Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

Key Takeaways:

* US/European bank swaps were broadly tighter last week on the heels of favorable Greek elections and Moody's downgrades being less bad than feared. We'd remind investors that (a) even if Greek austerity terms are eased, the rate of contraction in the Greek economy will make compliance nearly impossible, setting the stage for another showdown, and (b) Moody's downgrades have costs. While we saw lots of commentary about funding costs not being affected by the downgrades, the more salient takeaway is that institutions that moved to triple-B should see derivatives flow move away, on the margin.

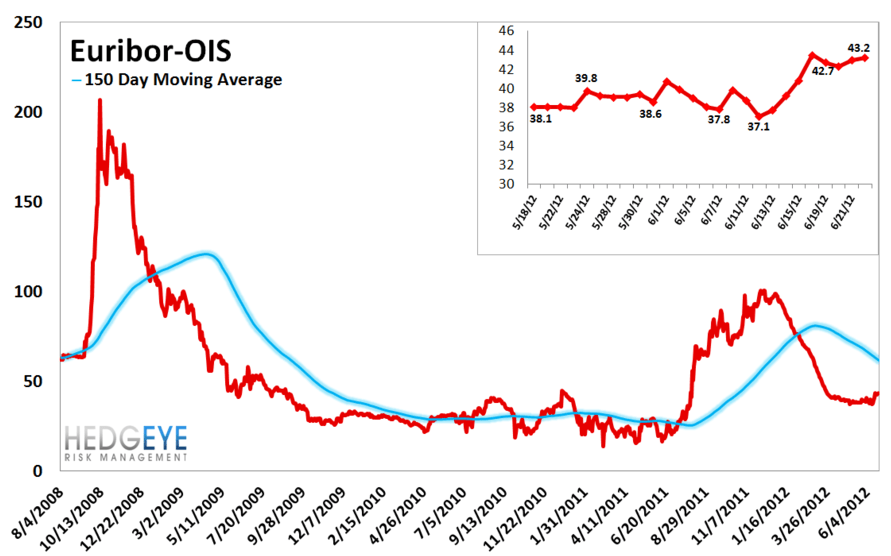

* Risk took a breather last week as large declines in high yield, MCDX and higher leveraged loan prices were indications that the temporary calm in Europe was enough for a broad-based rally. Interestingly, the one measure you'd have expected to contract actually expanded: Euribor-OIS.

-------

If you’d like to discuss recent developments in Europe, from the political to financial to social, please let me know and we can set up a call.

Matthew Hedrick

Senior Analyst

(o)

--------

European Financials CDS Monitor – 31 of the 39 European financial reference entities we track saw spreads tighten last week. The median tightening was 7.4% and the mean tightening was 1.8%. It's notable that the Spanish banks were the worst performers of the group.

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread has been moving higher of late for the first time in a long time. It ended the week at 43 bps.

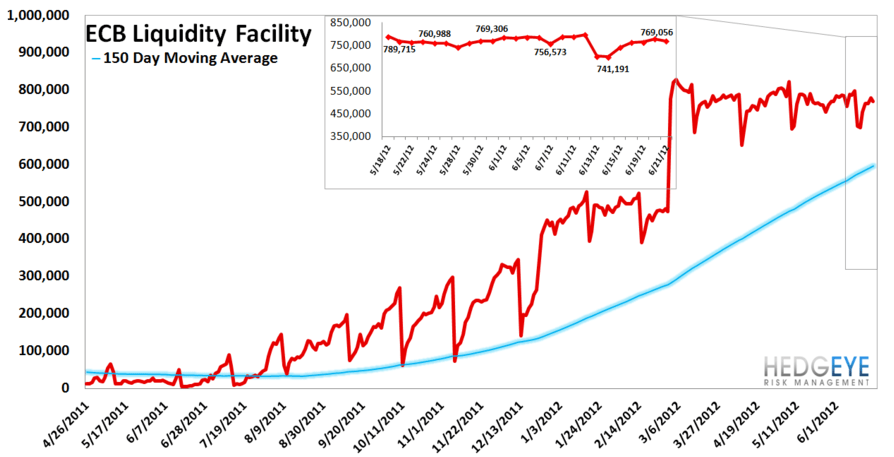

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis. This data shows through Thursday.

Security Market Program – For the fifteenth straight week the ECB's secondary sovereign bond purchasing program, the Securities Market Program (SMP), purchased no sovereign paper for the latest week ended 6/22, to take the total program to €210.5 Billion.