HEDGEYE ANALYST:

Brian McGough, Managing Director of Retail (@HedgeyeRetail)

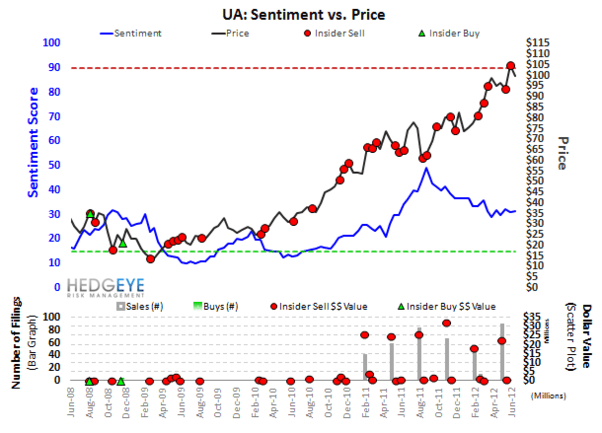

The case for Under Armour (UA) is an interesting one. After a meteoric rise in share price, the stock could be construed as a stock that’s “too expensive.” It’s up 100% since last August after swooping in and taking market share from Nike. After today’s post-UBS downgrade pullback and the unveiling of a new line of footwear, we added UA to the virtual portfolio. The long-term outlook for the company is very solid despite the cautionary landscape in the near-term.

Using our TRADE, TREND and TAIL durations, here are three takeaways on why UA is a long:

TRADE (Duration = 3 weeks or less)

UA remains a bit expensive and footwear isn’t really going anywhere right now. Though business appears to be stable, there will be a capital-intensive marketing campaign surrounding UA’s new line of shoes. Our TRADE support line is at $98.78.

TREND (Duration = 3 months or more)

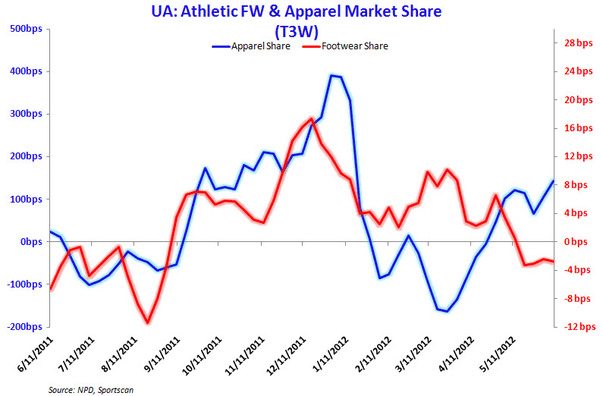

It appears that UA has finally got its inventory control levels sorted out and with a new management shake up that includes newly created positions, there’s a growth story here. UA is fixing problems that need to be addressed and by 2013, should be on its way to better margins and sales.

TAIL (Duration = 3 years or less)

We think that UA will put up $3 billion in revenue by 2014 after doing just $1.5 billion in 2011. Where does the growth come from? The incremental top line breaks out as follows. a) $500mm in core apparel growth, b) $300mm in incremental footwear, c) $300mm in international apparel, d) $250mm in women’s apparel, e) $125mm in accessories (having brought hats and bags licenses in house).

Under Armour is not an immediate-term stock to chase around. There is serious growth potential here that companies like Lululemon Athletica (LULU) can only hope to achieve.