This note was originally published at 8am on June 13, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The real test is how you behave when the crowd is roaring the other way.”

-George Goodman

Question: from an expectations perspective, have markets really changed since George Goodman penned The Money Game in 1968? As the weak whisper and the manic chase, that question has been on my mind for the last few weeks. Just a question.

While I’m at it, here’s another question: are you #Fedup yet? This morning’s Most Read (Bloomberg) headline = “US Stocks Gain Amid Speculation of More Fed Stimulus.” That’s awesome, right?

Right, right. And so is eating yellow snow.

Back to the Global Macro Grind…

Maybe Bernanke should read something from the late 1960’s and early 1970’s. Actually, wait a minute, Fred Kelly wrote in 1930 that “the crowd always loses”, so maybe Bernanke did read that. The man knows the 1930’s!

The Real Test in this game is not whether you are a student of one window of history. It’s whether or not you can beat the crowd. If Bernanke thinks he can thread the needle here into and out of next week’s FOMC meeting (June 20th), I say godspeed to him on that. He’s got the crowd right addicted to the drugs at this point, so how this all ends is anyone’s guess.

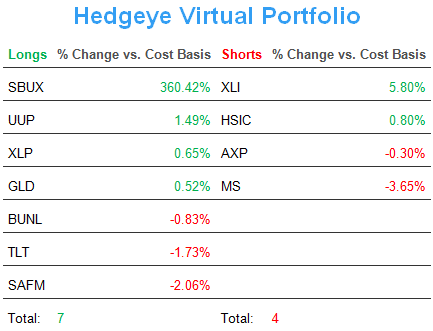

That said, I bought Gold and took my US Equity exposure up from 0% to 6% on red yesterday morning. Heck, why not roll the bones with The Bernank? This guy is a genius. Or at least that’s what the Washington crowd says.

Obviously I don’t play this game like roulette. That’s what some other people do (with other people’s money). The moves I make on red and green are based solely on my process. That investment process has 2 big parts:

A) The Research View

B) The Risk Management View

To be crystal clear, research and risk management are two very different things.

Quite often, as is the case with evaluating Fed Policy, what our research says Bernanke should do (nothing) and what he might do (something) are opposing thoughts.

When that happens, The Real Test is to remain sane and press the right buttons at the right time.

Timing? Yep, it matters.

In a market that’s being driven by a Correlation Risk that’s going to 1, timing matters, big time. Get the daily direction of the US Dollar right, and you’ll get a lot of other things right. With the USD down -0.35% yesterday, the best performing sector in the SP500 was the commodity heavy Basic Materials sector (XLB) at +1.9%.

Here’s an update on that (correlation risk between the US Dollar Index and everything else on a 2-month duration):

- SP500 = -0.92

- Euro Stoxx600 = -0.94

- CRB Commodities Index = -0.93

- WTI Crude Oil = -0.95

- Gold = -0.78

- Rubber = -0.93

I really hope you haven’t been long Rubber for the last 2 months.

Hope, of course, is not a risk management process. Neither is whining about “valuation” while ignoring the Correlation Risk. When it matters, it matters – and your Real Test as a real-time Risk Manager is to solve for that.

This is why I have been so hard on Bernanke and Geithner. If we get their dogmas and policies out of the way, we’re making the 1stcritical (causal) step in getting expectations for more USD driven correlation risk out of the way.

I know, it makes simple sense. What is not simple is that short-term political career risk (admitting they’ve had this all wrong since going to Qe2) gets in the way of the truth.

The truth is that Big Government Intervention policy expectations drive market expectations. That’s not free-market capitalism. That’s just really screwed up.

Maybe I’ll be long Gold for an hour. Maybe I’ll be long it for a week. Maybe I’ll be long it to $2,000 an ounce. I have no idea. And I shouldn’t, because I have no idea what this un-elected central market planner is going to do next.

What I do know is that if Obama gives Bernanke the political weaponry to debauch the Dollar one more time before the election, Gold and Oil are going to rip, and #GrowthSlowing is going to become the Research View of 2012.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1604-1648, $96.27-99.42, $81.98-82.56, $1.24-1.26, and 1304-1340, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer