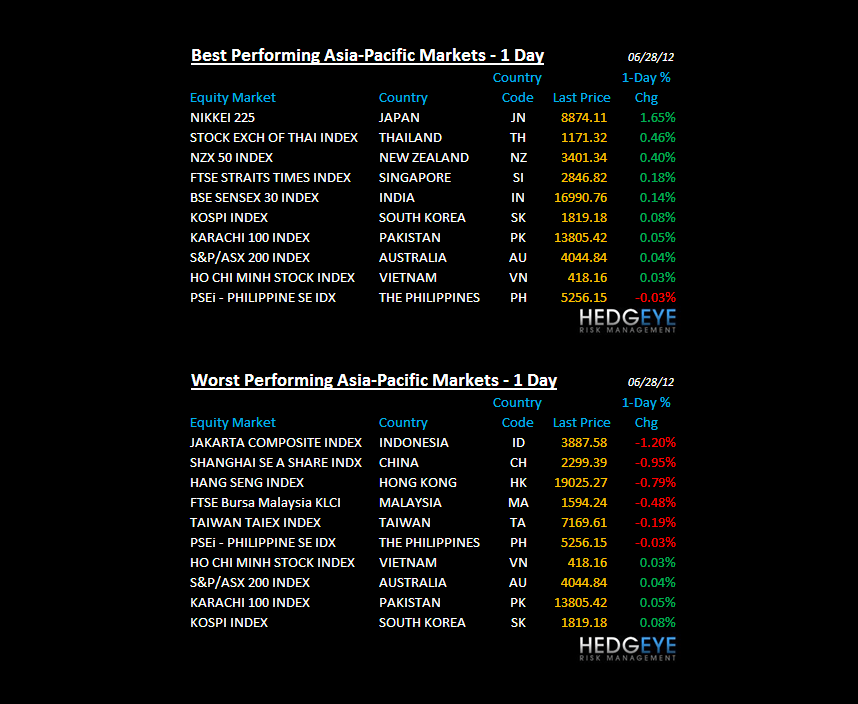

ASIAN MARKETS

CHINA – someone needs to tell the Chinese that the Italians are on it, because the dudes in Shanghai are freaking right out at this pt, pounding the Shanghai Comp to fresh new lows (down another 1% last night; down 10.5% since May 4th). *Reminder – any reactionary Chinese stimulus only amplifies #GrowthSlowing.

MIDDLE EAST

The Hedgeye Macro Team