-- For specific questions on anything Europe, please contact me at to set up a call.

No Current Positions in Europe: Covered EUR/USD (FXE) on 6/21; Covered Spain (EWP) on 6/18; and Sold German Bonds (BUNL) on 6/18

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.0% week-over-week vs +2.9% last week. Top performers: Greece +8.6%; Finland +5.0%; Cyprus +3.0%; Portugal +2.9%; Spain +2.3%; Italy +2.0%; Denmark +1.7%. Bottom performers: Russia (RTSI) -5.0%; Slovakia -1.9%; Norway -1.8%; Ireland -0.9%; Austria -0.8%.

- FX: The EUR/USD is down -0.59% week-over-week vs -0.58% last week. W/W Divergences: HUF/EUR +2.28%, NOK/EUR +0.70%, TRY/EUR +0.54%, GBP/EUR -0.24%; PLN/EUR -0.53%, CZK/EUR -1.27%, RUB/EUR -1.84%.

- Fixed Income: Yields came in dramatically this week. Portugal saw the biggest move, falling -104bps week-over-week to 9.54%. [Portugal’s 10YR has not seen sub 10% in over a year!] Greece also saw a large decline, falling -67bps to 27.06%. Spain dropped -35bps and Italy fell -20bps to 6.53% and 5.80%, respectively. Germany bounced +5bps week-over-week to 1.55%.

No Bazooka! Go Figure!

With the Greek elections over, and some insight into Spain’s bank recapitalization needs behind us, what’s next for Europe? This week we saw a few interesting phenomenon: peripheral yields and risk metrics (CDS) came down dramatically, while new peripheral sovereign paper was issues at significant premiums (vs pervious auctions as recent as last month), and data—including confidence figures and PMIs—were bombed out! [See below in Data Dumb]. Now all eyes are peeled on the EU Summit next week (June 28-9) for the delivery of a “panacea” to cure Europe’s ails. Even a major investment bank was out this morning saying that it has heard from participants at the recently ended G-20 meetings in Mexico that there could be a “bazooka” of sorts in the works!

Our response: there’s a fat chance Eurocrats can craft anything close to a bazooka/panacea next week.

What will the Eurocrats discuss? Well, there’s actually a ton of programs on the table for discussion, which in and of itself lends to a higher probability that nothing concretely gets issued. The main topics of discussion should include:

- Fiscal Compact

- Pan-European Deposit Insurance

- Eurobonds

- European Redemption Fund

- ESM (and EFSF)

- European Financial Transactions Tax

We continue to view Ms. Merkel as the Eurozone’s paymaster, the lead horse pulling the Eurozone cart along, but also a party at the table not willing to fold her cards. In this light, we expect Merkel to argue for more fiscal integration (signatures on the Fiscal Compact from a majority of the 27 EU members), the first step before such programs as Eurobonds and a European FDIC can even be imagined. This week the Germans largely pressed forward in support of a financial transaction tax, with or without the backing of the other member states. We’re slightly surprised by the positioning and will wait to see how this development plays out.

However, a more pressing question that should be discussed in earnest at the Summit surrounds the capabilities of the existing EFSF and ESM. Importantly, the ESM still needs to be ratified by the German Parliament, which is expected to take place on June 29th. Already, EU leaders have said that it is now expected to come online on July 9, versus the original proposal of July 1. In any case, there needs to be clarification on the terms of the ESM, namely if it can be directed for bank recapitalizations, and if borrowing from the ESM contributes to the debt of the borrowing country. Here the problem is that Europe doesn't have a TARP-like facility to lend directly to the banks, but must lend to the sovereigns first.

Our longer-term read through is that this Summit, like most in the past, will disappoint investors. We believe that 1.) the IMF may need to take a larger role in bailing out Europe, as individual countries will not post more money to existing bailout facilities, and 2.) Eurobonds may be the only quasi “bazooka” left, however the coordination of such subsidized bonds are many months, if not years, ahead.

Enjoy today’s match between Germany and Greece at 2:45pm EST!

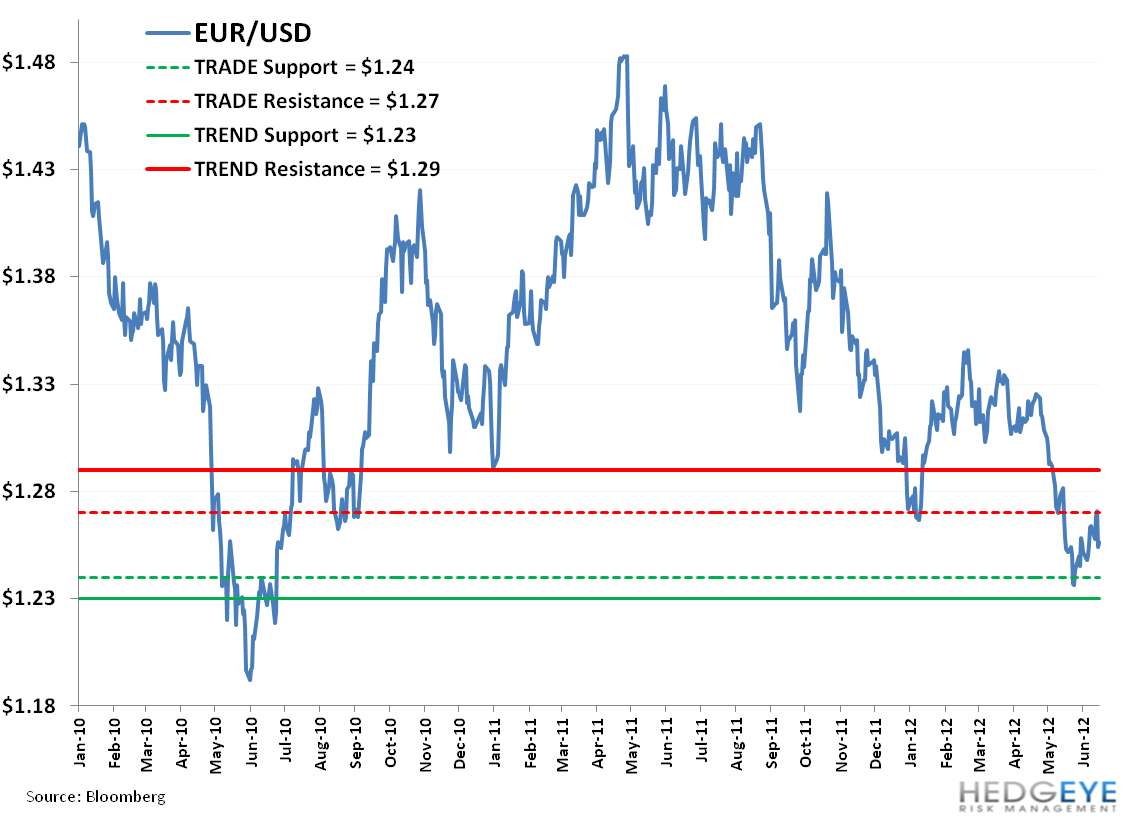

EUR-USD:

Below is an updated EUR/USD price level chart. Our immediate term TRADE support is $1.24 and resistance is $1.27. Our intermediate term TREND support level remains at $1.23. Our call is that if $1.23 breaks, look out below! We’re not EUR parity folks because we see Eurocrats stepping in to prevent it.

Call Outs:

Spain - According to stress tests conducted by the consultants Roland Berger and Oliver Wyman, Spanish banks recapitalization needs could reach €62 billion in a worst-case scenario. The base line scenario implies a 1.7% drop in real GDP this year and a 0.3% fall in 2013 alongside a 5.6% fall in housing prices this year and 2.8% the following year.

Spain - Spain has notified the four firms (Deloitte, KPMG, PwC and Ernst & Young) currently working on a second and more detailed audit of Spanish banks that the deadline to present their reports has been moved to September from 31-Jul.

IMF - says that emerging market economies have formalized funding pledges bringing total size of firewall up to $456 billion from $430 billion in April (China will give $43 billion while Mexico, Russia, India, Brazil commit to $10 billion each).

Eurogroup Chief - The press is reporting that French President Hollande will lobby his German, Italian and Spanish peers about the possibility of making his finance minister, Pierre Moscovici, head of the Eurogroup. Hollande's efforts may challenge German Finance Minister Wolfgang Schaeuble’s path forward; he was long thought to be the frontrunner to take over for Jean-Claude Juncker.

ECB - ECB Executive Board member Benoit Coeure, said in an interview that an interest rate cut was likely to be discussed at next month's meeting (5-July). However, he noted that while cutting rates was certainly an option as far as monetary policy is concerned and could help to some extent, it would not fix the fundamental problems in Europe. Recall that ECB President Draghi said that three members had pushed for a rate cut at the last ECB meeting on 6-June.

UK - Minutes from the BOE’s latest meeting showed that Governor King was overruled 5-4 to keep its bond- purchase target at 325 billion pounds this month. This is the first time since 2009 that King was overruled. King, Adam Posen and David Miles called for a 50 billion-pound expansion, and Paul Fisher’s bid for 25 billion pounds.

CDS Risk Monitor:

Like sovereign yields, sovereign CDS saw a large down move this week. Portugal saw the largest decline in CDS w/w at -195bps to 847bps, followed by Ireland -44bps to 625bps, Italy -28bps to 509bps, and Spain -21bps to 569bps. [Portugal hasn’t been sub 900bps since 7/6/2011!].

Data Dump:

Manufacturing PMIs JUN Preliminary:

Eurozone 44.8 JUN vs 45.1 MAY

Germany 44.7 JUN vs 45.2 MAY

France 45.3 JUN vs 44.7 MAY

Services PMIs JUN Preliminary:

Eurozone 46.8 JUN vs 46.7 MAY

Germany 50.3 JUN vs 51.8 MAY

France 47.3 JUN vs 45.1 MAY

*Eurozone Composite PMI 46.0 JUN vs 46.0 MAY

Eurozone ZEW Economic Sentiment -20.1 JUN vs -2.4 MAY

Eurozone Construction Output -5% APR Y/Y vs -2.6% MAR [-2.7% APR M/M vs 11.4% MAR]

Germany ZEW Current Situation 33.2 JUN (exp. 39) vs 44.1 MAY

Germany ZEW Economic Sentiment -16.9 JUN (exp. 2.3) vs 10.8 MAY

Germany IFO Business Climate 105.3 JUN (105.6) vs 106.9 [2yr low]

Germany IFO Current Expectations 113.9 JUN (exp. 112) vs 113.2 MAY

Germany IFO Expectations 97.3 JUN (exp. 99.8) vs 100.8 MAY

Germany Producer Prices 2.1% MAY Y/Y vs 2.4% APR (slows to a 23-month low)

France Own Company Production Outlook -4 JUN vs -4 MAY

France Production Outlook Indicator -30 JUN vs -28 MAY

France Business Confidence Indicator 92 JUN vs 93 MAY

UK Retail Sales w Auto Fuel 2.4% MAY Y/Y vs -1.1% APR [1.4% MAY M/M vs -2.4% APR]

UK CPI 2.8% MAY Y/Y (exp. 3%) vs 3.0% APR [-0.1% MAY M/M vs 0.6% APR]

UK RPI 3.1% MAY Y/Y vs 3.5% APR

UK ILO Unemployment Rate 8.2% APR vs 8.2% MAR

UK Jobless Claims Change 8.1K MAY (exp. -4K) vs -12.8K APR

Italy Consumer Confidence 85.3 JUN (exp. 86) vs 86.5 MAY

Italy Industrial Orders -12.3% APR Y/Y (exp. -8.6%) vs -14.3% MAR

Spain Mortgages on Houses -31.3% APR Y/Y vs -42.0% MAR

Switzerland ZEW Credit Suisse Expectations of Economic Growth -43.4 JUN vs -4 MAY

Switzerland Exports 1.8% MAY M/M vs -0.7% APR

Switzerland Imports -0.1% MAY M/M vs 3.1% APR

Switzerland M3 Money Supply 6.2% MAY Y/Y vs 6.3% APR

Holland Unemployment Rate 6.2% MAY vs 6.2% APR

Holland House Price Index -5.5% MAY Y/Y vs -5.2% APR

Holland Consumer Confidence -40 JUN vs -38 MAY

Austria Industrial Production 0.4% APR Y/Y vs 0.8% MAR

Sweden Unemployment Rate 8.1% MAY (exp. 7.8%) vs 7.8% APR

Sweden Consumer Confidence 3.1 JUN (exp. 4) vs 5.9 MAY

Sweden Manufacturing Confidence -4 JUN (exp. -2) vs -1 MAY

Russian Industrial Production 3.7% MAY Y/Y vs 1.3% APR

Russia Disposable Income 3.6% MAY Y/Y vs 2.1% APR

Russia Real Wages 11.1% MAY Y/Y vs 11.1% APR

Russia Producer Prices 3.1% MAY Y/Y vs 6.7% APR

Russia Retail Sales 6.8% MAY Y/Y vs 6.5% APR

Russia Unemployment Rate 5.4% MAY vs 5.8% APR

Russian Investment in Production Capacity 7.7% MAY Y/Y vs 7.8% APR

Poland Core Inflation 2.3% MAY Y/Y vs 2.7% APR

Poland Producer Prices 5.0% MAY Y/Y vs 4.3% APR

Poland Producer Prices 3.2% MAY Y/Y vs 3.6% APR

Slovakia Unemployment Rate 13.2% MAY vs 13.4% APR

Slovenia Unemployment Rate 11.8% APR vs 12.0% MAR

Ukraine Industrial Production 1% MAY Y/Y vs 0.0% APR

Turkey Consumer Confidence 92.1 MAY vs 91.1 APR

Interest Rate Decisions:

(6/20) Norwegian Deposit Rate UNCH at 1.50%

(6/20) Bank of England voted 5-4 to maintain asset purchase program

The Week Ahead:

Sunday: Jun. Germany Import Price Index (Jun. 24-30)

Monday: Jul. Germany GfK Consumer Confidence Survey; May Spain Producer Prices

Tuesday: Jun. France Consumer Confidence Indicator; May France Jobseekers; May UK Public Finances, Public Sector Net Borrowing; May Italy Hourly Wages; Apr. Italy Retail Sales; Spain Budget Balance YtD

Wednesday: Jun. Germany Consumer Price Index - Preliminary; May Germany Import Price; Jun. UK CBI Reported Sales; May UK BBA Loans for House Purchases; May Spain Retail Sales; Jun. Italy Business Confidence

Thursday: EU Summit in Brussels (Jun 28-29) aim to formally sign off on growth proposals; EC meets to discuss Institutional Affairs; Jun. Eurozone Consumer Confidence – Final, Business Climate Indicator, Economic Confidence, Industrial Confidence, Services Confidence; Jun. Germany Unemployment Data; 1Q Germany GDP – Final, Current Account, Total Business Investment – Final; Jun. UK Nationwide House Prices, GfK Consumer Confidence Survey; Jun. Spain CPI - Preliminary; Apr. Spain Total Housing Permits; Jun. Italy CPI - Preliminary; May Italy PPI

Friday: Jun. Eurozone CPI Estimate; May Eurozone Money Supply; May Germany Retail Sales; May France Producer Prices, Consumer Spending; 1Q France GDP – Final; Apr. UK Index of Services; Apr. Spain Current Account; Apr. Greece Retail Sales; German Parliament to ratify the ESM and Fiscal Compact

Saturday: June 30th is the deadline for EU Banks to meet 106 Billion EUR capital target.

Extended Calendar Call-Outs:

JULY: France – extraordinary session of parliament in July is due to re-draft the 2013 budget

1 July: ESM to come into force

5 July: ECB governing council meeting

19 July: ECB governing council meeting

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst