As we expected (DRI: SHAPING UP TO DISAPPOINT 6/21/12), 4QFY12 traffic trends disappointed at Olive Garden. What we didn’t expect, is that Red Lobster and LongHorn would also post such poor same-store sales numbers. Hiking the dividend is one way to keep investors happy but tough questions have to be asked of management.

Darden is an impressive company that has earned the investment community’s respect through years of producing strong financial results. CEO Clarence Otis, speaking on CNBC immediately after the print, was shining light on the full year results but the trajectory of comps during this most recent fiscal quarter is a concern going forward. What’s more concerning to us, is the lack of clarity on when consistent results can be expected at Olive Garden and how they will come about.

FY2013 Guidance and Outlook

Management's FY13 guidance lowered the bar versus the company’s long-term guidance. EPS growth is expected to be 8-12% versus the 10-15% longer term target while blended same restaurant sales growth guidance is 1-2% versus long-term guidance of 2-4%. During FY13, we expect EPS growth to benefit from more favorable food costs and other cost reduction initiatives. We cannot advise clients, with sufficient confidence, that a turnaround is afoot at Olive Garden. While we respect the operational acumen of the companies’ management teams, we are adopting a “show me” stance toward Darden’s numbers over the next couple of quarters. Hiking the dividend by 16% this morning is likely to help retain long-term holders, but believe that more intermittent volatility is likely for Olive Garden before the chain achieves consistency in its operational performance.

Olive Garden’s new menu and remodel program not being finalized at this point does not inspire confidence that a solution to the difficulties at Olive Garden is around the corner. Management cannot possibly predict consumer reaction to promotions and, while investors are waiting for the transition at Olive Garden to be completed, we feel that results at Olive Garden are going to continue to be inconsistent.

Below we go through our thoughts on the company’s three largest brands, their 4QFY12 results, and their individual outlooks for FY13.

Olive Garden

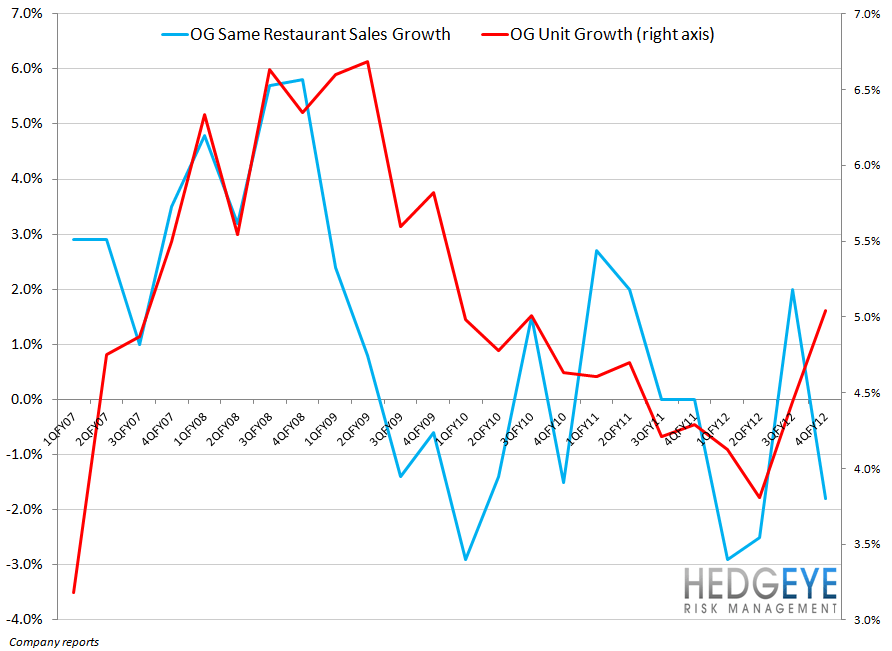

Darden’s largest chain, and a key focus for investors heading into this morning’s print, posted a disappointing same-restaurant sales number of -1.8% for the fourth fiscal quarter. According to Consensus Metrix, the Street was looking for 0.5% growth. Management apportioned most of the blame for Olive Garden’s disappointing comp store sales growth to performance during the month of May; the “Taste of Tuscany” promotion, which started at a price point of $10.95, failed to live up to management’s expectations. The Tuscany promotion extended into June so, as far as read-through for 1QFY13, the promotion proving ineffective is a negative indication. A decision not to advertise around Mother’s Day this year was also cited as a factor in the poor momentum at Olive Garden.

Looking forward to 2013, management is shifting towards a more “single-minded” approach to affordability. To that end, management is launching a new promotion, 2 for $25, which offers unlimited soup, salad, or bread sticks plus an appetizer or dessert plus an entrée. We are not convinced that this strategy will meet management expectations; there are many similar offers in the casual dining space.

One short-term concern we have is that the new menu is not going to be released at Olive Garden until 3QFY13. The menu is currently being tested at 40-50 stores. In the event that any adjustments need to be made to that menu, the start date could be pushed back further. Additionally, the Olive Garden remodel program – aimed at updating and refreshing 430 of the total ~800 stores – is in its final testing phase. The Street will be looking for more specificity from the company on the timetable of this initiative. Any protraction of the remodel program will only delay Olive Garden becoming a more consistent business.

A Darden earnings call without commentary on the Gap-to-Knapp (performance versus industry benchmark Knapp Track) is about as perturbing as a visit to Olive Garden without breadsticks. This break from tradition, while unsettling, is not a major surprise when we consider that Knapp Track results comfortably outperformed Olive Garden and Red Lobster monthly comps during 4QFY12. As keen as COO Andrew Masden was to highlight Olive Garden’s increasing strength versus the industry during 3QFY12, no such color was provided this morning. Here is the comment from 3/23, on Olive Garden trends versus the industry “Olive Garden same-restaurant sales were up 2% during the third quarter, roughly 60 basis points below the full-service restaurant industry benchmark. However, this is a sharp improvement from the 320 basis point shortfall in the second quarter.”

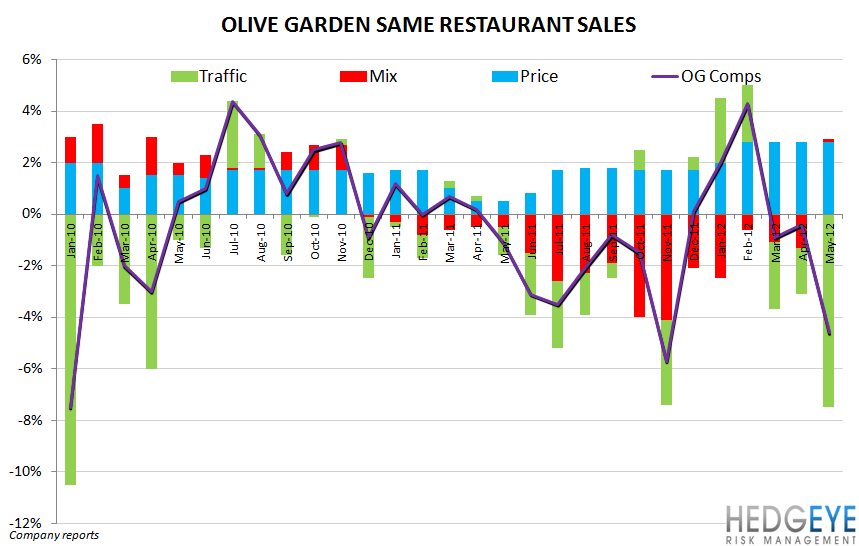

The new menu and remodel program may help end Olive Garden’s travails, but our near-term view is that the concept needs to find a way to become less price-dependent for top-line growth. On mix at Olive Garden, management had the following to say this morning: “the biggest dynamic is that we experienced at all of our large casual dining brands during 2012, we experienced a meaningful amount of menu mix, negative menu mix. So, guests trading down to lower priced items. Ordering fewer appetizers, fewer desserts. And we think that step-down is going to moderate during fiscal '13. So we wouldn't expect that negative trend in guest behavior to continue.” Looking at the chart paints a different picture. Mix was positive in May and negative for 17 consecutive months prior to that.

Red Lobster

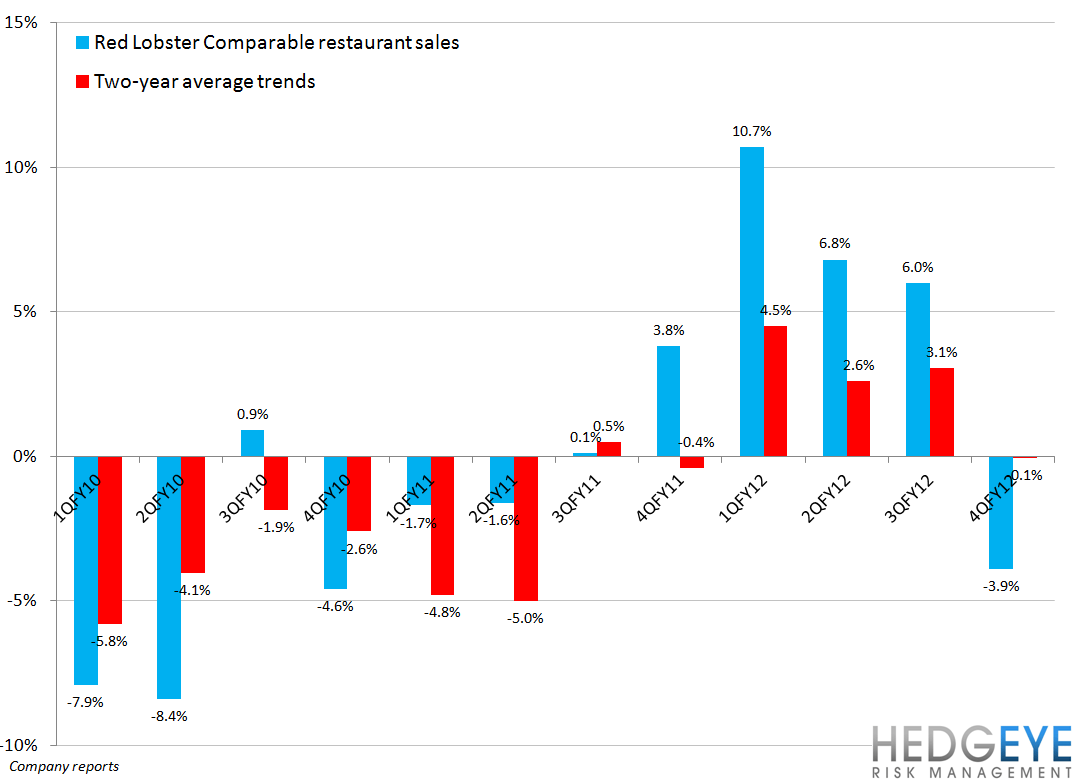

The Lenten period shift negatively impacted Red Lobster’s 4QFY12 results by 130 basis points. Same-restaurant sales came in at -3.9% versus Consensus Metrix expectations of +1.3%. Lobsterfest, a signature promotion for Red Lobster that typically coincides with the Lenten season, performed poorly this year due to the spike in gasoline prices occurring during the Lenten season.

The Festival of Shrimp promotion began at Red Lobster in late April and continued through May. The company took a price increase for the promotion of $1 from $11.99 to $12.99 based on its success last year and on research that suggested consumers were largely indifferent between $11.99 and $12.99. The same-restaurant sales decrease in May, according to management, shows that the price increase turned out to be too aggressive. This highlights a key concern we have for the Red Lobster business, as well as Olive Garden; the comps at their two largest businesses are overly dependent on price and the customer is highly sensitive to increases in price.

LongHorn Steakhouse

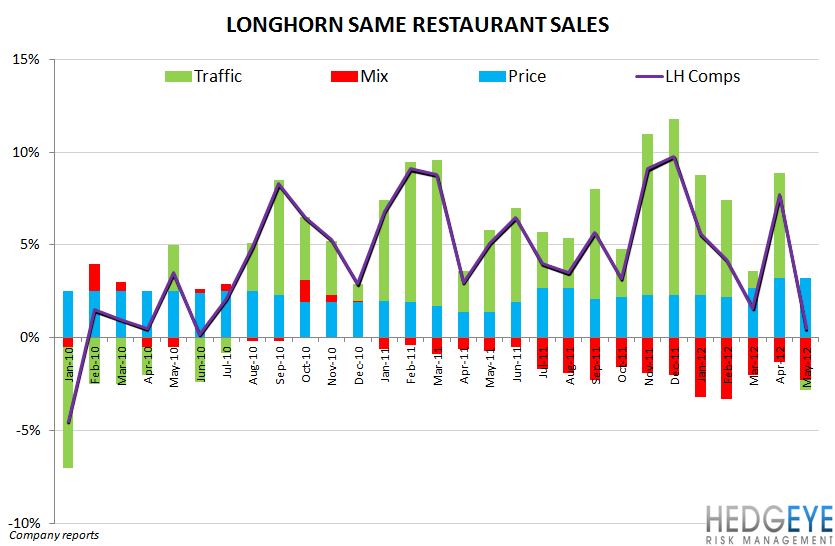

LongHorn’s comps came in lower than expected, which we highlighted as a possibility in our preview post. Increased competition in the steak category is making it difficult for LongHorn to take share as rapidly but, as a part of the Darden portfolio, we see this concept as a bright spot for the company. As the chart below indicates, comps sequentially slowed to 3% from 6.7% the quarter prior and Consensus Metrix 4QFY12 expectations of 4.5%. This stock is important for the longer-term TAIL story, but as we wrote in our preview note published yesterday morning, Olive Garden and Red Lobster are more important for the immediate-term TRADE and intermediate-term TREND.

Conclusion

The underlying fundamentals of Olive Garden are a concern for Darden’s business over the near-term. We see the transition period as possibly lasting longer than some investors are expecting and there is substantial risk, in our view, of mishaps occurring as the company makes adjustments to its most important brand while accelerating unit growth. We are content to sit on the sideline for now. The dividend yield will continue to provide support for the stock but our expectation is for the first and (possibly) second quarter to be a difficult period for Darden.

Howard Penney

Managing Director

Rory Green

Analyst