TODAY’S S&P 500 SET-UP – June 25, 2012

As we look at today’s set up for the S&P 500, the range is 17 points or -1.27% downside to 1318 and 0.00% upside to 1335.

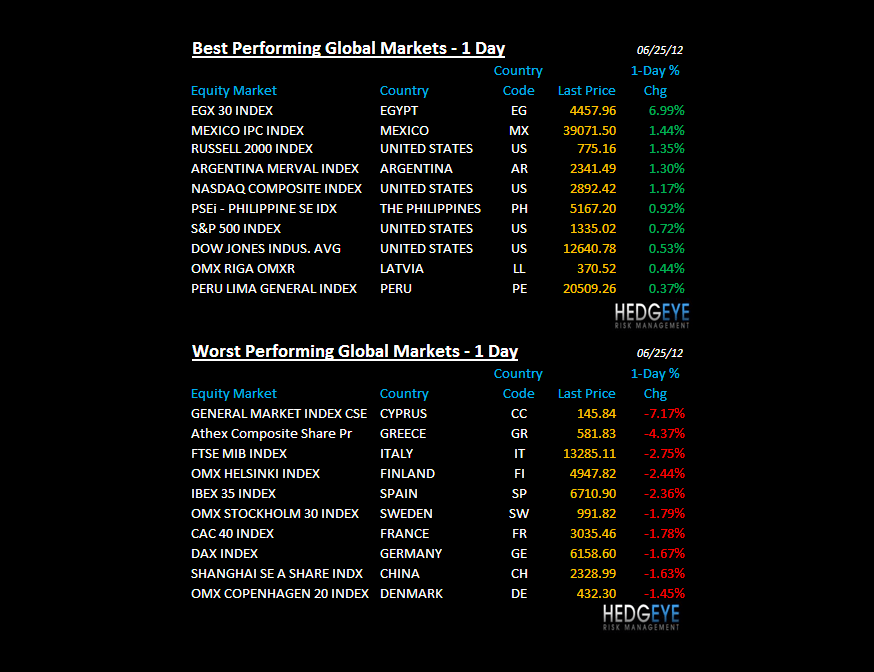

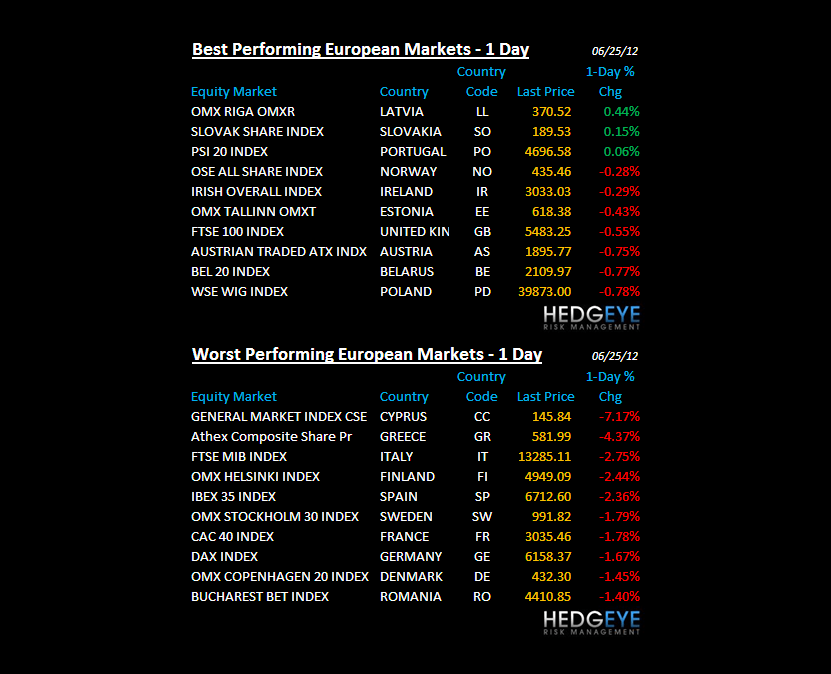

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/22 NYSE 1140

- Up from the prior day’s trading of -1901

- VOLUME: on 6/22 NYSE 1577.41

- Increase versus prior day’s trading of 82.18%

- VIX: as of 6/22 was at 18.11

- Decrease versus most recent day’s trading of -9.81%

- Year-to-date decrease of -22.61%

- SPX PUT/CALL RATIO: as of 6/22 closed at 1.65

- Down from the day prior at 1.81

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.62

- Decrease from prior day’s trading at 1.67

- YIELD CURVE: as of this morning 1.33

- Down from prior day’s trading at 1.37

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Nat Activity Index, May (prior 0.11)

- 10am: New Home Sales, May, est. 345k (prior 343k)

- 10:30am: Dallas Fed Manf. Activity, June (prior -5.1)

- 11am: Fed to sell $8-8.75b notes in 3/15/2014-10/31/2014 range

- 11:30am: Treasury to sell $30m 3-mo. bills, $27m 6-mo.

- 4pm: USDA crop progress report

GOVERNMENT:

- Washington Week Ahead: Supreme Court may rule on health law

- Supreme Court may rule on challenge to health-care law

- House, Senate in session

- Senate to take up long-term flood insurance reauthorization

- Heather Zichal, White House energy and climate adviser, speaks on hydraulic fracturing at New Policy Institute, 12pm

- Export-Import Bank President Fred Hochberg speaks at Center for American Progress, 12pm

- Treasury Undersecretary for International Affairs Lael Brainard speaks at Women’s Foreign Policy Group discussion on “International Financial Diplomacy,” 1pm

- George Walz, VP at Financial Industry Regulatory Authority’s Office of Risk, joins panel discussion on “FINRA Examination Data Collection Process,” 1:30pm

- HHS, CMS advisory panel meets on Medicare Economic Index price, productivity measurements, 8:30am

- WTO dispute settlement body meets in Geneva

- International Trade Commission to say whether it will review findings by 2 of its judges that MSFT, AAPL infringed Motorola Mobility patents

- Governmental Accounting Standards Board meets in Conn. to vote on state, local pension-reporting rules that would reduce funded levels of plans

WHAT TO WATCH:

- AB Inbev said to near Modelo takeover for more than $12b

- Supreme Court announces decisions; may rule on challenge to health-care law: preview

- ITC to say whether it will review findings that MSFT, AAPL infringed Motorola Mobility patents

- Fitch downgrades Republic of Cyprus to junk

- European leaders prepare for summit on currency union

- Tropical Storm Debby may spare Gulf of Mexico oilfields

- Russell Indexes to post final membership lists for indexes

- Shire falls after FDA unexpectedly approved a generic version of its hyperactivity medicine Adderall

- Pixar’s “Brave” opens at No. 1 in U.S./Canada theaters with $66.7m for parent Walt Disney

- JPMorgan to let CIO make potentially risky investments: WSJ

- Sales of new homes probably rose in May for 2nd month to 346k annual rate, according to median forecast by Bloomberg News

- New York settled a lawsuit for $410m with J. Ezra Merkin over claims that Merkin funds secretly placed client money with Bernard L. Madoff

- Banks need “healthy push” to avoid prolonging crisis: BIS

- Vivendi, whose mgmt met during the weekend to discuss strategy, said it had nothing to update investors with

- Bain said to pay $1b for 50% stake in Japanese TV company

- India plans measures to support rupee, spurring inflation

- No IPOs expected to price today: Bloomberg data

- Weekly Industry Agendas: Finance, Media/Entertainment, Industrials, Energy, Real Estate, Consumer, Health, Transports, Technology, IPOs, Canada Oil & Gas, Canada Mining

- U.S. Health Care, EU Summit, Google: Week Ahead June 23-30

EARNINGS:

- HB Fuller (FUL) After-mkt, $0.55

- Synnex (SNX) 4:01pm, $0.90

- Apollo Group (APOL) 4:05pm, $0.97

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG

- Bulls Proven Wrong as Prices Slump Into Bear Market: Commodities

- Gold Set to Decline in London as Stronger Dollar Curbs Demand

- Oil Trades Below $80 for a Third Day Amid European Debt Concern

- Grains Climb as Dry Weather Wilts U.S. Crops, Threatening Supply

- Copper Seen Advancing for First Day in Four Before EU Meeting

- Sugar Rebounds on Speculation Prices Fell Too Far; Coffee Slides

- Fonterra Farmers Approve Plan to Open Exporter to Equity Markets

- Morgan Stanley Expects Corn, Soybean Prices to Advance on Supply

- Hong Kong’s LME Deal Spurs Industry’s Steepest Slump: Real M&A

- Coal Plant Plunge Threatens Billions in Pollution Spend: Energy

- Hedge Funds Turning Bearish Push Oil Below $80: Energy Markets

- Florida Orange Trees Threatened on Tropical Storm Debby Floods

- Oil to End Commodity Currencies’ Divergence: Chart of the Day

- China Faces Summer Steel Output Cut on Prices: Chart of the Day

- Silver Seen Extending Drop as Support Breaks: Technical Analysis

CURRENCIES

EUROPEAN MARKETS

RUSSIA – get the Dollar and the Petro price right, and you get the Petro-Dollar equities right – this is obvious in Russian stocks (next to Egypt’s -9% drop last wk, the RTSI led losers at -5% and has now eclipsed Spain on my drawdown sheet for 2012 at -27% from YTD top vs Spain and Italy at -24% and -22%).

ASIAN MARKETS

CHINA – Shanghai Composite starting to lead losers in Global Equities as #GrowthSlowing accelerates on the downside (down another -1.6% overnight; down -9.2% since beginning of May) – we highly doubt Bernanke or Geithner have a central plan for China, but you never know…

INDIA – Keynesian economic disasters tend to end with currency debauchery, then local crisis – India’s Rupee is in the middle of one of those and it’s a huge problem domestically as inflation is priced in local FX; but do not worry, India is now saying they are unveiling a “dozen steps to save the Rupee” – almost like a Tony Robbins thing I guess…

MIDDLE EAST

The Hedgeye Macro Team